Today one of the greats in the business said the stage is set for a big move in gold and gold miners.

King World News has now released a powerful audio interview with Nomi Prins, who gives keynote speeches to the World Bank, IMF and Federal Reserve. For now…

The Stage Is Set

October 4 (King World News) – John Hathaway, Portfolio Manager at Sprott Asset: We believe the stage is set for a powerful advance in gold mining equities. While the 27.71% year-to-date advance in the bullion price could (but won’t necessarily) take a breather for the rest of 2024, significant catch-up potential for deeply undervalued gold miners has been barely exploited.

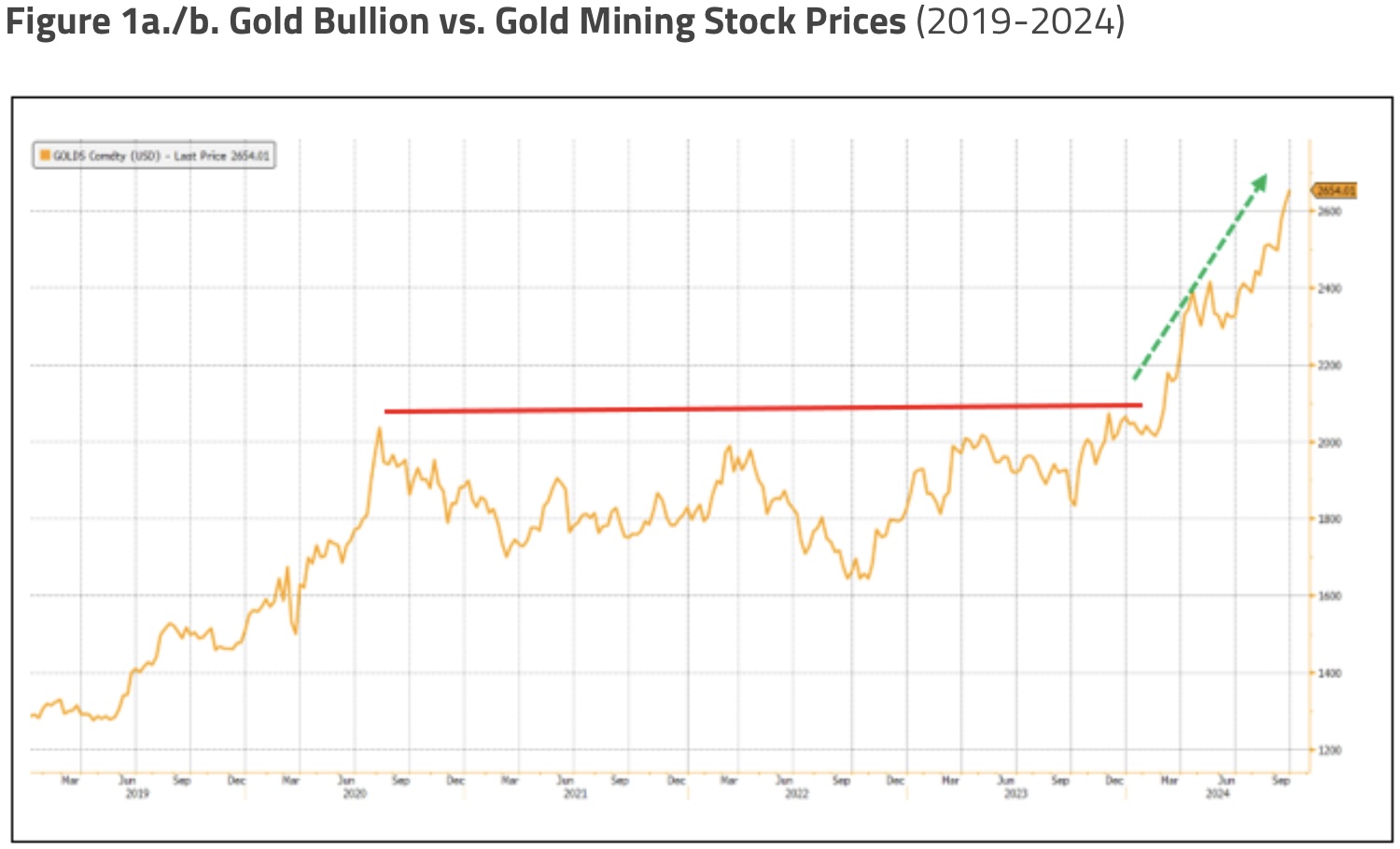

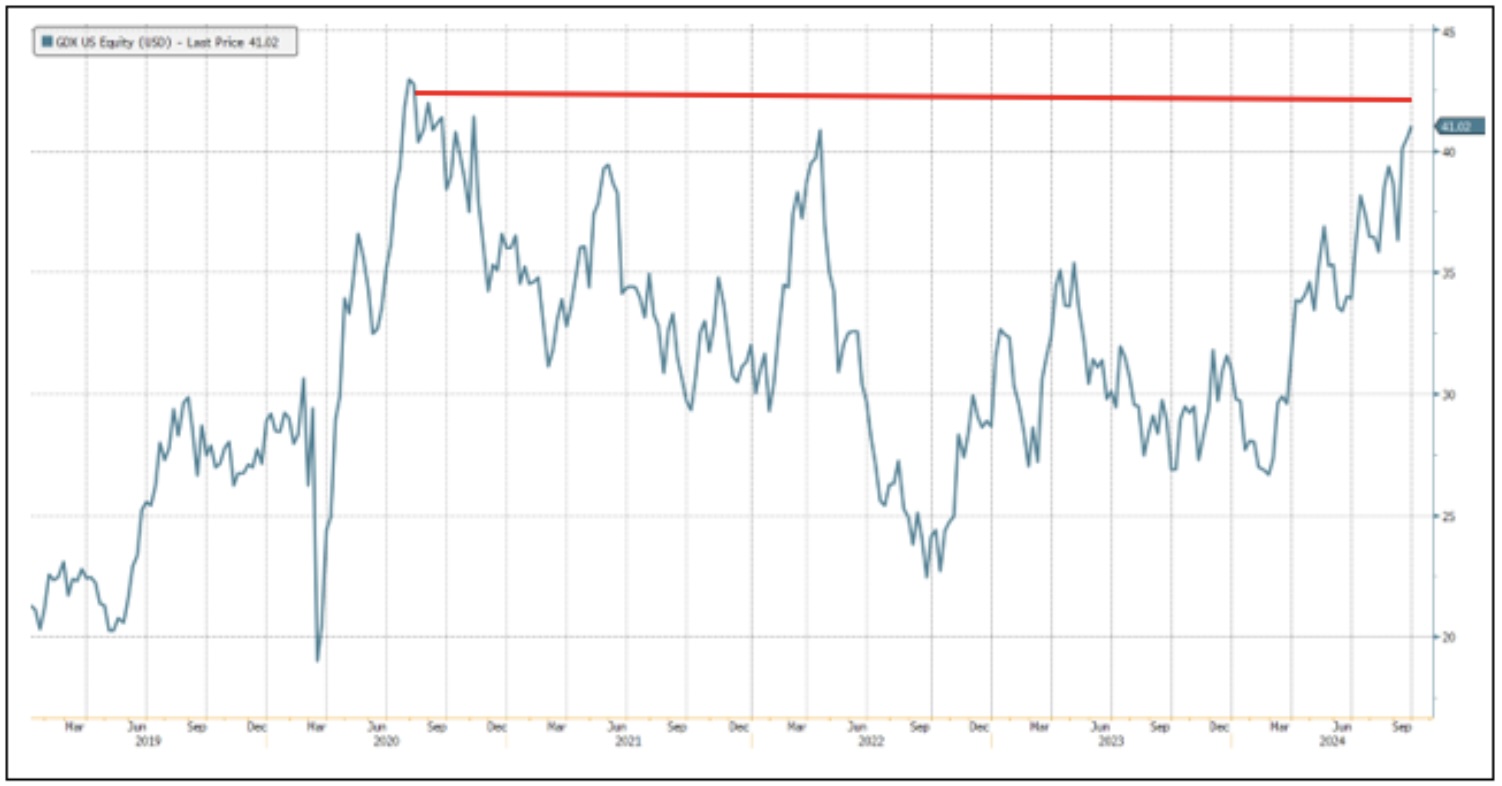

With gold trading at all-time highs, precious metals mining shares are just beginning to stir. GDX (VanEck Vectors Gold Miners ETF and a proxy for gold mining shares) has increased 28.41% year-to-date, only slightly more than the metal’s year-to-date gain of 27.71% (as of 9/30/2024). Looking at the five-year total return comparison (10/1/2019 to 9/30/2024), mining stocks gained 58.71%, distantly lagging gold’s 78.92% rise.

We have addressed the disconnect between gold bullion and gold equities in previous commentaries. Gold stocks, in our opinion, are coiling for a sharp advance during the remainder of 2024. At the time of writing, GDX is breaking out above a five-year trading range that looks very similar, with a six-month lag, to gold’s breakout earlier this year.

Favorable Fundamentals for Gold Miners

The investment fundamentals for miners have rarely been so favorable against a backdrop of such disinterest. The Q3 2024 average gold price (the most important single variable for miners’ earnings and cash flow) will exceed Q2 by 5.2% sequentially, and 2023 by 18.8% year-over-year. For many companies, production is weighted toward the second half; we believe we may see blockbuster Q3 earnings reports later in October and early November.

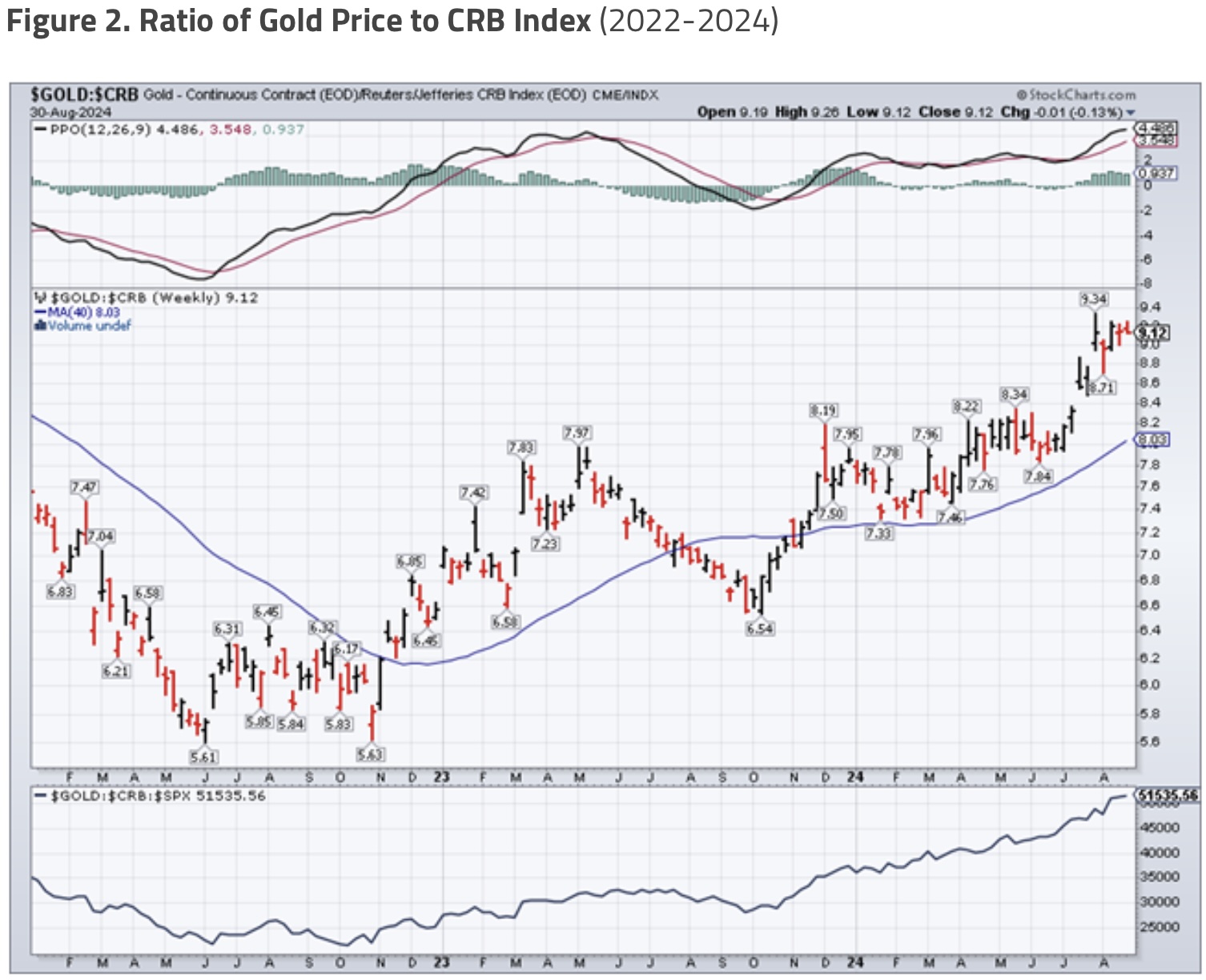

Looking ahead to 2025, we expect production costs to remain stable or even decline in the event of a recession. Profit margins could expand even if the U.S. dollar gold price marks time (which we don’t expect). Figure 2 depicts the relationship between gold and commodity prices (CRB Index). A rising trend line tends to be exceptionally bullish for the earnings of gold miners.

Gold Is Still Underpriced

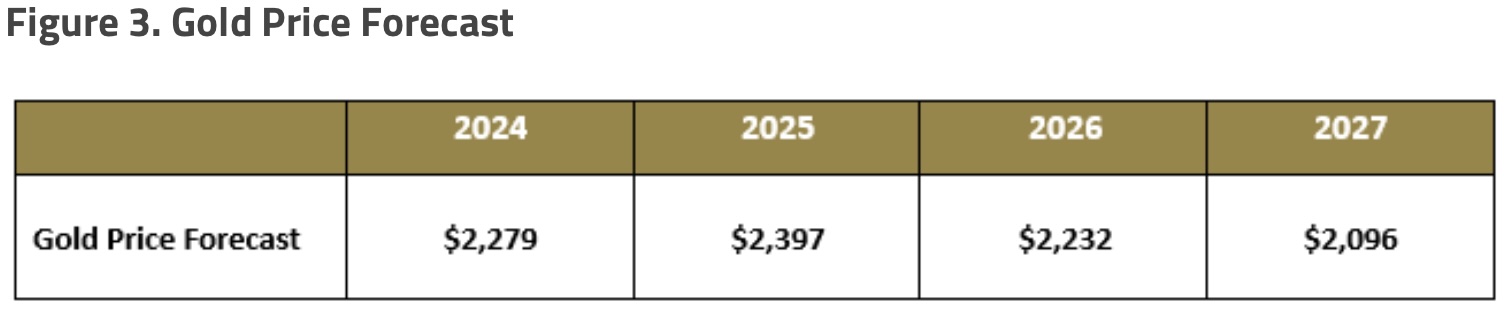

A key factor in the underperformance of mining shares is general disbelief that current gold bullion prices are sustainable or capable of further increase. In our view, the breakout in the gold price is not a fluke. The many contributing factors include (but are not limited to) de-dollarization, central bank buying, seemingly intractable U.S. fiscal issues, a possible recession, further monetary malpractice by the Federal Reserve (and other central banks) and the worrisome geopolitical landscape. Still, gold skeptics far outnumber believers. Proof can be seen in the forecasts for future gold prices from a broad array of financial firms (compiled by Beacon Securities; individual estimates by firm in Appendix A).

Who would invest in a gold mining stock with such a negative price outlook? While there are a few outliers, the consensus does not regard current prices as sustainable. We attribute collective bearishness to inattentiveness, lack of understanding, intellectual laziness, disinterest, and incompatibility with the groupthink underpinning mainstream financial market positioning.

For the sake of brevity, we will not elaborate here on the multiple forces (some admittedly speculative) that could power the further gains in monetary metals that we expect. Extensive commentary on our rationale can be found in our previous commentaries, as well as from many other observers.

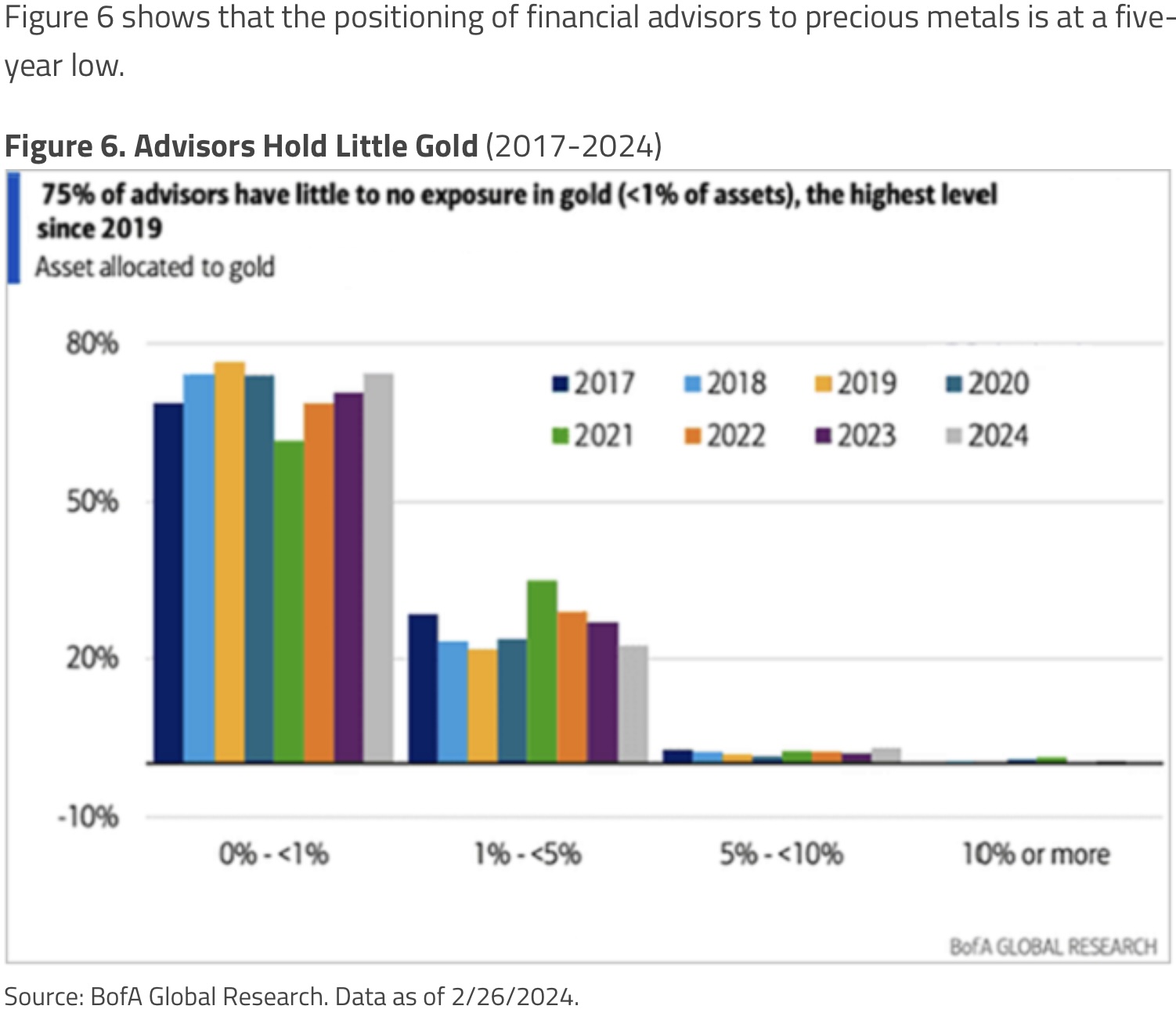

Western Investors Continue to Ignore Gold

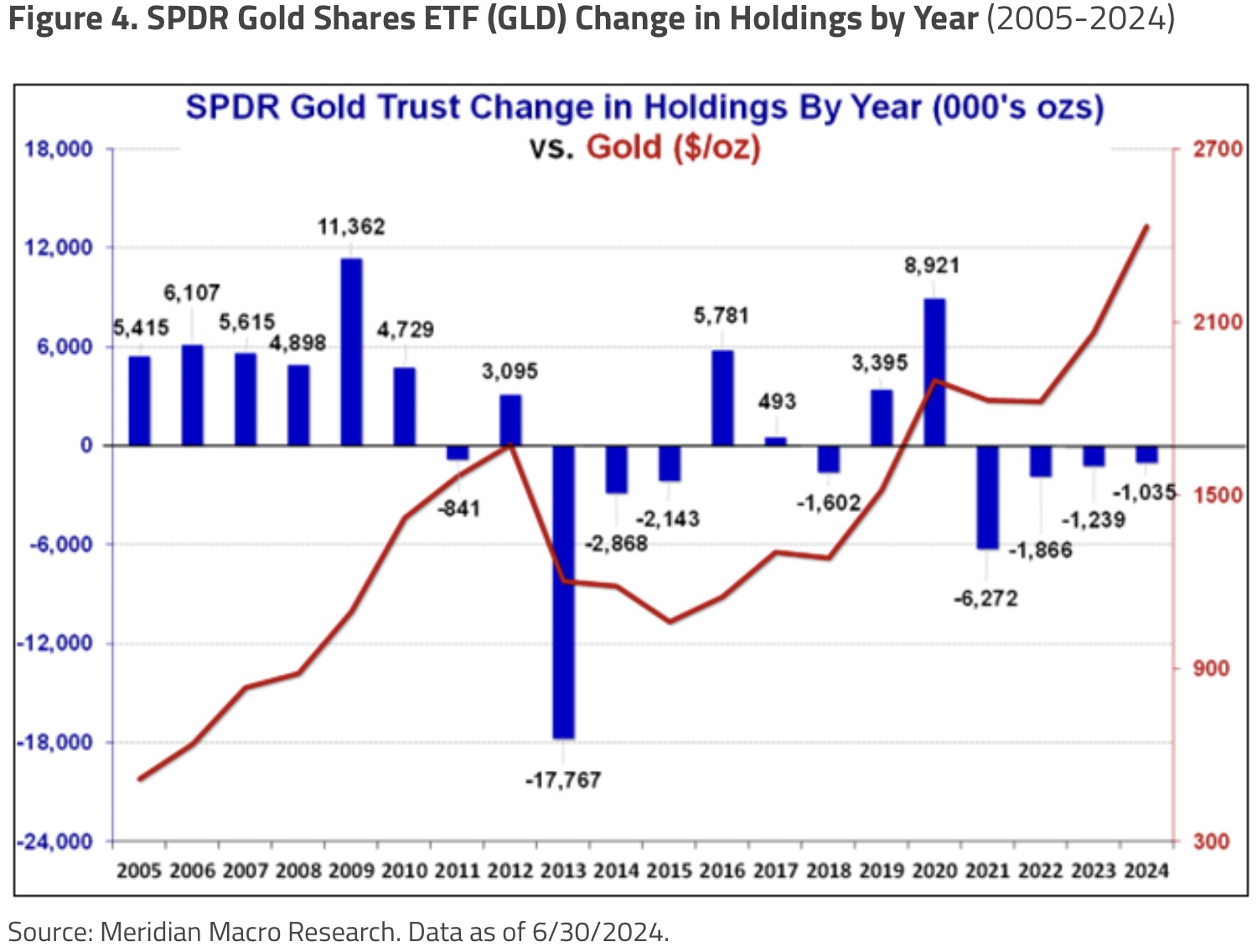

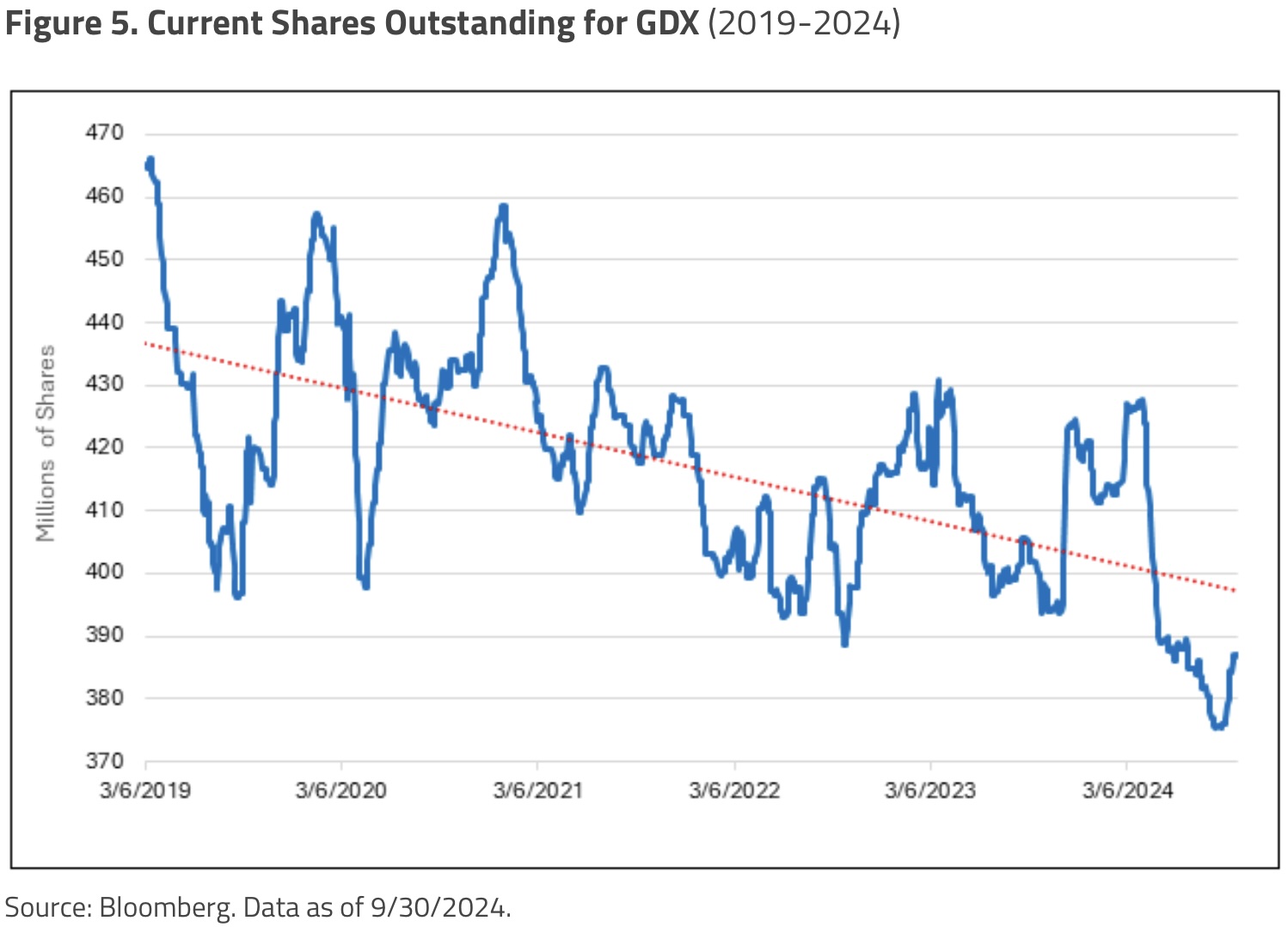

For now, it is enough to note that gold’s 78.92% five-year advance has occurred with almost no participation from U.S. and European investors. Negative investment flows have persisted in both ETFs backed by physical gold and mining stocks, as shown in Figures 4 and 5.

When Western capital market investors decide to reallocate a small portion of their capital to gold, and there are multiple reasons why they might, the metal’s price will likely move higher. The impact on mining company shares, which collectively have a market capitalization approximately equal to Home Depot or Costco’s, would, in our opinion, substantially exceed the percentage increase in the metal’s price.

It is worth noting that following the launch of GLD (SPDR Gold Shares ETF) in 2004, inflows of approximately 38 million ounces were sufficient to help fuel a 300% rise in the gold price from slightly less than $600 to $1,900 in August 2011, a seven-year span. Since 2010, the quantity of money (M2) has increased 248% while the quantity of gold has increased (through mine output) only 22.2%. The quantity of U.S. dollars that could be exchanged for gold has increased 10x relative to the quantity of physical gold over the past 15 years.

Measured against the ratio of U.S. dollars to gold creation, the five-year 70% increase in the gold U.S. dollar price seems both sustainable and probably inadequate. Liquidity created by the Fed’s decade-long policy of ultra-low interest rates and QE (quantitative easing) initially found its way into overvalued equities and assorted other financial assets. A small leakage from those positions would represent enormous buying power relative to available metal…

ALERT:

To learn about one of the greatest gold & silver royalty companies in the world CLICK HERE OR ON THE IMAGE BELOW.

Early-Stage Bull Market for Gold

The current bull market for gold is embryonic, in our opinion. The classic hallmarks of an early-stage bull market include widespread skepticism and general underpositioning. The inevitable transition of investor psychology from pessimism to exuberance takes several years. Long-term investors in mining stocks are beginning to experience a small amount of daylight with the year-to-date rally.

The temptation to cash in gains that are paltry relative to years of unproductive returns is difficult to resist. We advise further patience. In our view, valuations remain exceptionally attractive assuming only the continuation of spot pricing for precious metals. Inflows into the tiny precious metals mining universe have barely started. The upside potential that likely lies ahead may be well worth any additional wait.

© 2024 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.