Here is an important preview of what to expect in 2023.

Strong Demand-Supply Fundamentals for 2023

February 20 (King World News) – Paul Wong, Market Strategist at Sprott Asset Management and Jabob White at Sprott: As 2022 ended, most of the main bearish risks for the U.S. (rising interest rates), EU (cold winter), and China (zero-COVID) faded suddenly and nearly simultaneously, setting the market for a more pro-cyclical outlook. The upward revision in global growth, the timing effect of the China credit impulse and the surprise ending of China’s zero-COVID policy have provided a tailwind for the metals market. For energy transition metals, we see this as a cyclical boost on top of the robust secular demand that is in play. If 2022’s pullback was the typical mid-cycle correction common in the commodity resource sector, then we believe 2023 will reaffirm the demand (strong) and supply (shortages) fundamentals.

The Russian invasion of Ukraine, the LME nickel short squeeze, systemic negative macroeconomic factors, etc., all affected energy transition materials in notable ways in 2022. Critical metals have attracted significant attention in the past few years despite plenty of short-term risks.

January, in particular, was a solid start to 2023. We believe we are in the early stages of an energy transition materials secular bull market and will likely have favorable supply-demand dynamics going forward.

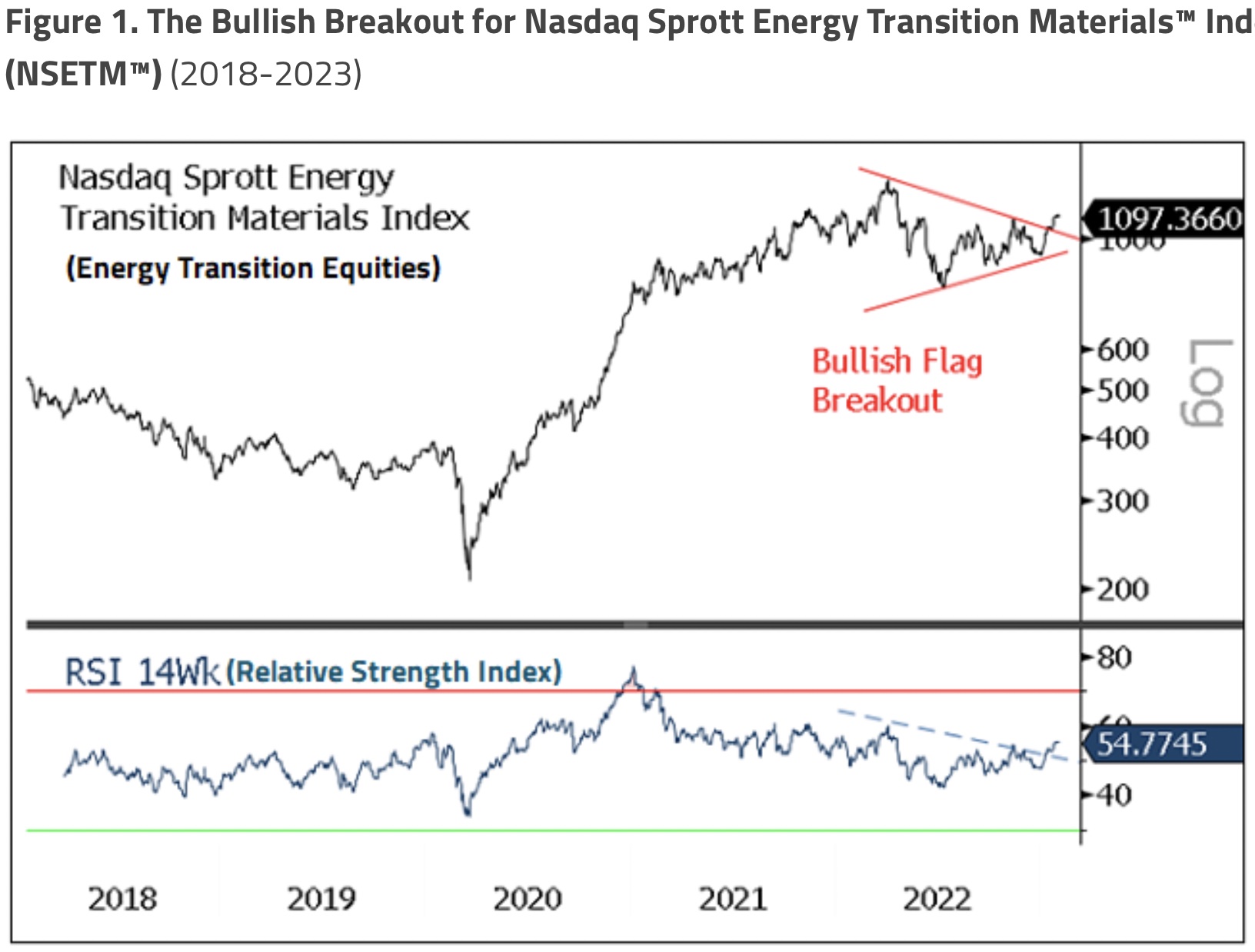

January Rebound for Energy Transition Materials

The Nasdaq Sprott Energy Transition Materials™ Index (NSETM™), a global equity index of selected energy transition materials industry equities, rebounded strongly by 17.51% for the month, outpacing most cyclical and resource sectors we track. NSETM™ and other mining and metals-related equities peaked around April 2022 as the Federal Reserve (“Fed”) embarked on aggressive rate hikes and China devalued the yuan. Both events signaled and pulled forward slowdown and recession risks. Market depth/liquidity at that time also declined, amplifying trade flows and exacerbating price swings. NSETM™ bottomed in July before other metals miners, but by late September, the Index began rallying into year-end as market conditions inflected (U.S. dollar [USD peak], Fed rate hike peak)…

This Company Has A Massive High-Grade Gold Project In Canada And Billionaire Eric Sprott Has A Huge Position! To Learn Which Company Click Here Or On The Image Below.

January was a solid month for risk assets as investment funds were underexposed for a positive, right-tail outcome. The significant left-tail risks of 2022 quickly faded or reversed as we headed toward the new year. In the U.S., fears of hyperinflation and more Federal Reserve (“Fed”) rate hikes abated as the Fed signaled it might slow its rate hikes just as inflation data finally moderated. (At this writing, the Fed indicated that it is likely to raise interest rates at least twice more, following much stronger-than-expected U.S. job growth in January.) In Europe, a far warmer-than-expected winter prevailed, allowing the EU to dodge the worst of an energy-spike-induced hard landing and associated stress events. After years of a strict zero-COVID policy, China quickly reversed to a full reopening, instantly giving the world an unexpected growth shock. With all three major economic regions experiencing a sudden reversal from left-tail (negative) to right-tail (positive) outcomes, massive forced buying was triggered.

Furthermore, with moderation in Fed rate hikes in sight, both the USD and interest rates declined sharply, easing financial conditions and paving the way in January for a rebound in many financial assets. Whether this rally is the beginning of the consensus-desired soft landing or yet another bear market rally remains to be seen. We expect that macro volatility will likely remain high in the months ahead. For the commodity resource sector, however, China’s reopening may help boost demand for commodities (and their related equities) so that they may experience a more substantial recovery relative to other cyclical sectors and industries.

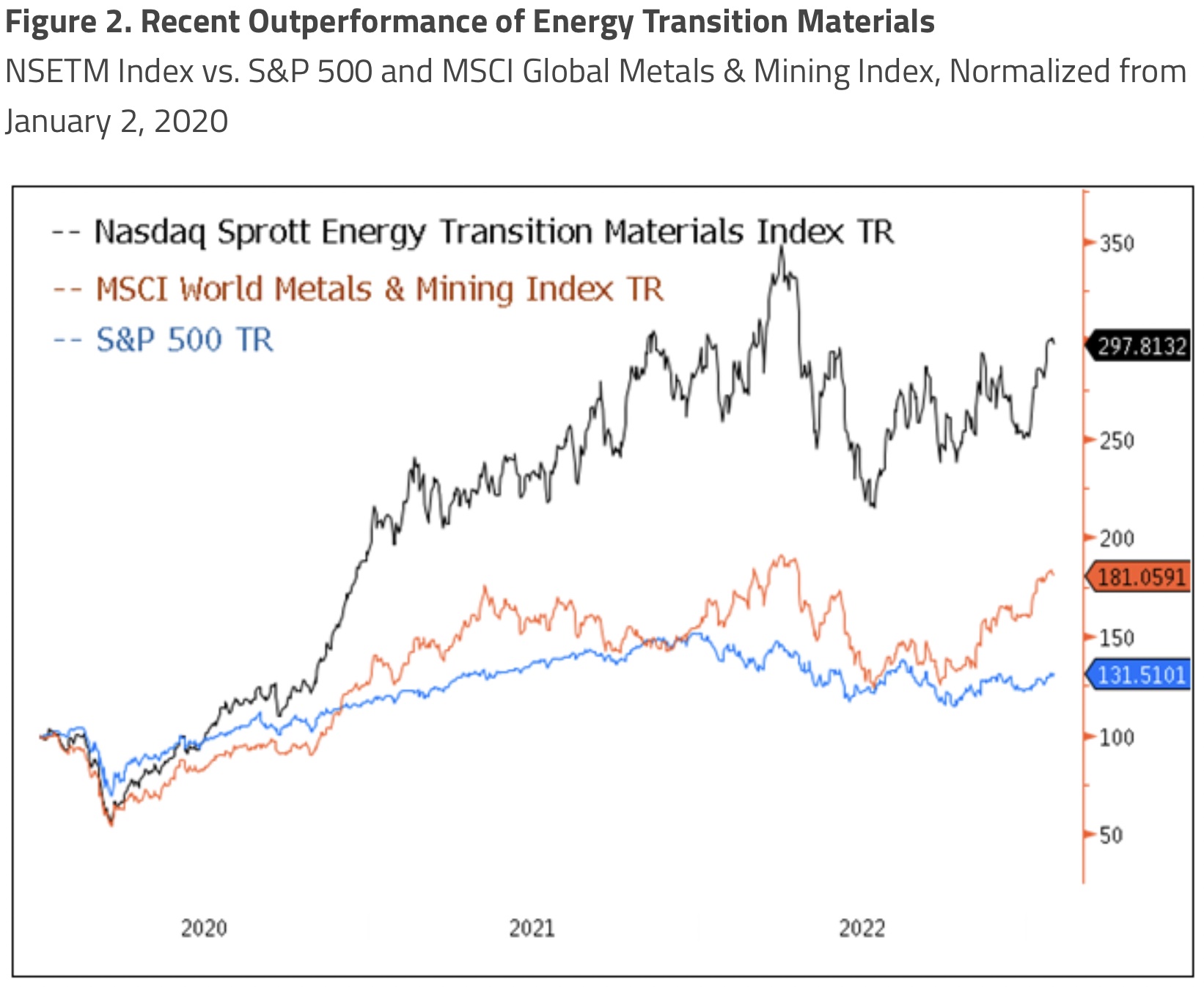

Energy Transition Equities Outperformance Since January 2020

In our 2023 Top 10 Watch List, we compared a basket of energy transition commodity metals to the Bloomberg Commodity Index (a broad commodity index) and the Bloomberg Industrial Metals Subindex (base metals) as a reality check. The energy transition commodities basket showed clear outperformance relative to both indices, confirming our bullish narrative for these physical metals.

In Figure 2, we compare the relative performance of the energy transition materials/mining equities (NSETM™) to the S&P 500 and the MSCI World Metals & Mining Index, with data normalized to a 100 index level starting January 2, 2020.

For the period from January 2, 2020, to February 13, 2023, NSETM™ (197.81%) outperformed the S&P 500 (31.52%) and the MSCI World Metals and Mining Index (81.06%) by considerable margins. In our view, the technical patterns support a continuation of this trend. Of note, NSETM™ and the MSCI World Metals and Mining Index have a high correlation (0.84 over the last five years) since they both represent metals mining equities, but NSETM™ has the added secular growth element of the energy transition.

Revisiting the Last Major Commodity Cycle

In Figure 3, we highlight the performance of the S&P 1500 Metals & Mining Index versus the S&P 500 Index back to 1995 (data limit) as a quick history review. For most of the 1990s, the metals and mining sector underperformed the broader equities market. In general terms, the metals group was still digesting the supply brought on by the past supercycle when additional supply arrived from the collapse of the Soviet Union in 1991. The technology group drove the broad market in the 1990s through the first tech growth boom, and valuation multiples expanded dramatically as interest rates fell in the first decade of the Great Moderation. The 2000s represented the most recent commodity supercycle, driven by the rise of China and its near-insatiable demand for commodities. Conversely, following the bursting of the dot-com bubble (2001), the technology group spent the decade losing value.

The 2010s saw China’s rate of gross domestic product (GDP) growth peak and its demand for commodities moderate. However, unlike past cycles, capital spending to maintain productive capacity was significantly reduced as capital was redirected more to share buybacks and dividends. The technology group began its next growth boom, and its valuations exploded even higher as the post-GFC (global financial crisis) world of QE-ZIRP-NIRP and low volatility fueled its startling rise in market capitalization…

This Is Now The Premier Gold Exploration Company In Quebec With Massive Upside Potential For Shareholders click here or on the image below.

Deglobalization and Geopolitical Tensions Have Accelerated the Energy Transition

The 2020s started with the COVID-19 pandemic, fiscal and monetary stimulus far outpacing the GFC response, the Russia-Ukraine war, and the resultant fracturing of global supply chains, geopolitical reordering, and global hyperinflation. The secular demand surge for critical minerals for energy transition was well underway due to the threat of climate change. But since the onset of the Russia-Ukraine war, deglobalization has accelerated and geopolitical tensions have risen. The need to quicken the global energy transition and secure critical minerals supplies has increased commensurately, and it comes on the heels of a decade that saw chronic underinvestment, which now magnifies the level of capital investment needed.

From an investment cycle perspective, we are likely in the early stages of this commodity supercycle. In the 2000s commodity supercycle, China joined the World Trade Organization in 2000, and commodity prices made their lows in the 2002 recession. Despite fantastic performance for the commodity complex in 2003 and 2004, it was not until 2005 that investment inflows began reaching the level that acknowledged that commodities were in a demand shock-driven market. We see a similar history being repeated now, and other resource sectors, such as energy, are demonstrating the same pattern. Investment consensus does not reflect that we are in a commodity supercycle based on the current level of absolute and relative fund flows.

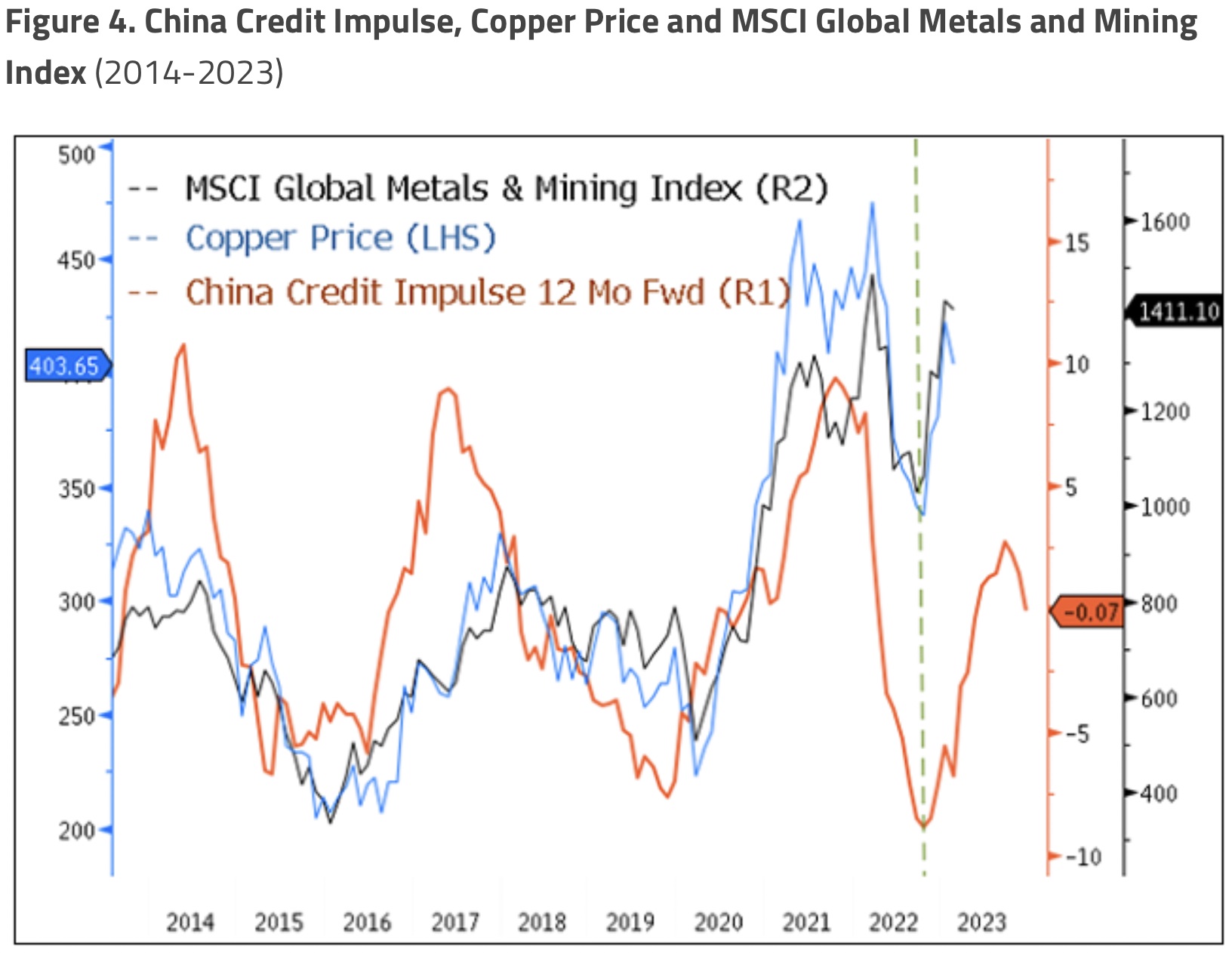

China Credit Impulse: A Closely Watched Leading Indicator for Metals Demand

China credit impulse refers to the change in the rate of growth of new credit in China created by banks and other financial institutions. Credit impulse is a leading indicator of economic activity, signaling potential economic changes in the future rather than current activity. An increasing credit impulse indicates that the rate of new credit growth is expanding, while a decreasing credit impulse indicates that the credit growth is slowing or contracting.

China’s credit impulse is a closely watched leading indicator of economic activity, as credit growth is closely tied to investment and consumption, leading to higher demand for metals and other commodities. A falling credit impulse would warn of a slowdown, contraction, and lower demand for metals. Although the lead time for the credit impulse to affect the economy can vary, we use a 12-14 months rule of thumb for metals commodities. China accounts for roughly 50-60% of overall metals demand, and how it expands/slows credit creates a boom-bust effect.

China is the biggest consumer of virtually every commodity and has an outsized pricing effect due to its binary approach to stimulus. While China’s impact may change in the future due to growing metals demand in the energy transition and further deglobalization, China will dominate in the short term. In Figure 4, we plotted the China credit impulse 12 months forward. We then overlaid the copper price and the MSCI Global Metals and Mining Index to illustrate this lead indicator’s usefulness over the past decade.

The Early Stages of an Energy Transition Materials Bull Market

China’s credit impulse is not the only factor that affects metals prices. Many other factors can impact the supply and demand for metals, such as the overall global economy and geopolitical events. Although the demand growth rate for critical metals essential for the energy transition is expected to be high, these metals have other uses beyond the energy transition that are impacted by the economic cycle. In other words, the secular growth trend of critical metals can be amplified during a global cyclical economic upswing.

In the most recent case, China’s reopening after ending its zero-COVID policy can add further demand on top of the secular and cyclical forces. The demand growth rate for critical metals for the energy transition (EVs, solar, nuclear, wind, etc.) is expected to increase over the next decade. However, the demand growth rate can vary depending on factors such as government policies, technological advancements, and geopolitics…

ALERT:

This company is about to start drilling what could be one of the largest gold discoveries in history! CLICK HERE OR ON THE IMAGE BELOW TO LEARN MORE.

Update on Critical Materials

Here we discuss some of the primary metals driving the global energy transition.

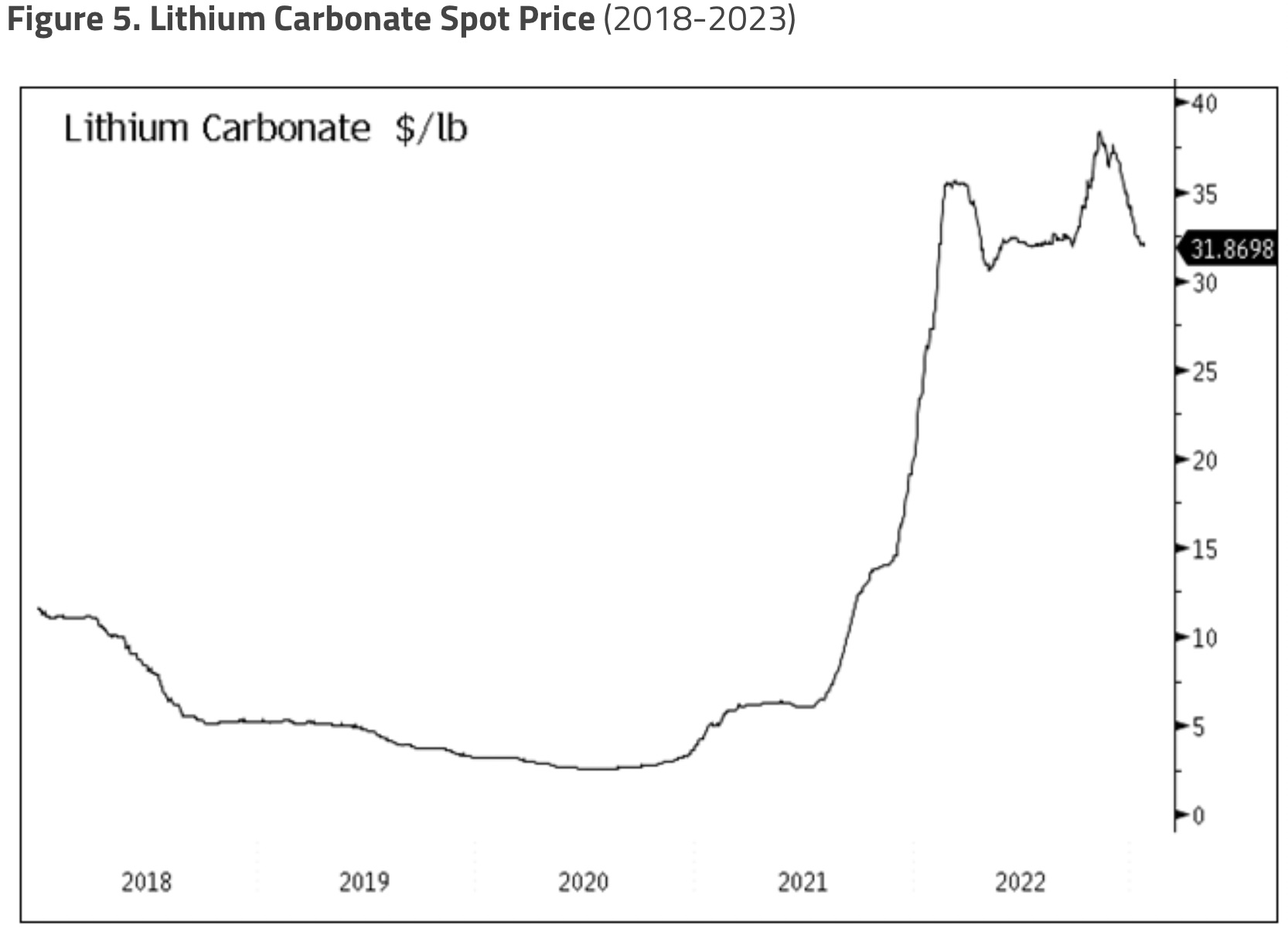

Lithium: Exponential Demand

As shown in Figure 5, the price of lithium had a meteoric rise in 2021 and 2022 making it the best performing commodity over the period. Lithium is essential for the lithium-ion batteries used in electric vehicles (EVs) and consumer goods, representing most of the demand for this critical mineral. Over recent years, the growth in the EV industry has been exponential and drove the lithium market balance into a deficit. Lithium prices skyrocketed with no available substitutes, inadequate supply, and inelastic demand.

More recently, lithium prices have entered a consolidation range after nearly quintupling in price since mid-2021. Some softness in consumer spending has weighed on lithium demand in the short run. Forecasts for 2023 by investment banks and other price forecasters have also been mixed. Some estimate that the lithium market will be in surplus for 2023, while others site supply challenges (i.e., longer lead times) that will result in a supply deficit. Nevertheless, lithium demand is expected to grow substantially in the long run to meet EV demand, and we believe supply is unlikely to keep up.

Uranium: New Bull Market in Development

As shown in Figure 6, the uranium bull market has continued its significant progression, excluding the volatility induced by the Russia-Ukraine war. This latest bull market has been defined by the global government’s recognition of uranium’s dual role in the energy transition and energy security. Renewable energy sources have seen considerable investments, but only recently has sentiment toward nuclear energy, and thereby uranium, significantly improved…

To Find Out Which Uranium Company Is Positioning Itself To Become A Powerhouse In Nevada Click Here Or On The Image Below.

Nuclear energy has a very low full-cycle carbon footprint and is the most reliable baseload energy source. Renewable energy has much lower capacity factors than nuclear, and therefore nuclear energy has begun to see increased government attention with its ability to offset this intermittency. There has been an unprecedented number of announcements for nuclear power plant restarts, life extensions, and new builds, which are likely to create additional demand for uranium. Supply levels remain constrained given that western utilities are no longer contracting with Russian suppliers, inventory levels are reduced, and the current uranium price remains below incentive levels to restart tier 2 production.

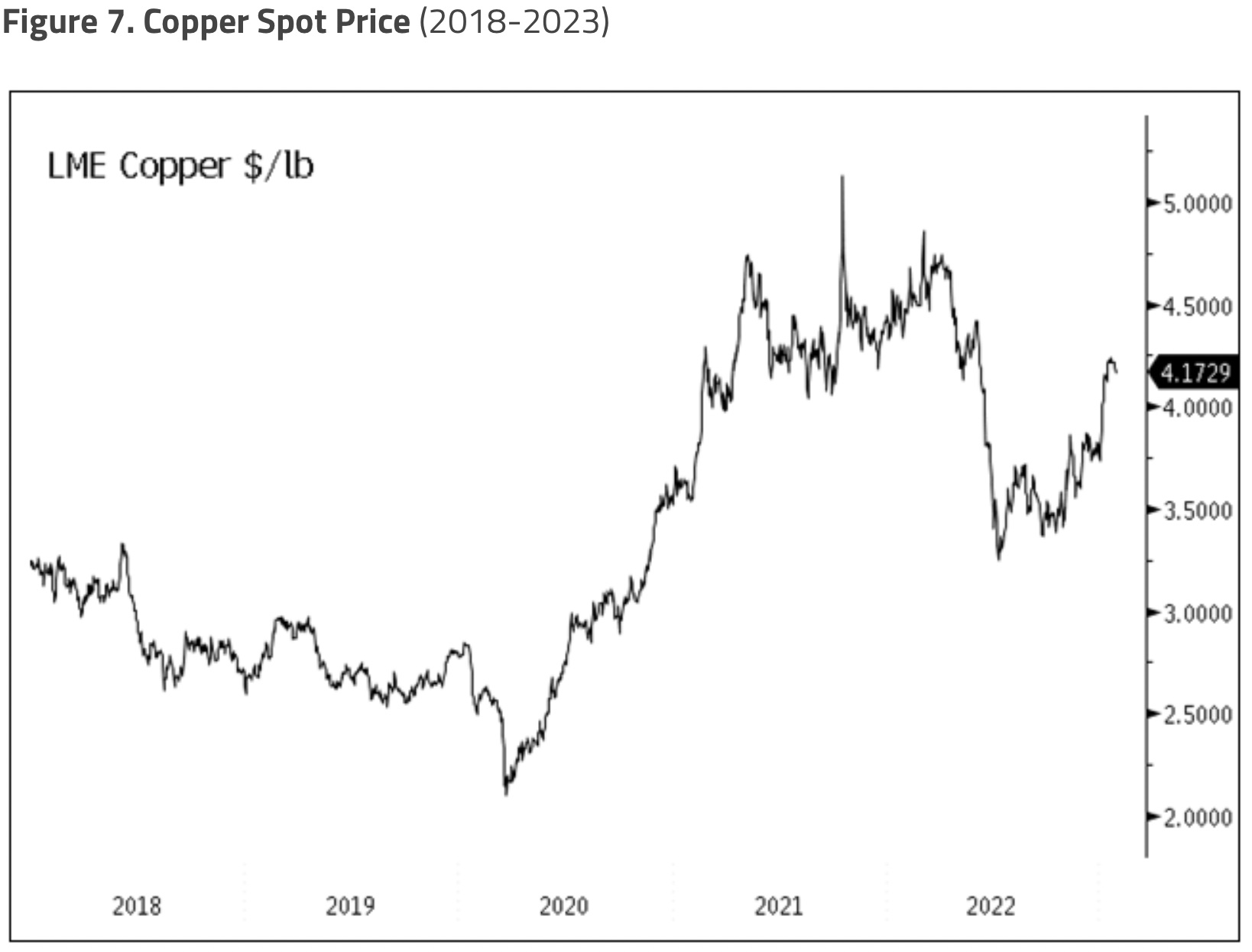

Copper: Positive Macro and Structural Demand

Copper has many uses in the global economy and is tied more closely to macroeconomic trends than other energy transition materials. Copper is cyclical and has benefitted from the reversal of the 2022 strong USD and the forecasted slowing of Fed interest rate hikes. China is by far the largest consumer of copper, and the reversal of its zero-COVID policy to full reopening has acted as a tailwind for the metal.

Looking ahead, increased demand for copper is expected to be fueled by the global energy transition. Copper is critical for conducting electricity in renewable energy sources, including wind and solar, but especially for electric vehicles and electricity grid investments. We believe that the additional demand expected from energy transition needs, a disruptable supply chain, low copper inventories, and declining ore grades may lead this market into a supply-demand deficit in the future.

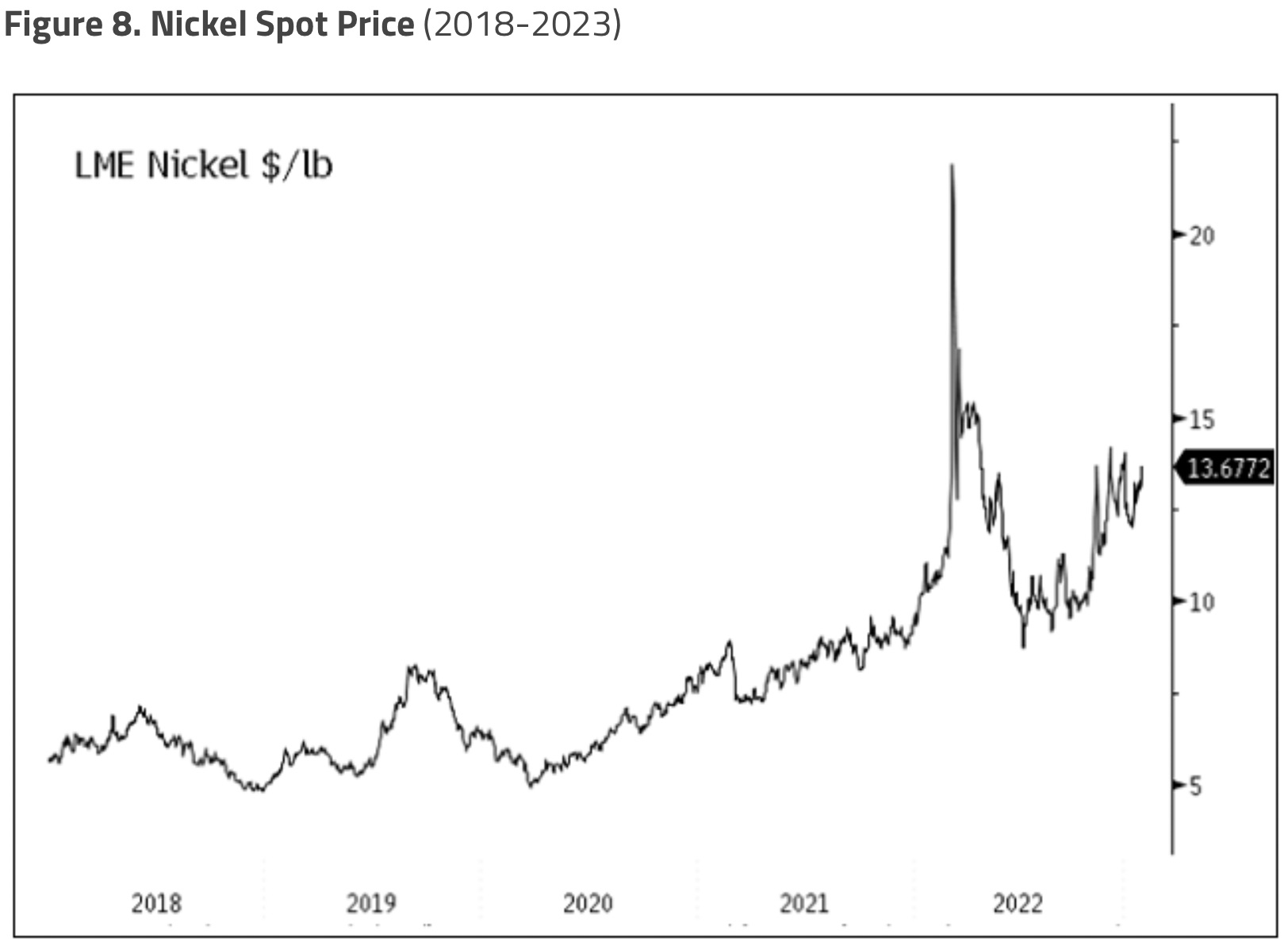

Nickel: Prices Returning to Fundamentals

As shown in Figure 8, nickel has been in a significant uptrend in the past couple of years, excluding the volatility induced by the historic short squeeze on the London Metal Exchange’s nickel market in March 2022. Currently, nickel’s demand primarily comes from stainless steel. However, batteries are the most significant demand growth driver, given that nickel is a critical mineral for NMC cathodes. NMC refers to Lithium-Nickel-Manganese-Cobalt-Oxide (LiNiMnCoO2), the preferred cathode powder for electric batteries.

NMC cathodes are used for power tools, e-bikes, and other electric powertrains and are considered a superior option for automotive batteries. NCM cathodes have a higher energy density than alternatives, allowing more energy to be stored and the EV car to have a greater range. Supply is divided into Class I, which is of higher nickel content and can be used for batteries, and Class II nickel, which is mainly used for stainless steel. In January, an additional supply of Class I nickel was announced by a major private company’s idle copper plants, and this slightly weighed on the nickel price. In the long run, we believe it is likely that the Class 1 nickel market will be in a deficit due to the significant demand from batteries and the transition to higher nickel content chemistries.

A New Supercycle for Commodities

We believe the post-pandemic era marks the beginning of a new supercycle for commodities, especially for critical minerals driving the clean energy transition. Investment opportunities presented by the clean energy transition will likely center around the critical minerals vital to powering the planet through low-carbon energy sources and revolutionizing the transportation sector through the electrification of the world’s vehicle fleet.

Escalating geopolitical tension and the need for governments to re-shore supply chains and production to ensure industrial security have helped to accelerate the transition, which will be commodity- and capital-intensive. We foresee a demand shock for commodities, particularly critical materials.

ALSO JUST RELEASED: NEW WORLD ORDER: This Collapse Will Be Breathtaking And Will Lead To Great Reset CLICK HERE.

ALSO JUST RELEASED: What’s Happening Now Is Exactly What Happened Before 2008 Panic & Dot-Com Bust CLICK HERE.

ALSO JUST RELEASED: Gold Has Been Pouring Out Of COMEX, Who Knows What’s Happening In London? CLICK HERE.

***To listen to Gerald Celente tell you what the mainstream media won’t CLICK HERE OR ON THE IMAGE BELOW.

***To listen to Alasdair Macleod discuss gold disappearing out of COMEX vaults as well as what’s happening with the Russians and much more CLICK HERE OR ON THE IMAGE BELOW.

© 2023 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.