The Fed is going to cut rates in 2024, but expect a lot of chaos in global markets. Here is why…

January 2 (King World News) – Peter Boockvar: “We always did feel the same. We just saw it from a different point of view. Tangled up in blue” sang Bob Dylan in the very last verse of this classic song. We can apply analysis to the same set of facts we all look at every day, both at the micro and macro level but have different approaches and many times come to different conclusions about what it means and where it maybe will eventual lead to.

I see the set up for 2024 as having a lot of potential big time trade offs. Nothing ever is smooth and I lay out here some of those possible puts and takes.

1)The Fed is going to cut overnight interest rates in 2024 but it’s possible that long term rates rise in response as markets would see the Fed pulling back from the inflation fight. The battle against inflation is being won with the rate of change slowing but there is no victory yet in the war as we need a sustainable drop in inflation, not a cyclical one. Also, the dollar should weaken further on rate cuts that then raises inflationary risks and could lead to a rise in commodity prices, particularly oil. And if the Fed is cutting because growth is faltering, the budget deficit blows out further, Treasury supply spikes, a problem in 2023 that is only going to get worse in 2024, and long rates jump. Also impacting long term rates is the BoJ finally getting out of NIRP which could lead to more bond market volatility on the long end.

2)Moderating inflation is obviously very positive for the consumer, especially as wage growth is still pretty good at around 4-5% but consumers live on the level of inflation, not its rate of change.

23)Also with receding inflation, on the corporate side revenue growth is going to slow as price increases become more difficult. Can double digit expected earnings growth estimates for 2024 can really be met as nominal GDP slows?

4)Lower interest rates is a definite pain reliever for those with debt but we still have about $750b of corporate debt needing to be refinanced in 2024, mostly investment grade, according to Goldman Sachs and $500b of commercial real estate debt according to Trepp. The new interest rates paid on these new loans will be notably higher than on the rates on the loans maturing. The trade off is that many small and medium sized businesses that have floating rate debt have already experienced the acute phase of higher interest rates over the past 18 months and should see at least some relief as the Fed cuts assuming SOFR follows.

5)If the Fed cuts 3 times as the dots say, it would be a modest reset in response to falling inflation but markets might be disappointed as that is not what is now priced in. If the Fed cuts 6 times as the market is pricing in, it’s because the unemployment rate is 4.5% or more which would most likely mean an economic recession and faltering earnings. Also, a REAL rate of about 250 bps used to be normal once upon a time.

6)If the economy doesn’t land and continues with decent growth, the Fed will barely cut rates, if at all, which is quite different than what the market is pricing in as stated and seen. Then, higher for longer will remain, which could eventually negatively impact the ‘decent growth.’

7)Can lower rates save us all? Maybe, but it didn’t save us in 2001-2002 nor in 2007-2009. And even 150 bps of cuts will still mean a 4% fed funds which is a far cry from zero.

8)QT continues on which is a good thing long term but by late Q1/early Q2 the Fed’s RRP could be empty which means the liquidity drag will really start to pick up.

9)A P/E market multiple of 21x 2024 eps estimates is VERY expensive with rates at current levels but there are many other parts of the market, such as small and medium sized stocks that are much cheaper as are many international markets. This for sure has been the case for some time but maybe that creates more bifurcation in 2024 in reverse and opportunities outside of the beloved stocks we all know too well.

10)The ECB, BoE and other foreign central banks will likely cut in 2024 but in response to both lower inflation and an economic recession.

Here are two other potential trade offs,

11)Service inflation continues to slow as the rent growth moderation shows up in the inflation stats but goods price inflation picks up again as goods inventories finally start getting rebuilt.

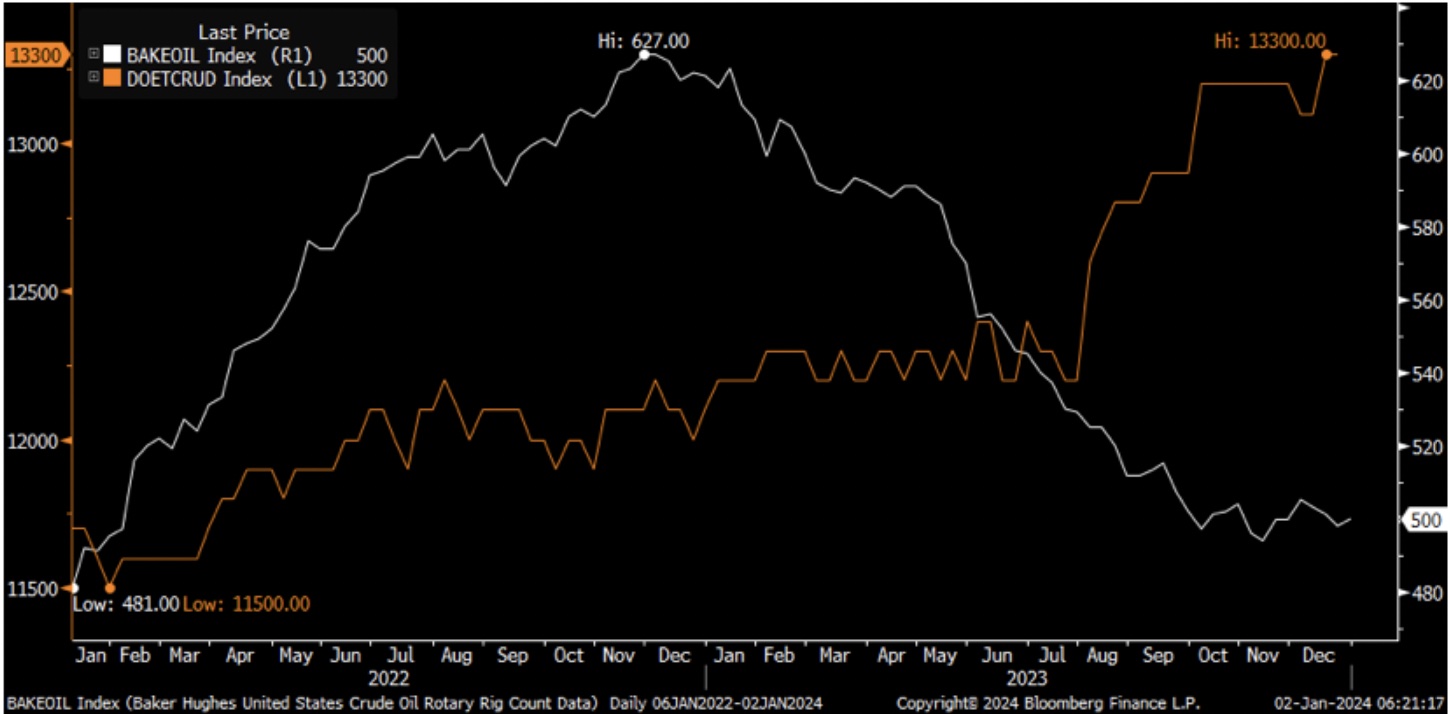

12)US oil production growth slows, after reaching record highs due to impressive efficiency gains, as the drop in the rig count eventually begins to matter. We’re still long energy stocks so I’m talking my book here.

US oil production in orange/US oil rig count in white

The December Eurozone manufacturing PMI was revised to a still very weak 44.4 from 44.2 initially and hasn’t been above 50 since June 2022. The UK manufacturing index was 46.2 vs 46.4 in the first December print but down 1 pt m/o/m and was last above 50 in July 2022.

Again with global manufacturing, the destocking seems to have mostly run its course but there are no signs yet that a restocking phase is soon to begin. It will though at some point.

To listen to Alasdair discuss how 2024 will kickoff for gold, silver, and the mining stocks CLICK HERE OR ON THE IMAGE BELOW.

© 2024 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.