Below is a truly fascinating email from a retired pawnbroker.

From the Bench of the Retired Pawnbroker

October 22 (King World News) – Email from retired pawnbroker Gurjit L: The Pawnbroker’s Lens: Why the Money Supply and Gold Still Matter

You see, for thirty years, I dealt with the most basic form of finance: cash for collateral. I saw what a Pound was actually worth on the street. Forget all the fancy finance terms; when the money supply—M2—goes up or down, it changes the value of what folks bring through my door, whether it’s a gold watch or a title loan application. And right now, there are three huge, wonky forces at play: the wild swings in M2 growth, the absolute control of the Federal Reserve in enabling that growth, and the looming shadow of Basel III.

Let’s break down what’s happening to the very currency in your pocket.

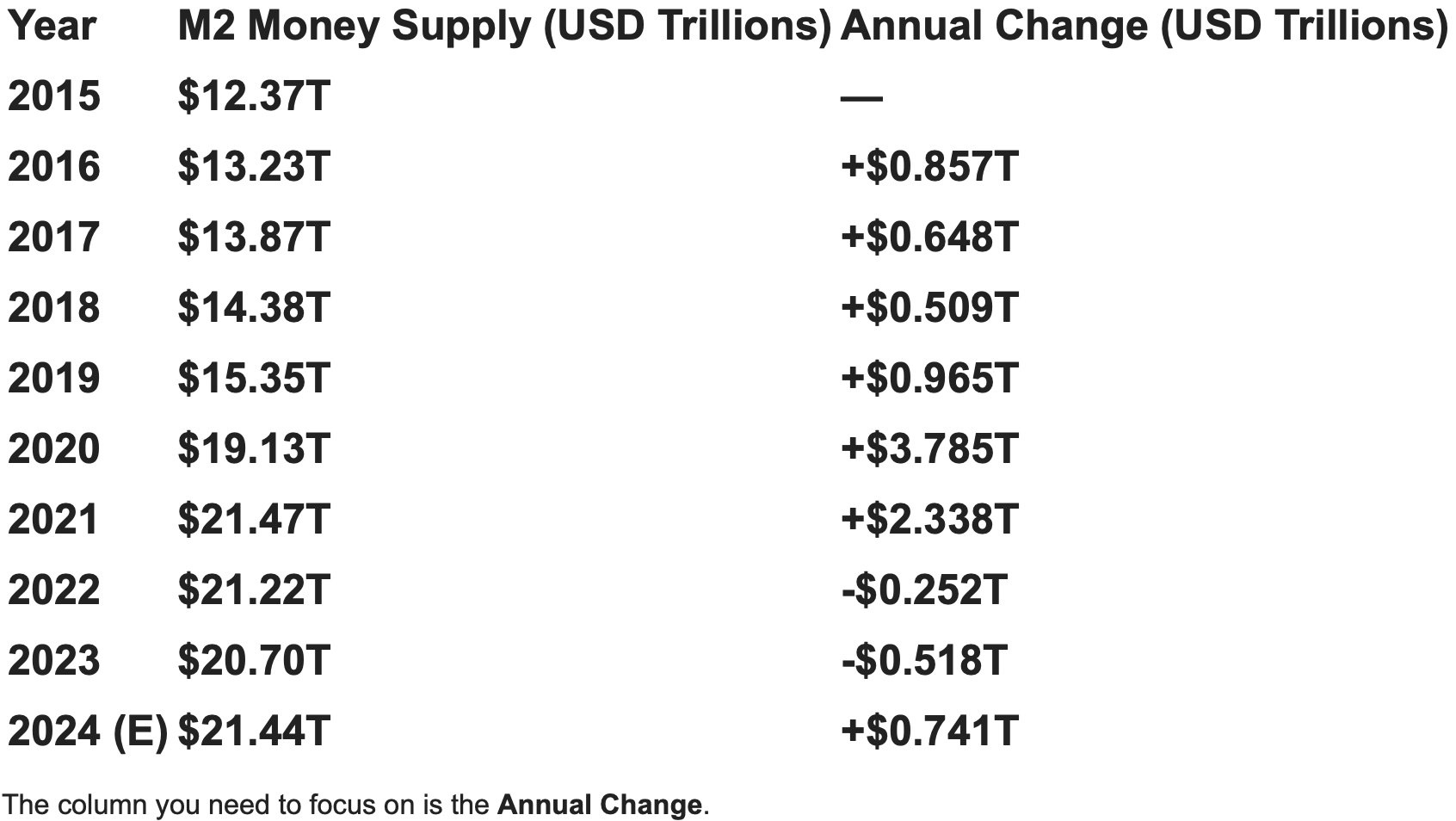

The Mountain of Money: U.S. M2 Supply

M2 is the economist’s way of saying, “all the easily available money.” It’s the currency in your hand, the money in your checking and savings accounts, and your small certificates of deposit. It’s the total pile of readily accessible cash in the country.

Look at the numbers. Nothing short of a wartime boom explains the jump between 2019 and 2021. The Federal Reserve moved money into the system at a speed never before seen, trying to keep the economy from locking up.

- The years 2020 and 2021 saw a colossal influx of new money (over $6 Trillion combined). This flood of dollars chases the same amount of goods and services, leading straight to inflation. That’s why everything costs more—there are simply too many dollars in the system.

- The years 2022 and 2023 showed a rare, small contraction. The Fed began pulling some money out, a process called Quantitative Tightening. This is a deflationary pressure, showing the market is trying to digest the massive printing binge.

The Architect of Money: The Role of the Federal Reserve (The Fed)

The Fed’s primary job is to control the money supply and influence interest rates to achieve maximum employment and stable prices. They do this mainly through commercial banks, where money creation actually happens.

How M2 Explodes: Banks Create Money

This is the key concept that shocks people: M2 doesn’t just grow when the government prints paper cash; it grows primarily when banks make loans.

- The Loan Process is Money Creation: When a bank issues a $100,000 car loan, they don’t take it from a vault. They simply credit the borrower’s checking account (which is part of M2) with the amount. In that moment, the money supply has instantly increased by $100,000, created out of thin air, backed by the borrower’s promise to repay.

- The Refinancing Trick: Low rates encourage a refinancing boom. When a homeowner cashes out $50,000 in equity, that money goes straight into their checking account. This, too, is an increase in the M2 money supply.

In short, the Fed enables lending, and lending creates the M2 money supply.

The Limit: Bank Capital Requirements

Banks can’t print money infinitely. Their main constraint isn’t how much cash they have in the vault, but their own capital. They only have to have a certain level of banks’ own capital (equity, retained earnings) to issue new loans. This is set by regulators like the FDIC and Federal Reserve, and is their primary tool for managing risk and controlling the maximum amount a bank can lend. The less capital a bank has, the fewer new loans it can create.

The Gold Standard: A Pawnbroker’s True North

When the dollar gets shaky due to surging M2, people turn to what’s tangible. For me, that’s always been gold.

Gold is the Anti-M2: The M2 money supply can be expanded at the push of a button. Gold is finite. When the M2 supply surges, it means your dollar buys less, and the price of gold, the eternal hedge against currency devaluation, tends to rise because the currency used to buy it is worth less. Gold becomes the logical safe haven for people scared that their cash savings are melting away.

The Shadow of Basel III: Why Banks Care About Gold

Basel III is a set of global banking standards designed to improve capital and liquidity rules following the 2008 financial crisis. For the gold market, these rules fundamentally change the economics of holding gold, especially the distinction between physical and “paper” gold.

The 0% Capital Requirement Rule

Under the Basel III framework, physical gold bullion held by a bank (or held on an allocated basis, where the client owns specific bars) is recognized as a Tier 1 Capital Asset and is assigned a 0% risk-weighting.

- What this means: Banks are not required to hold any loss-absorbing capital against their allocated physical gold holdings, treating it effectively the same as cash. This acknowledges gold’s lack of credit risk and its function as a high-quality reserve asset.

The Cost of ‘Paper Gold’: Net Stable Funding Ratio (NSFR)

The more immediate impact, particularly in the London Bullion Market (which involves a great deal of unallocated gold), comes from the Net Stable Funding Ratio (NSFR) rules, which for major banks are being implemented globally, including the US potentially beginning a phase-in period starting July 1, 2025 (though implementation timelines can vary by jurisdiction).

- Unallocated Gold Exposure: Unlike allocated gold, exposures due to unallocated gold accounts (which are essentially bank liabilities or contracts for gold) and other gold derivatives are treated like any other physically traded commodity.

- The 85% Rule: These exposures are generally subject to an 85% Required Stable Funding (RSF) factor. This means banks must fund 85% of their unallocated gold liabilities with long-term, stable funding. This dramatically increases the cost and capital needed for banks to run high-leverage “paper gold” operations.

Basel III heavily favors holding physical gold on the balance sheet, as it is cheap and safe to hold (0% capital requirement), while making it far more expensive to run highly-leveraged unallocated (paper) gold positions (85% funding requirement). This regulatory shift creates a structural, long-term incentive for major institutions to increase their demand for the real, physical metal.

The Pawnbroker Takeaway: This institutional demand is a long-term, powerful upward force on the price of gold, reinforcing its status as the ultimate safe haven in an era of volatile money supply figures.

Final Thoughts from the Bench

We’ve seen massive, unprecedented moves in the money supply, and institutional demand for gold is now baked in thanks to regulation. However, nothing goes straight up forever.

We are due some big pullbacks in the gold price. These are necessary to grab liquidity from the markets and not to destabilize the markets too quickly. I will give you my charts and thoughts on entry points in my next article.

Enjoy the ride, and remember the key takeaway from the old pawnbroker:

Be patient. Do nothing but stack on dips. this is not the final end game yet.

Gurjit L

KWN Gold Special!

In this KWN Gold Special interview listen to the man who correctly predicted that 2024 and 2025 would each be a Golden Year For Gold gives listeners an update on what to expect with gold, silver and miners CLICK HERE OR ON THE IMAGE BELOW.

Friday’s Pullback In Gold & Silver

To listen to Alasdair Macleod discuss Friday’s pullback in gold, silver and the mining stocks as well as what to expect next CLICK HERE OR ON THE IMAGE BELOW.

© 2025 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.