The public has been selling into gold’s rise, but here is the good news.

Gold Being Accumulated

February 9 (King World News) – Alasdair Macleod: Gold and silver moved sideways for yet another week, exhibiting a bullish undertone. In European trade this morning, gold was $2032, down $7 from last Friday, while silver was $22.62, almost unchanged on the week.

Silver

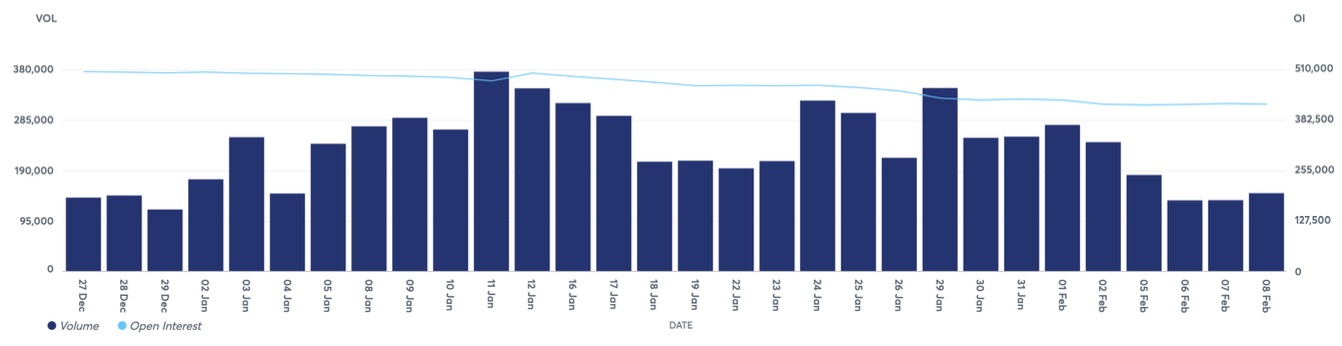

Silver volumes on Comex picked up to reasonable levels on bargain-hunting, while gold volumes were subdued, as the screenshot below illustrates.

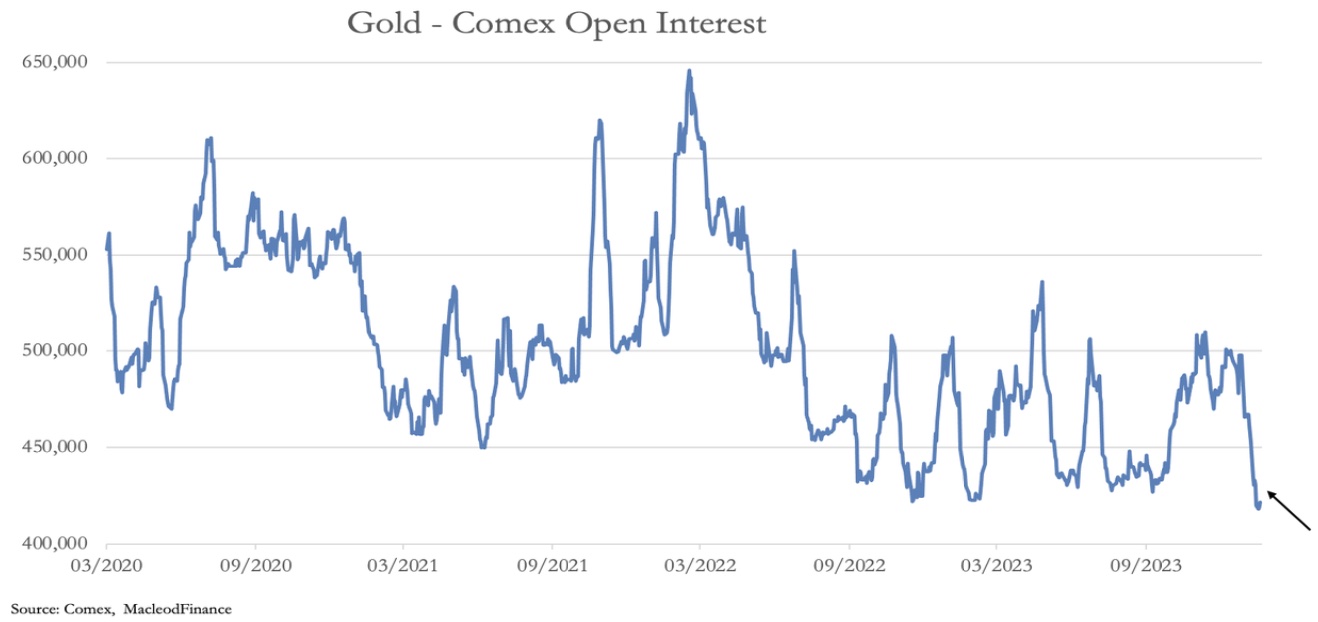

Open interest on Comex has collapsed as well, which suggests that Comex is no longer driving spot gold.

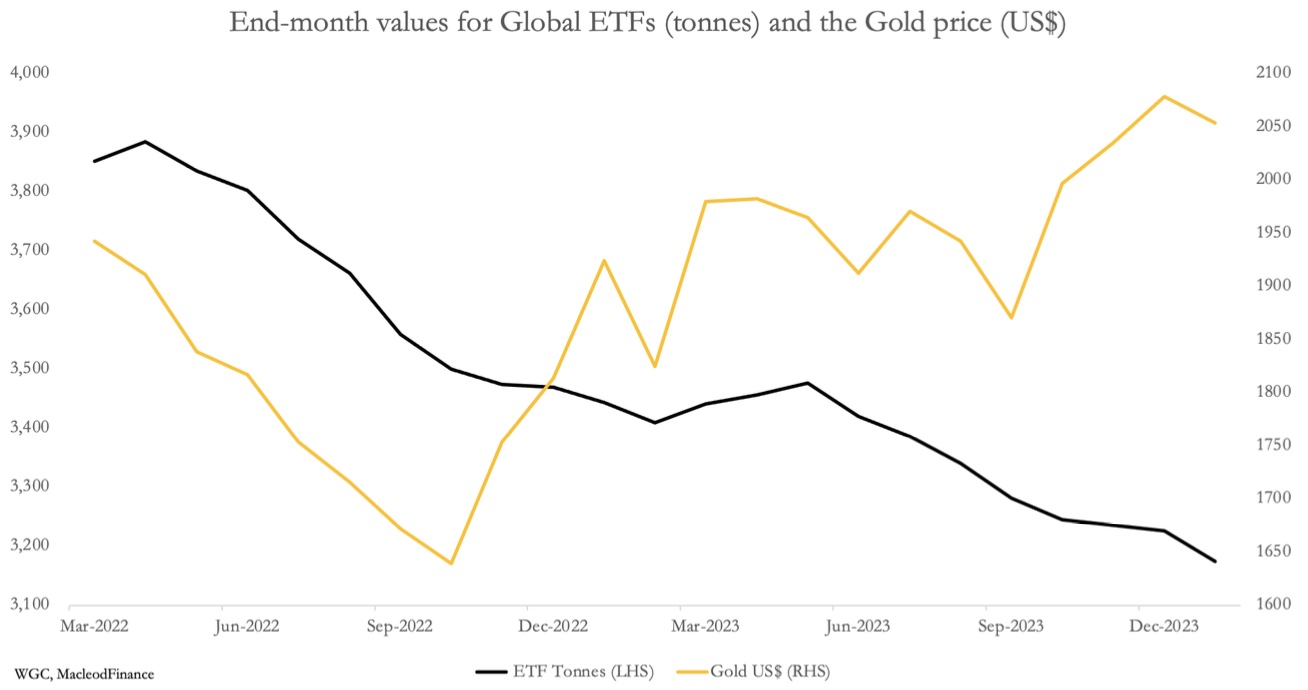

Indeed, with a stronger dollar’s trade-weighted index and US Treasury yields firming, these are the conditions which usually drive the gold price lower, particularly when there is so little public interest in gold. The next chart shows how public interest has diminished, reflected in liquidation of gold ETFs.

Public Selling Into Gold’s Rise

While the gold price has been rising, the public has been selling. And we can see from Comex Open Interest that demand is not emanating from paper markets either. But some categories of buying are accumulating bullion, driving up the price. We know that central banks have been increasing their holdings. To this, we can add an unknown factor: purchases by sovereign wealth funds and other government entities. But we don’t really know what is happening in London, which is about eight times the size of Comex. And we can be sure that Asian and Middle Eastern ultra-high net worth family funds are also buying, partly for geopolitical-driven diversity from dollars and euros.

With gold consolidating close to all-time highs, the indications are that the bullion banks in the LBMA are closing down their short positions. Bear in mind that the banks which oVer unallocated gold accounts do so on a fractional reserve basis. In other words, gold deposit liabilities are probably less than one-eighth covered by a combination of physical gold and over-the-counter derivatives. The point to note is that derivative liquidity is almost certainly drying up, driven partly by the lack of physical bullion availability, and partly by bullion bank traders sensing it is increasingly dangerous to be short.

For whatever reasons, the argument that rising bond yields detract from gold’s value is not holding. There may be a better argument in favour of the dollar’s trade weighted index, but that is comprised of a fiat currency cohort and doesn’t automatically reflect the relationship with gold. The next two charts show recent developments in bonds and the dollar’s TWI.

Clearly, this combination of rising bond yields and the TWI should be undermining gold. Gold’s resilience against these headwinds is remarkable and unexpected.

There is an additional factor coming into play, and that’s Chinese retail demand, which in December was reflected in withdrawals from the Shanghai Gold Exchange of 271 tonnes, the second highest on record (which was 285.5 tonnes in July 2015). Chinese citizens are facing a collapsing stock market and a property crisis. They cannot hedge out of renminbi because of exchange controls, so they can only buy gold.

It could be that December’s withdrawals were inflated by seasonal demand ahead of the Chinese New Year, which is tomorrow. But this demand contrasts sharply with western retail apathy, reflected in ETF net selling. Alasdair Macleod’s audio interview was just released discussing the Chinese public buying close to all-time record amounts of physical gold. To continue listening to Alasdair Macleod discuss the near all-time record demand for gold and what this means for the price of gold in 2024 CLICK HERE OR ON THE IMAGE BELOW.

© 2024 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.