As we kickoff 2023, Sprott says gold and mining shares are severely under owned.

Connecting a Few Dots

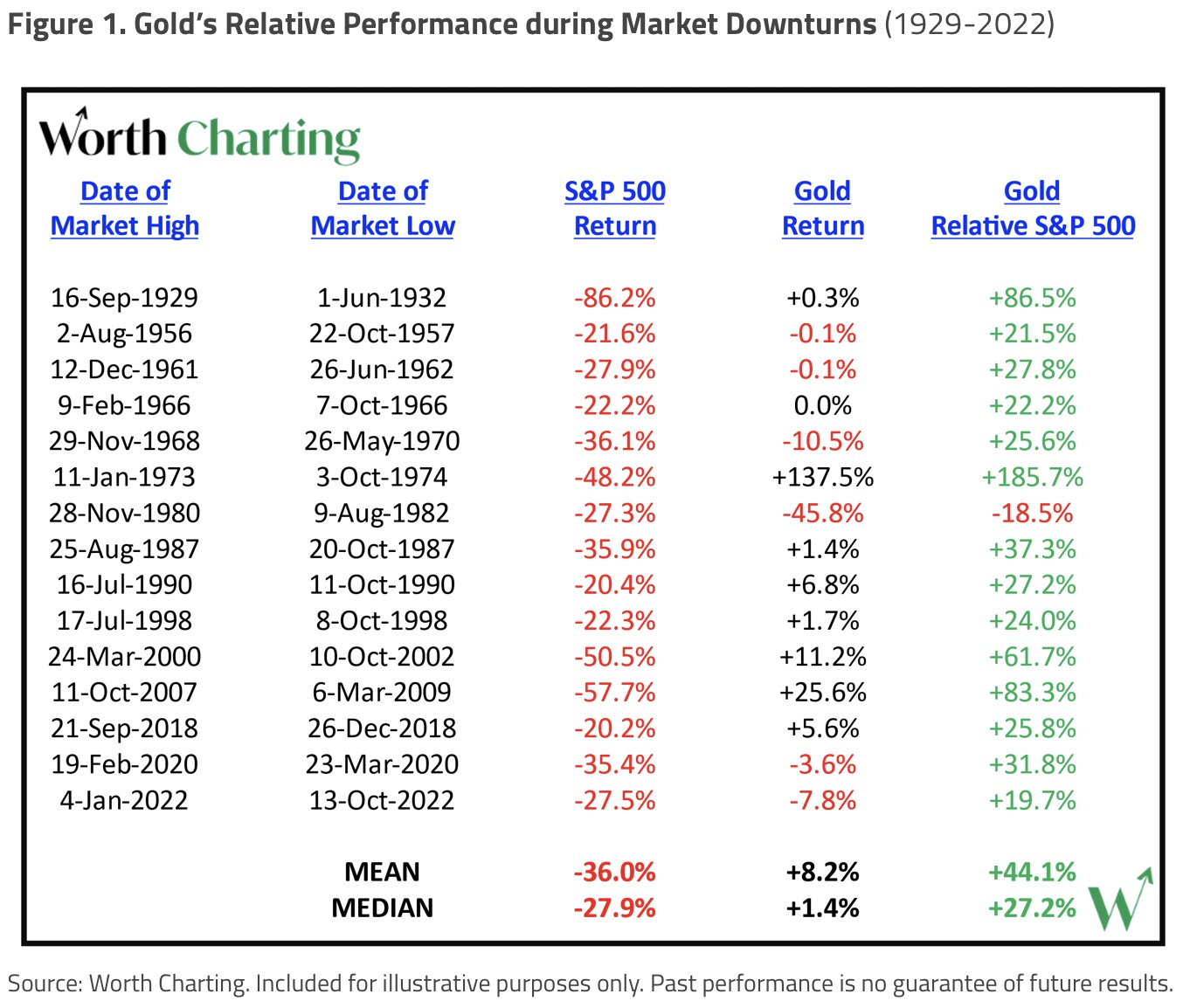

January 9 (King World News) – John Hathaway at Sprott Asset Management: Gold was an effective hedge in 2022. For the full year, gold bullion posted a -0.28% return, compared to a decline of 18.11% for the S&P 500 Index, an outperformance of 17.93%. Gold mining shares declined 8.14%, an outperformance of 9.97% relative to the S&P 500. U.S. Treasuries, considered a safe haven amidst adverse financial markets, fell 13.01%. We expect financial markets to continue to struggle in 2023. Gold and related mining shares, still severely underowned, should again demonstrate their merit as effective antidotes to ongoing macroeconomic chaos by striving to deliver strong absolute and relative performance.

2023 will reveal that the gross mispricing of financial assets that led to the worst performance of financial markets since 2008 has been only partially resolved. We believe the bear market is far from over, even though investment sentiment is more negative than at the market lows of 2002 and 2008 (AAII Investor Sentiment Survey). With the economy likely to slump into a protracted recession, the Federal Reserve (“Fed”) will be forced to abort its anti-inflation jihad. A Fed reversal could give temporary respite to financial assets. More importantly, it could underscore the dependency of public policy on money printing and provide a significant boost to the precious metals sector.

Despite the nonsensical but withering strong U.S. dollar and rising interest rate chatter that pinned gold to the penalty box in the eyes of mainstream groupthink for most of 2022, the yellow metal has emerged as the clear macroeconomic winner in relative and absolute terms. Gold’s emergence from 2022 as a bona fide safe haven comes as a surprise to consensus analysts, including Credit Suisse and J.P. Morgan which had forecasted year-end prices of $1,500 and $1,520, respectively. Gold has built a solid base, in technical terms, for a strong advance to new record highs against the supposedly invincible U.S. dollar. The following brief commentary will support these contrarian claims by connecting a few important dots.

Sovereign Debt Bubble Is Deflating

Despite aggressive Fed policies, interest rates remain well below where they might be if free market price discovery were to operate unconstrained. Supply promises to overwhelm demand. Rising fiscal deficits (due to the sharp decline in tax receipts, increased fiscal spending), Fed quantitative tightening ($95 billion/month, $1.1 trillion annually), and potential sales by non-U.S. holders (multiple reasons) could combine to produce the largest quantity of U.S. Treasuries for sale in decades. Foreign holdings of $7.5 trillion plus $8.8 trillion held on the Fed balance sheet equates to an overhang of $16.3 trillion.

As flagged by Luke Gromen (Forest For the Trees, 12/09/22):

“Tax receipts fell 11% y/y [year-over-year] in November, driven ‘largely’ by a drop in income and payroll taxes. Not only did higher U.S. interest rates drive U.S. income and payroll taxes down $23 billion, but they also drove U.S. government interest expense up $18 billion, driving a $41 billion deficit increase (which rose by $57B y/y total). This ‘receipts down with stocks and interest expense up with rates’ dynamic is how you get a 37% revision to U.S. 4Q22 projected deficits in just a three-month span.”

This sudden and unexpected change translates directly into increased borrowing (supply of U.S. Treasuries) of $150 billion. In our opinion, the dynamic of falling tax receipts, rising fiscal deficits and untamed inflation is likely to persist…

ALERT:

Legendary investors are buying share of a company very few people know about. To find out which company CLICK HERE OR ON THE IMAGE BELOW.

Sponsored

Sponsored

It appears that the U.S. fiscal situation may be spiraling out of control. The U.S. cannot afford a recession, which the Fed tacitly requires to combat inflation, because it would exacerbate the supply/demand mismatch in the treasury market. While market events of 2022 deflated many bubbles (FAANG, Crypto, Private Equity), sovereign debt ranks first and foremost among the deflated. The Keynesian playbook of modulating business cycles through monetary tightening followed by fiscal stimulus is running on empty. We believe that the Fed will be forced to pivot and abort its anti-inflation crusade sooner rather than later.

The Bear Market is Just Getting Started

Figure 2 shows consensus estimates (from 19 well-known strategists for major investment firms) for 2023 S&P Earnings and the projected closing price for the coming year. In December 2021, the same group projected the average year-end 2022 S&P 500 Index closing price would be 4,950, 28.92% above the actual close of 3,839.50. At first glance, the projected rise for 2023 of roughly 4.21% seems reasonable based on groupthink’s median earnings estimate of $219/share.

However, that earnings estimate does not seem reasonable against the backdrop of a 2023 recession. A Wall Street Journal article dated January 2, 2023, states that more than two-thirds of economists at major financial institutions expect a recession in 2023. What is interesting from a contrarian perspective is that most of these economists expect the recession to be shallow, in other words, a soft landing.

The stock market decline of 2022 was caused by lower valuations triggered by Fed-induced rising interest rates. Earnings came in pretty much as expected.

In 2023, if a (mild) recession-induced earnings decline of 10% -20% materializes, which would seem logical, a downside of at least that proportion could be in store, and even more should an extended bear take its usual toll on sentiment.

Other shoes that could drop include a steeper and more-protracted-than-expected recession (not the soft landing fantasy), pressure on the banking system caused by recession-associated credit deterioration, and geopolitical black swans.

With respect to the odds of the consensus expectation of a soft landing, former Treasury Secretary Larry Summers stated in a Bloomberg interview in December:

“It’s much harder than many people think to achieve a soft landing because there are all these mechanisms that kick in. At a certain point, consumers run out of their savings, and then you have a Wile E. Coyote kind of moment where consumption falls off. At a certain point, people start putting their houses on the market, and then you see house prices falling, and then other people rush to put them on the market. At a certain point, you see credit drying up, and when credit dries up, people can’t pay back their old borrowing. So, there is this proposition…when the unemployment rate goes up by 0.5%, it goes up by more than 2%. And that’s because once you get into a negative situation, there’s an avalanche aspect. And I think we have a real risk that that’s going to happen at some point.”

Financial market adversity tends to favor the time-tested protection offered by gold. Given the epic lack of exposure to gold in mainstream portfolios, a small shift in capital flows would have a disproportionate impact on the pricing of gold bullion and gold mining shares…

ALERT:

Billionaire mining legend Pierre Lassonde has been buying large blocks of shares in this gold exploration company and believes the stock is set to soar more than 150% in the next 6 months. To find out which company CLICK HERE OR ON THE IMAGE BELOW.

Further Dollar Weakness Ahead

Since posting our October 7, 2022, commentary, “The Dollar, Safe Haven or Leaky Lifeboat?”, the U.S. dollar index (DXY) has dropped from a near manic high of 115 (9/28/2022) to a current reading of 105 (1/04/23), a decline of approximately 8.70%. As noted in that article, the “strong dollar” was a major headwind for gold. Positioning by machine traders offset dollar exposure with short selling of gold. It remains a mystery to us how highly leveraged paper trades with little or no claim to physical metal are able to dominate gold bullion prices, but a partial explanation may lie in the fact that weekly trading in various gold derivatives exceeds $300 billion, according to a recent London Bullion Market Association (LMBA) study.9

The pronounced 2022 fourth-quarter weakness of the U.S. dollar signifies more than the post-mania sell-off of a consensus trade it might appear to be. It is, in our view, an early warning that the Fed’s tight money stance is unsustainable and that significant change is ahead. It quite possibly signifies that the jig may be up for U.S. Treasury bonds and sovereign credit, in general, as safe havens.

Never mind that the strong 2022 U.S. dollar created havoc for trading partners and emerging markets, leading some, including Japan, to divest holdings of U.S. Treasuries to defend their currencies (and others contemplating the same). Treasuries are, of course, denominated in U.S. dollars. As such, their increasing supply and the inventory overhang (Fed balance sheet, foreign holdings, Social Security system, etc.) are symptomatic of ongoing fiscal decay. As with previous manic tops, including the dot-com bubble (2000), complex mortgage instruments (2007) and crypto (2022), there has been an exhaustion of potential buying as well as the rationale for doing so.

What is the natural rate of interest for a debt instrument denominated in a defective currency? We suspect that it would be much higher than anything contemplated by the Fed or the investment consensus. When the Fed pivots, the exchange rate of the U.S. dollar might temporarily rise in anticipation of a boost to economic activity. However, longer-term market forces will, in our opinion, demand higher compensation to stabilize USD exchange rates…

ALERT:

Billionaire and mining legend Ross Beaty, Chairman of Pan American Silver, just spoke about what he expects to see in the gold and silver markets and also shared one of his top stock picks in the mining sector CLICK HERE OR ON THE IMAGE BELOW TO HEAR BEATY’S INTERVIEW.

Shadow Banking System Poses Systemic Risk

According to Sheila Bair, former Chair of the Federal Deposit Insurance Corporation, in an excellent Financial Times interview with Brooke Masters (12/15/2022), a recession could endanger global financial stability:

“Regulators have never really got to grips with private equity, hedge funds and private lenders, collectively dubbed ‘shadow banks.’ That means pension funds, endowments and other investors that put large amounts of money into private funds over the past decade are at risk of unexpected losses. If the turmoil then spills into public markets and the banking system, it could endanger global financial stability.”

According to the Financial Stability Board, global assets of shadow banks (non-bank financial intermediaries or NBFIs) exceed those of traditional financial institutions, $239 trillion vs. $182 trillion as of year-end 2021. Again, according to Bair:

“The weaknesses are obviously in the non-bank sector. In Dodd-Frank, the financial reform law, I pushed for regulators to be able to provide more oversight of the shadow banking sector, and those authorities largely have not been used. This stuff always comes back. You can’t insulate banks from instability in the non-bank sector. In the financial crisis, banks got blamed and they were responsible for a big part of it, but at the origination level it was primarily non-banks that were making unaffordable mortgage loans and securities firms played a big role in subprime securitizations. Non-banks were a clear driver during the financial crisis.”

Non-bank financial intermediaries are financial intermediaries that don’t use deposits. They use market-based funding or investor dollars to fund their assets. Some are publicly traded so there’s a bit more transparency, but not so with the private funds which have experienced the most dramatic growth. Market-based funding is not stable, so you experience a liquidity problem in times of stress. Bank deposits actually grow during a crisis, but market-based funding, investor funding, can disappear pretty quickly. If you use deposits, you get tons of regulation and oversight and of course deposit insurance, but if you fund through the market, you don’t.

Bair concludes:

“Getting overconfident, and listening to your own rhetoric about how well-capitalized the banks are is a real danger for bank regulators. Because there’s a lot of exposure they don’t fully understand. If the Fed takes us into a recession through monetary tightening and the big banks get into trouble again because they don’t have enough capital to absorb unexpected losses, then the Fed is going to have to do another bailout. That means it’s going to have to lower interest rates, open credit facilities, start printing money to pump the system with liquidity. That’s going to be inflationary.”

To summarize, complacency as to the soundness of the banking system based on the post-2008 reforms is not justified because those reforms did not address the risks latent in the shadow banking system. These risks are largely unaccounted for by the investment consensus. Even a mild recession could expose these risks, extend and deepen the downturn and panic policymakers into a new round of money printing…

ALERT:

Powerhouse merger caught Rio Tinto’s attention and created a huge opportunity in the junior gold & silver space CLICK HERE OR ON THE IMAGE BELOW TO LEARN MORE.

A Look Through the Geopolitical Lens

Much has been written about the war in Ukraine and the realignment of economic interests between the U.S., Europe and Eurasia. The kinetic war obviously suggests open-ended risks to any mainstream investment scenario about which there is little to be gained from further discussion.

More productive would be to take note of the negative implications for the international status of the U.S. dollar. In terms of a reserve currency, “the world is going from unipolar to multipolar and the actions of heads of state are far more important than the actions of central banks.” (Source: War and Commodity Encumbrance, Zoltan Pozsar, Credit Suisse Economics, 12/27/2022.)

Important developments in this regard are multiple agreements among Asian countries to settle trades in renminbi, rubles and or collateralized in some manner by underlying commodities, including gold. The institutional framework for circumventing the dollar appears to be a work in process, but that goal was made explicit in President Xi’s speech at the recently concluded (12/10/2022) China-GCC (Gulf Cooperation Council). Pozsar observes that these developments could represent the “dusk of the Petrodollar,” the international system in place since the 1970s of recycling trade surpluses into U.S. Treasuries, which has enabled the U.S. to finance seemingly perpetual internal and external deficits.

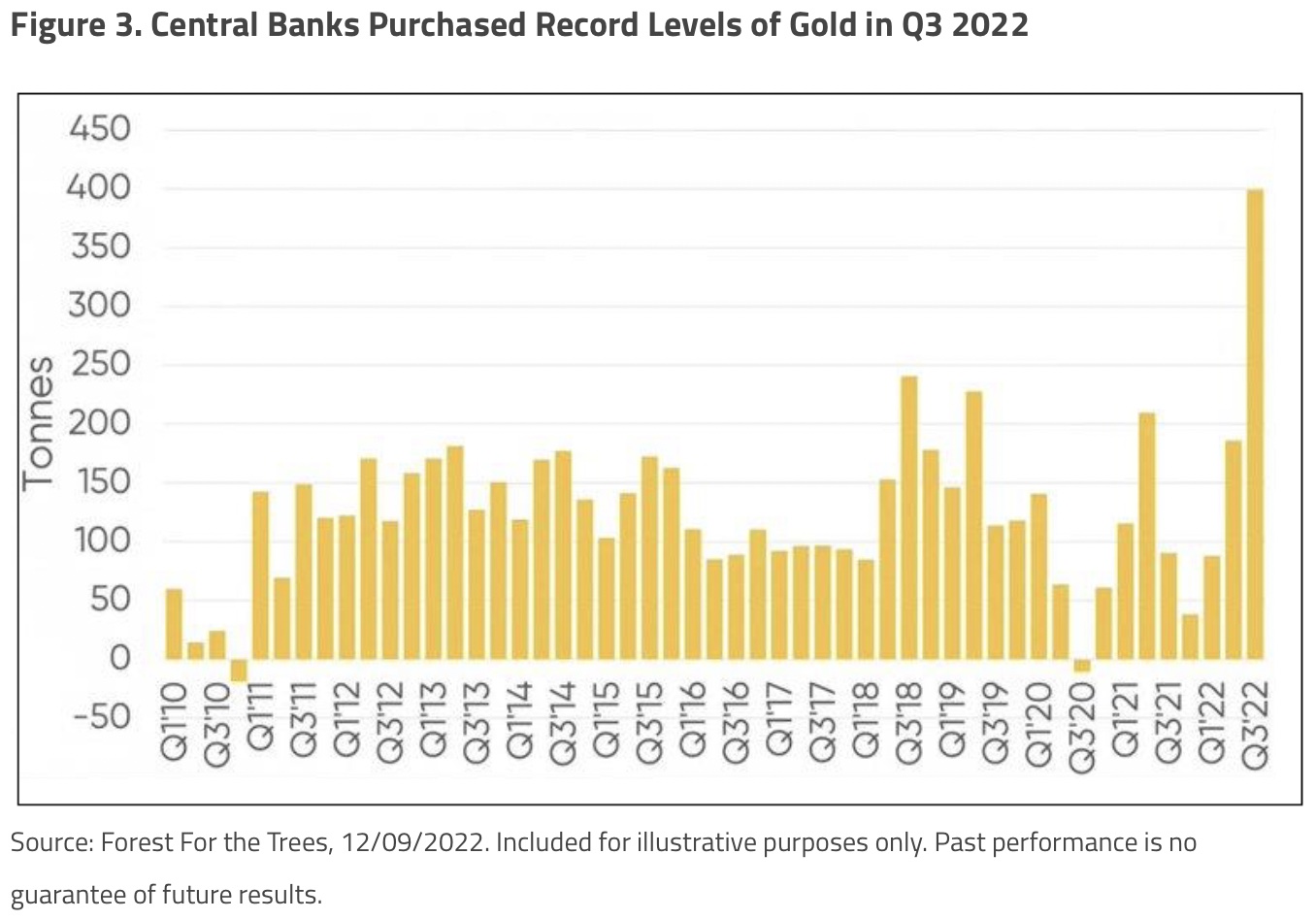

As noted by Luke Gromen (Forest For the Trees, 12/09/22), central banks sold $424 billion of their holdings of U.S. Treasuries through the first nine months of 2022 while buying record amounts of gold in Q3 2022.

Geopolitical developments suggest that the “strong dollar” investment proposition is deeply flawed, irrespective of hawkish Fed intentions. Perhaps Poszar is correct in predicting a bleak future and diminished relevance for central bankers and monetary policy.

A Brighter Note: Structural Gold Market Changes Could Enhance Gold’s Monetary Status

Gold trading has been handicapped by an archaic, even medieval, market structure that has diminished the metal’s utility as fungible collateral similar to U.S. Treasuries. Note that under the Basel III banking accord, gold is not considered to be a high-quality liquid asset (HQLA) for purposes of evaluating a particular institution’s financial strength. Since 2018, the FMSB (Financial Markets Standards Board), a not-for-profit market-led standards body, has presided over a Precious Metals Working Group which consists of entities including the World Gold Council (WGC), London Bullion Market Association (LBMA), global banks, and financial market associations. The objective of the working group has been to identify potential enhancements to the global gold market focusing on robust market infrastructure, increased data transparency and post-trade effectiveness.

Major banks active in the gold market including J.P. Morgan, HSBC, UBS and Deutsche Bank are members of the FMSB and will be familiar with all Standards and Spotlight Reviews that have been drafted by the Precious Metals Working Group and the observations made as to potential reforms to be implemented across the OTC gold market.

Successful modernization of the gold market structure could advance gold’s status to become a widely used reserve asset such that it would have transactional utility similar to liquid national currencies and other safe assets such as treasuries. Important to this effort is the employment of technology to digitize the universe of physical gold bars to enhance uniformity, liquidity, and transparency. Success would activate demand that does not now exist.

A preponderance of gold investors (with a Western capital market mindset) seem to position gold mainly as an expression, in one way or another, as a form of antipathy to fiat currencies and related negative consequences. (We plead guilty to that charge.)

Few imagine or perceive a constructive investment case for gold. For most, the virtues of gold’s potential as a liquid, borderless safe asset is mainly an abstraction because it has been written out of the monetary script for nearly a century. A plausible path to restore its historical function seems impossible to imagine.

An understanding of how the market reforms observed by the FMSB will be implemented, barriers to overcome, milestones, and timelines to achieve this could help free existing investors from depending on gloomy macroeconomic speculation to rationalize their exposure. More importantly, a clear understanding might attract a wider audience of mainstream investors who have avoided gold altogether because they perceive it as the third rail of perpetual pessimism…

This Is Now The Premier Gold Exploration Company In Quebec With Massive Upside Potential For Shareholders click here or on the image below.

As might be imagined, the timeline for such reforms, given the necessary involvement of many stakeholders including banks and potential regulators, is impossibly imprecise. Nevertheless, it is important to recognize that important and painstaking work towards these goals has been underway for years, and it is in the self-interest of all participants in the gold industry for this effort to succeed. From our perspective, success would on balance diminish reliance on fiat currencies and in the process, improve price discovery, and potentially lead to a permanently higher price.

Conclusion: Breaking the Ranks of Groupthink to Embrace Gold

Precious metals are underowned and out of favor despite their strong relative and absolute performance in 2022. Most gold and silver mining stocks provided decent but not compelling relative performance last year. However, investors should remember that mining shares trade as long-duration options on higher gold and silver prices. For this reason, they provide investment performance leverage relative to intermediate to longer-term directional moves in the metal price.

We believe a positive shift in money flows in 2023 will be driven by a deeper and longer-than-expected recession, a panic-driven shift to monetary ease, a further decline in the U.S. dollar and a continuation of the bear market in financial assets. Moreover, secular U.S. dollar weakness may be supported by longer-term structural shifts in the global currency and trading arrangements owing to geopolitical considerations and the eventual modernization of gold trading.

We believe gold bullion and gold mining shares registered a major bottom in Q4 2022. As flagged by Fred Hickey (High Tech Strategist, 11/2/22), whenever COMEX Managed Money short positions approach 35% of open interest, as was the case in September 2022, significant rallies may follow:

Many investors still appear to be mired in nursing their wounds from 2022. They may be understandably shellshocked and paralyzed, engrossed in postmortems, or too distracted to understand the root causes of their misfortune. Most likely, they are seeking solace and hope that a rebound lies just ahead. Only a few will investigate the merits of gold exposure, but those investors who seize the opportunity presented by inexpensive, unloved gold mining equities, we believe, will have the potential to reap substantial benefits from breaking the ranks of groupthink.

ALSO JUST RELEASED: Greyerz Just Warned Investors To Prepare For A Hyperinflationary Collapse CLICK HERE.

ALSO JUST RELEASED: Greyerz – The Clear Path For The World Is Now Full-Blown Collapse CLICK HERE.

***To listen to Alasdair Macleod discuss what is happening in Asia as well as what Russia is up to in the gold market along with what surprises to expect as we kickoff 2023 CLICK HERE OR ON THE IMAGE BELOW.

© 2023 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.