Today one of the greats in the business warned there are so many sings of financial disaster showing across the world that there is very little time to prepare before all hell breaks loose.

So Many Open Signs of Financial Disaster Ahead and Gold Working

April 23 (King World News) – Matthew Piepenburg, partner at Matterhorn Asset Management: From oil markets to treasury stacking, backdoor QE, investor fantasy and hedge fund prepping, it’s becoming more and more clear that the big boys are bracing for disaster as gold stretches its legs for a rapid run north.

Recently, I dove into the cracks in the petrodollar as yet another symptom of a world turning its back on USTs and USDs.

Gold, of course, has a role in these headlines if one looks deep enough.

So, let’s look deeper.

Diving Deeper into the Oil Story

The headlines of late, for example, are all about “surprise” OPEC production cuts.

Why is this happening and what does it say about gold down the road?

First, let’s face the politics.

As noted many times, it seems US policy, on everything from short-sighted (suicidal?) sanctions to the “green initiative” makes just about zero sense in the real world, which is miles apart from the “keep-me-elected” fantasy-world of DC.

After all, energy, matters, which means oil matters…

Listen to the greatest Egon von Greyerz audio interview ever

by CLICKING HERE OR ON THE IMAGE BELOW.

But the current regime in DC has been losing friends in Saudi Arabia and cutting its prior and once admirable shale production outputs (think 2016-2020) in the US despite a world that still runs on black gold fighting against green politics.

The DC attack on shale may make the Greta Thunbergs happy, but let’s be blunt: It defies economic common sense.

Saudi, by cutting production, is now showing a still very much oil-dependent world it is not afraid of losing market share to the USA in the face of rising oil for the simple reason that the USA just aint got enough oil to fill the gap or flex its energy muscles.

In the meantime, Chinese demand for crude is peaking while Russian oil flows to the east (including to Japan) are hitting new highs at prices above the US-led price cap of $60/barrel.

If DC has any blunt realists (wrongly castigated as tree-killers) left, it will have to re-think its anti-oil policies and get back toward that recent era when US shale was responsible for 90% of total global oil supply growth.

If not, oil prices can and will spike, making Powell’s war on inflation even more of an open charade.

Speaking of inflation…

Ghana Oil-for-Gold Beats Inflation

When it comes to oil and the decades-long bully-effect of a usurious USD (See: Confessions of an Economic Hitman), we have argued countless times that a strong USD and an imposed petrodollar was gutting developing economies around the world.

We also warned that developing economies (spurned by global distrust of the Greenback in a post-Putin-sanction era of a weaponized reserve currency) would respond by turning their backs on US policies and its dollar.

In the old days, the US could export its inflation abroad. But those days, as we warned as early as March 2022, would be slowly but steadily coming to a hegemonic end.

Again, this does not mean (nod to the Brent Johnson) the end of the USD as a reserve currency, just the slow end of the USD as a trusted, used or effective currency.

Toward that slow but steady end, it’s perhaps worth noting that Ghana’s inflation rate has fallen from 156% to just over 60% since it began trading oil for gold rather than weaponized USDs.

Hmmm.

Gold Works Better than Inflated Greenbacks

The most obvious conclusion we can draw from such a predictable correlation is that gold seems to be working better than fiat dollars to fight/manage inflation, a fact we’ve been arguing for well…decades.

From India to China, Ghana, Malaysia, China and 37 other countries engaged in non-USD bilateral trade agreements, the inflation-infected USD is losing its place in more than just the critical oil trade.

Nations trapped in USD-denominated debt-traps (thanks to a rate-hiked and hence stronger and more expensive USD) are now finding ways to tie their exports (i.e., oil) to a more stable monetary asset (i.e., GOLD).

This, of course, makes me that much more confident that as the world moves closer to its global (and USD-driven) “Uh-Oh” moment, that the already-telegraphed Bretton Woods 2.0 will have to involve a new global order tied to something golden rather than just something fiat.

This, again, explains why so many of the world’s central banks are loading up on gold rather than Uncle Sam’s IOUs.

Gosh. Just see for yourself:

Ouch.

Uh-oh?

US Investors: Still High on Past Fantasy Rather than Current Reality

Sadly, however, the US in general, and US investors in particular, remain trapped in a spiral of cognitive dissonance and still believe today and tomorrow’s America is the America of magical leaders, deficits without tears and the balanced-budget honesty of the Eisenhower era.

That’s why the vast majority (and their consensus-think, safety-in-numbers advisors) are still huddling in correlated 60/40 stock bond allocations rather than physical gold according to a recent BofA survey of wealth “advisors.”

This always reminds me of a phrase circling around Tokyo just before the grotesquely inflated Nikkei bubble lost greater than 80% of its hot air in the crash of 1989, namely: “How can we get hurt if we’re all crossing the road at the same time?”

Well, a large swath of US investors (and their “advisors”) is about to find out how.

Doubling Down on Return Free Risk

This may explain why US households (a statistical term of art which includes hedge funds) have upped their allocations to USTs by 165% ($1.6T) since Q4 of 2022 at the same time that the rest of the world (see above) has been dumping them.

But in all fairness, this does make some sense, as higher rates in the US give investors in USTs (especially in short-duration/money market securities) a greater return than their checking or savings accounts.

Unfortunately, where the masses go is also where bubbles go; but as I like to remind: All bubbles pop.

Of course, when adjusted for inflation, these poor US investors are still getting a negative return on USTs.

Foreigners, of course, have stopped falling for this, but when Americans themselves get suckered en masse into this same bond-trap, they’re basically just paying an invisible tax while chipping away at GDP growth and unknowingly helping Uncle Sam finance his debt for free (namely: at a loss to themselves).

Crazy?

Yep.

Negative Returning IOUs—The Lesser of Evils

But why are hedge funds (i.e., the “smart money”) falling for this? Why are they loading up on USTs?

Because they see trouble ahead, and even a negative returning UST is safer (less evil) than a tanking S&P–and that’s exactly what the pros are bracing for/anticipating.

Waiting for a Market Bottom

In short: The big-boys are safe-havening today in negative-USTs so that they’ll have dry powder at hand to buy a pending and massive market bottom tomorrow.

Once they can buy a bottom, they too will dump Uncle Sam’s IOUs as the QE (along with inflation) kicks back to new highs thereafter.

And speaking of QE…

Backdoor QE: Coordinated and Synthetic Liquidity by Another Name

I have always endeavored to simplify the complex with big-picture common sense.

Toward this end, let’s keep it simple.

And the simple truth is this: With US debt at unprecedented and unsustainable levels, it is a matter of national survival to prevent bond yields—and hence bond-driven rather than Fed- “set” interest rates–from spiking.

Such a natural, and bond-driven spike, after all, would make Uncle Sam’s embarrassing debt too expensive to function.

Survival vs. Debate

Thus, and to repeat: Keeping bond yields controlled is not a matter of pundit debate but national survival.

Since bond yields spike when bond prices fall, it is thus a matter of sovereign survival to keep national bond prices at reasonably high levels.

This, however, is naturally impossible when bond demand (and hence price) is naturally sinking.

This natural reality opens the door to the un-natural “solution” wherein central banks un-naturally print trillions (“synthetic demand”) to buy their own bonds/debt.

Of course, this game is otherwise known as QE, or “Quantitative Easing”–that ironic euphemism for un-natural, anti-capitalist, anti-free market and anti-free-price-discovery Wall Street socialism whose inflationary consequences cause Main Street feudalism.

In short: QE has backstopped a modern system of central-bank-created lords and serfs.

Which one are you?

See why Thomas Jefferson and Andrew Jackson feared a Federal Reserve, which is neither “federal,” nor a solvent “reserve.”

The ironies, they do abound…

How Can there be QE if the Headlines Say QT?

But the official narrative and headlines are still telling us only stories of QT (Quantitative Tightening) rather than QE, so what’s the problem?

Well, as with just about everything from CPI data and transitory inflation memes to recession re-defining, the official narrative is not always the truthful narrative…

In fact, back-door or “hidden QE” is all around us, from the Fed bailing out/funding repo markets and dead regional banks to central banks making secret deals behind the scenes.

Although it’s not officially QE when the central bank of one country is buying the IOUs (bonds) of another country, it is more than likely that leading central banks are acting in a coordinated way to “QE each other’s debt,” a system which former Fed official, Kathleen Tyson, describes as a “Daisy Chain.”

And if we look at the IMF’s own data, we can connect the dots of this Daisy Chain with relative (rather than tin-foil-hatted) clarity.

Since Q4 of 2022, for example, overall FX reserves are now up by over $340B, the equivalent of over $100B per month of central bank QE by another name.

Toward that end, the math is simple, with: 1) GBP reserves up 10% (no surprise given the gilt implosion of Oct. 2022), JPY reserves up nearly 8%, EUR reserves up 7% and USD reserves only up only 0.5%.

Not only does this look like backdoor QE masquerading as “building excess reserves,” it looks to me, at least, like a coordinated attempt by DXY central banks to collectively weaken the 2022 USD which Powell’s rate hikes had made painfully too high for the rest of the world, a fact/pivot of which we warned throughout 2022.

Since the above G7 policies kicked in, the USD has fallen 11% into 2023 as the other DXY currencies (JPY, EUR and GBP) gave themselves a little backdoor/QE boost.

It seems, in short, that the need for artificial liquidity in a world thirsty for USDs found a clever way to weaken the relative strength (and cost) of that USD (and confront/tame skyrocketing volatility in USTs) without overtly requiring Powell to mouse-click dollars from his own laptop.

Why Markets Rise into a Recession

This unofficial but likely coordinated play to constructively weaken the USD among the big boys helps explain why the S&P has been rising into 2023 despite open indicators that the country is itself marching toward a recession.

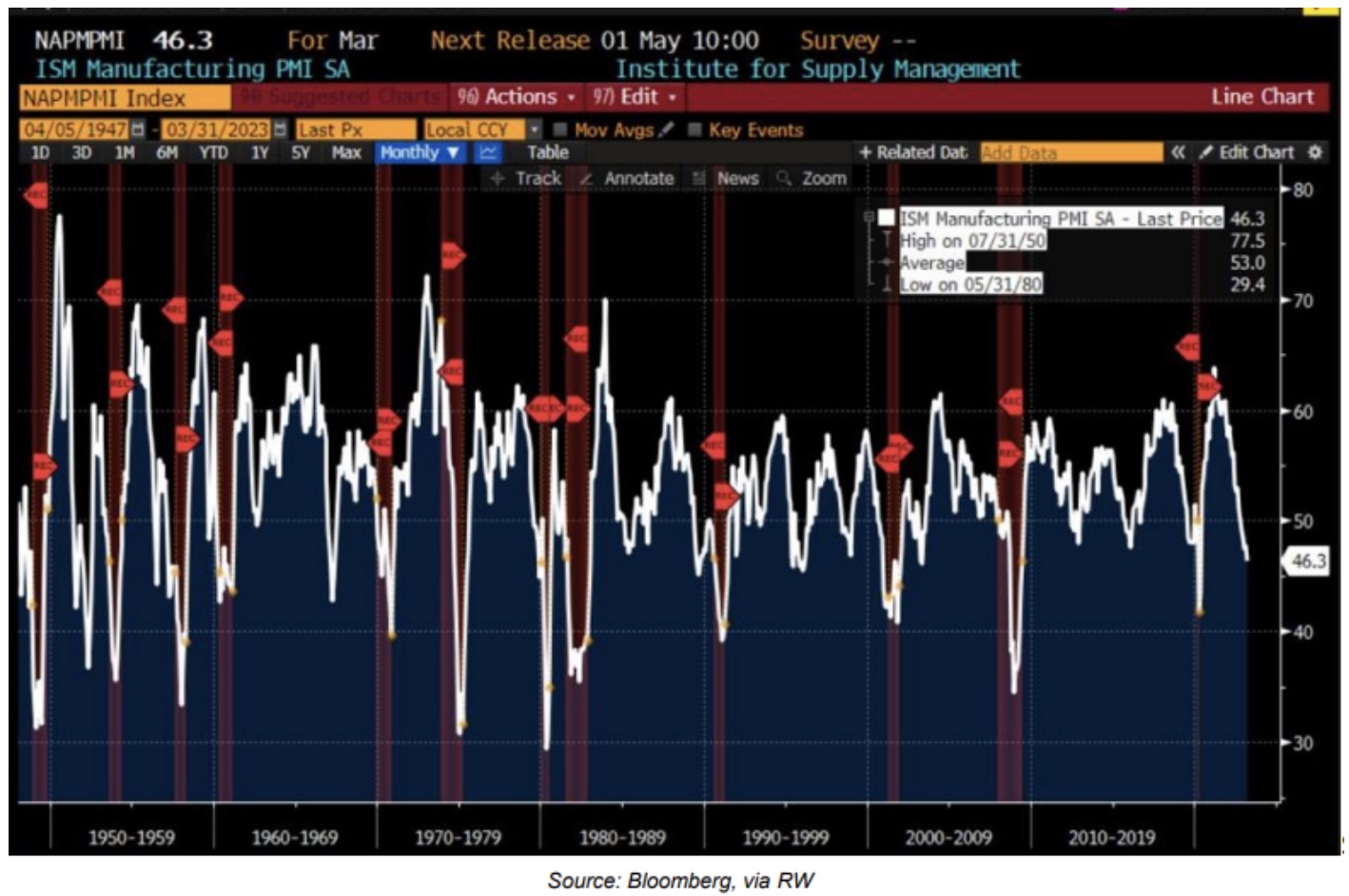

US Manufacturing data (ISM) is now at levels consistent with a recession…

Again: The ironies (and un-natural manipulations) abound.

Meanwhile, the Atlanta Fed’s GDPNow is down 1.5% from March’s 3.2% figure.

But hey, who needs growth, productivity, tax receipts or even a modicum of national economic health to keep a liquidity-supported stock market from defying reality—at least for now…

Waiting to Pay the Debt Piper…

Ultimately, of course, debt will get the last, cruel laugh, and with the US heading toward a deficit that is greater than 50% of GLOBAL GDP (!), I personally believe the Fed will need to return to its own money printer in a big way once this market charade ends in an historical “uh-oh” moment.

This seemingly inevitable return to mouse-click trillions (inflationary) will likely come after a deflationary implosion in equity assets currently supported by the foregoing tricks and fantasy rather than earnings and growth.

In the interim, and like those hedge fund jocks discussed above, we can only wait for things to get S&P ugly as gold, often sympathetic in the first hours of a market crash, rips toward all-time highs thereafter…Matthew Piepenburg’s powerful KWN audio interview has just been released and you can listen to it by CLICKING HERE OR ON THE IMAGE BELOW.

© 2023 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.