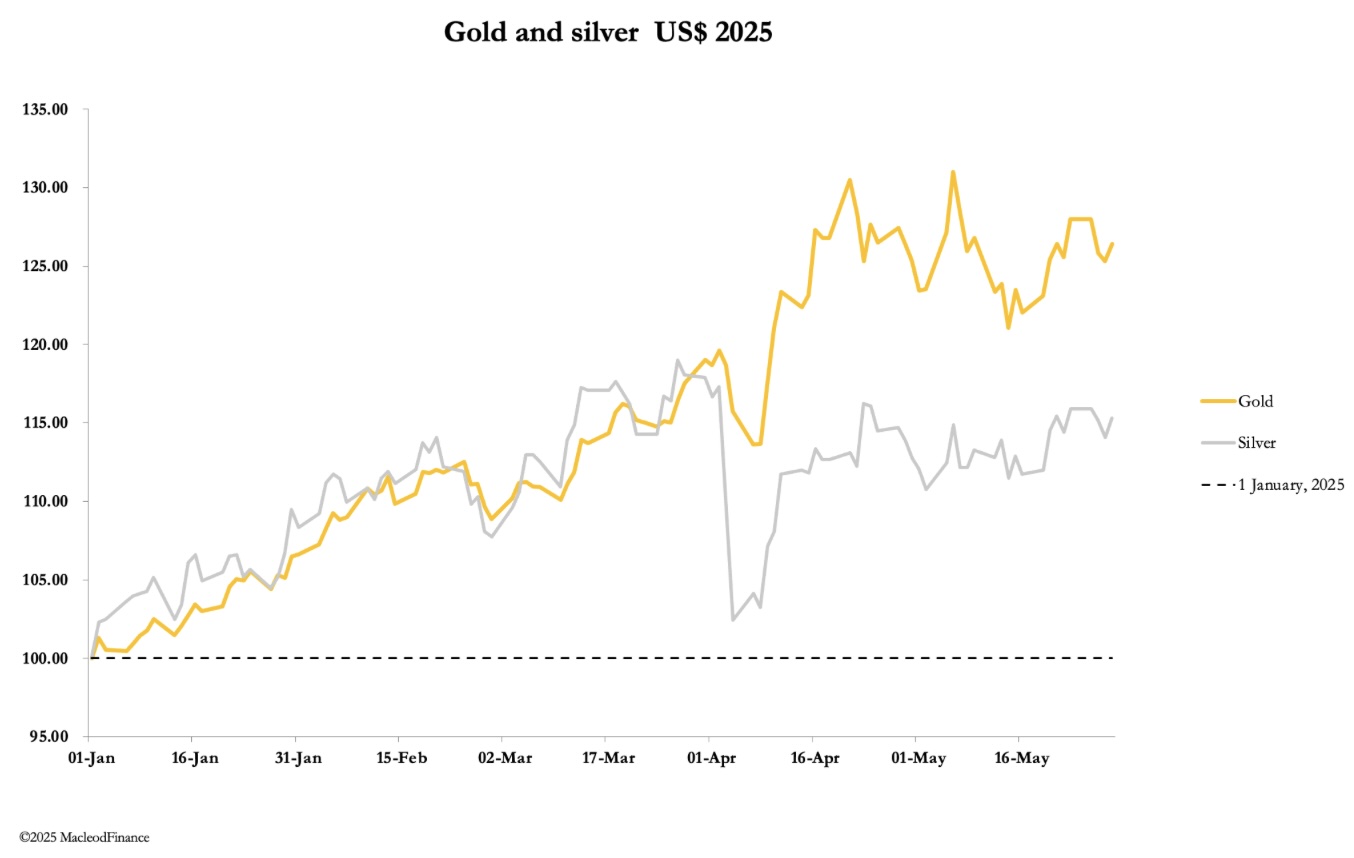

1Gold and silver consolidation continues but look at this…

Due to unforeseen travel complications there will be no audio interviews this weekend, but they will resume next week! Thank you for your patience and loyalty. For now…

May 30 (King World News) – Alasdair Macleod: Wholesale market operators who rely on being able to roll leases on maturity face the prospect of having to buy back bullion which has simply vanished.

In a week when the US Court of International Trade ruled that the constitution gave congress the power to levy tariffs and not the president, gold and silver sailed on more or less regardless. In European trade this morning, gold was $3295, unchanged from last Friday’s close. Silver was $33.17, up 12 cents. Trade was quiet in a short week due to public holidays on Monday in London and the US.

Furthermore, this week Comex June contracts were running off the board, which together with option expiry is usually a time of price weakness as traders with long positions and call options sell or abandon them respectively, resulting in sell-offs. They didn’t happen.

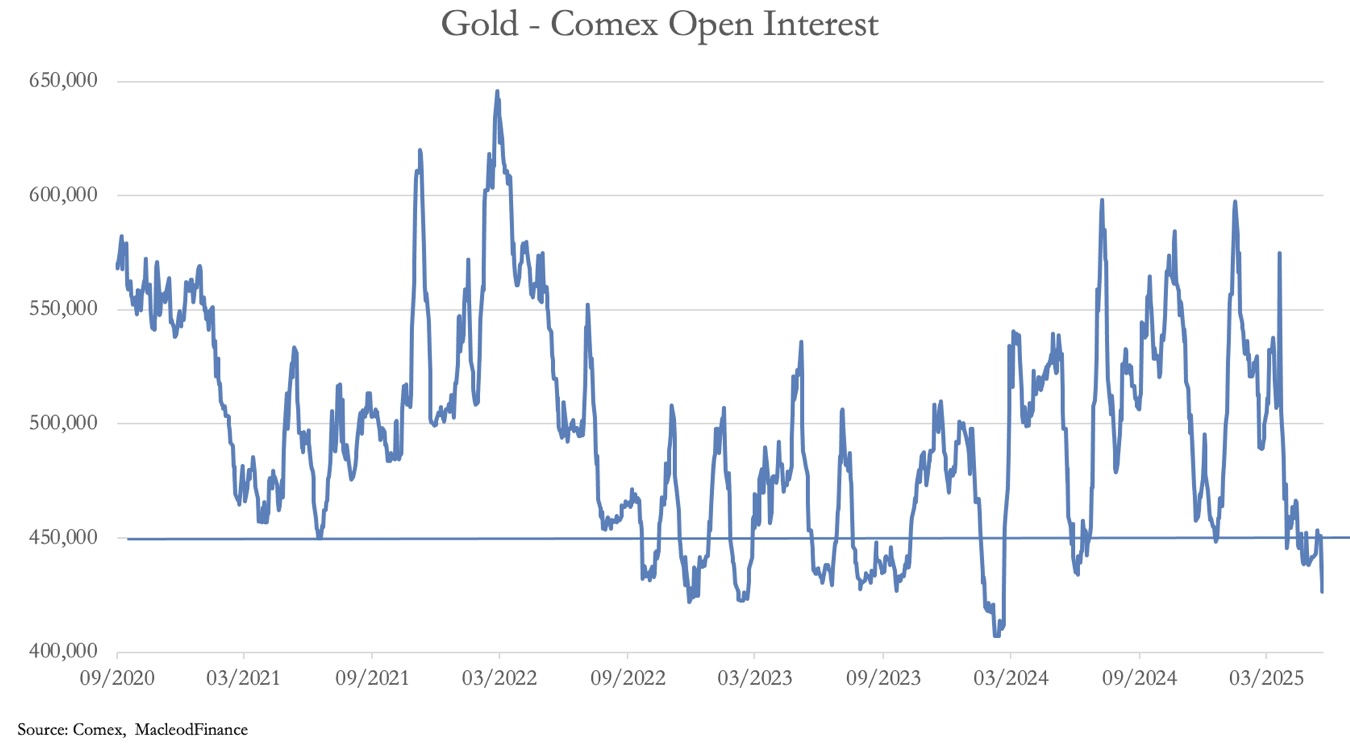

Judging by Comex data, gold is actually oversold with open interest the lowest it has been since February 2024.

Attempts by the shorts to shake out weak longs were futile because there aren’t any. And the stands-for-delivery continue at pace at 640.5 tonnes this year so far, an annual rate of 1,540 tonnes. It is beginning to eat into Comex stocks which have declined by over 195 tonnes since the all-time peak on 3 April — the day after Trump’s so-called liberation day:

Recall that some of that gold was extracted from the Bank of England’s vault, whose bullion stocks since October declined by 437 tonnes to end-April. We can be certain that much of this gold was leased by bullion banks from BoE central bank customers. And that this gold has been delivered into unknown hands through Comex stand-for-deliveries.

This is a radical departure from the Bank’s ledger transfer system, whereby gold remains stored at the Bank irrespective of ownership. Central banks leasing gold are now aware that gold which they have leased out has effectively disappeared with no firm guarantee that it will be replaced by the lessors when leases end.

The scale of the problem, real or imagined, is enough to persuade central banks with earmarked gold in London and New York to withdraw from all gold leasing activities. This gives both forward and futures markets a problem, because gold leasing is a major source of market liquidity.

Instead, wholesale market operators who rely on being able to roll leases on maturity face the prospect of having to buy back bullion which has simply vanished.

Doubtless, when the super-premiums on Comex triggered an arbitrage flow of over 870 tonnes into Comex warehouses from last October to April from London, Switzerland, and elsewhere the arbitrageurs thought only of the profits without the final transaction of buying back gold for paper. It really was a sucker’s trade of “you have the paper and we have the gold” variety.

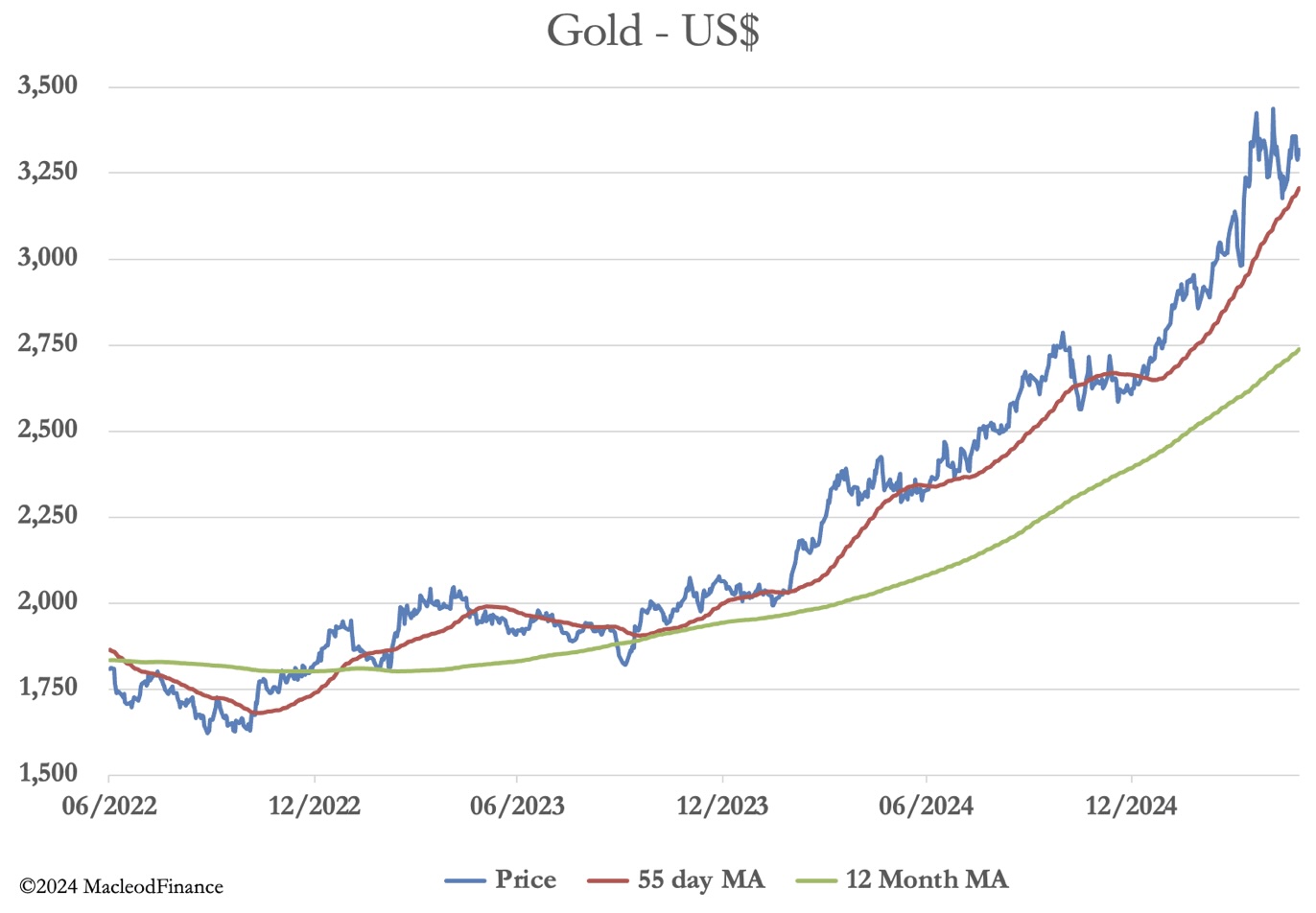

Meanwhile, with no flaky longs on Comex, if that’s any guide to other markets as leases expire and the scramble to buy bullion gets underway, the backstop must be to bail out the bullion banks. The chart below illustrates the technical background, which offers no comfort to the shorts:

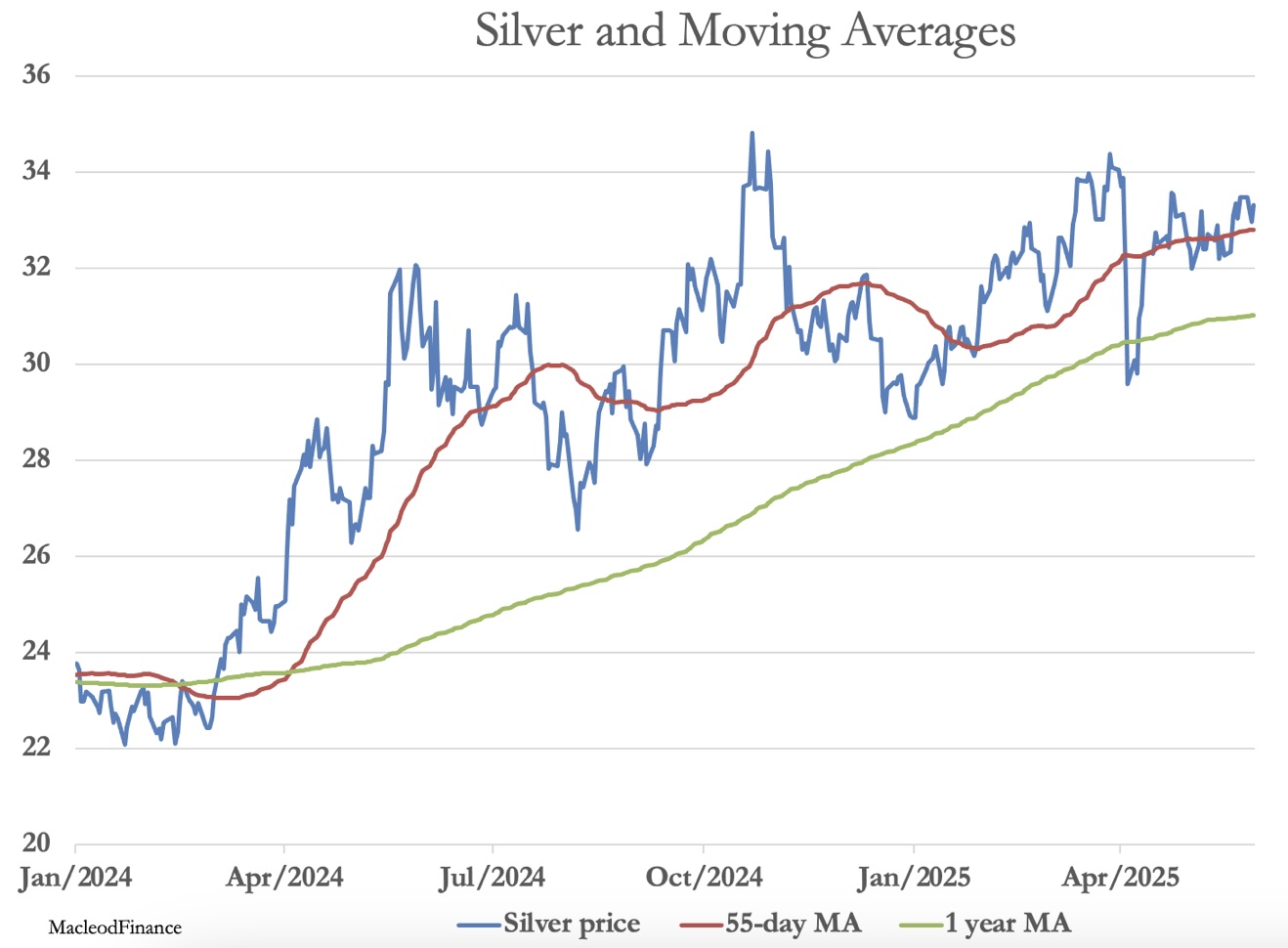

The chart suggests a liquidity crisis which is ongoing. And with the gold/silver ratio at 99, speculators are likely to chase silver to maximise profits as a crisis in gold paper markets unfolds. Silver’s chart is below:

© 2025 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.