As the stock market in the US plunges look at what has people worried.

Stock Market Decline

March 12 (King World News) – Peter Boockvar: It’s easy to blame the tariffs and scattershot approach being employed for the decline in the stock market but it’s broader than that. I argued last month (February 18th to be exact) that the AI tech trade was over in terms of their stock market dominance and it’s become clear of that, with the DeepSeek news in January being a key catalyst for that, along with the unclear revenue drivers all this spend will generate. Also, we now have multiple compression also being a notable part of the stock performance as earnings growth slows. You lose the special 7 stocks, which at its peak made up about 35% of the S&P 500, you are without a net in the broader market unless the baton is immediately passed to someone else.

I also said then, “In a way, the big 7 have become its own reserve currency where foreigners around the world have parked their money in and kept a bid under the US dollar.” Well, we’ve seen the US dollar tank along with the big 7 stocks. And many international stock markets have done great instead and where we remain bullish and long of. To this point that the selloff is not just worries about tariffs, the Mexican stock market is up for the year by 4.5% and the Canadian market is down only slightly, by 1.4%.

My point here is, and I’ll say again, a regime change is taking place in the markets and what used to work is not going to work from here anywhere to the same degree. The stock market has a history of handing the baton over to other things and now seems to be one of those times.

Domestic Travel Is Tumbling

I also want to point out that we are also possibly losing the massive fiscal influx into the US economy that I’ve talked about here and Treasury Secretary Bessent referred to last week as needed ‘detox.’ The nearly 7% budget deficit as a % of GDP was also a big boost to corporate earnings and profit margins. I need to add now too, the other big leg holding up the US economy has been upper income spending, as we know, helped by a record net worth for those that own stocks and their homes. Thus, we lose the stock market right now, you can be sure upper income spending will falter. You want to debate the odds of a recession? you need to have an opinion on the S&P 500.

Southwest Airlines is repeating pretty much what Delta said last night in response to the now cloudy economic outlook. This morning they are lowering their Q1 revenue per available seat mile (RASM) growth rate to a “range of 2% to 4% on capacity down approximately 2%, both on a y/o/y basis. They blame part of this on “less government travel, and a greater impact from the California wildfires than originally estimated.” But also this, “The remainder of the decrease is primarily attributable to softness in bookings and demand trends as the macro environment has weakened.”

This is what Delta said last night in its 8k:

They lowered their y/o/y revenue guidance to growth of 3% to 4% from its initial guidance of 7% to 9%, along with trimming margin and eps guidance and said “The outlook has been impacted by the recent reduction in corporate confidence caused by increased macro uncertainty, driving softness in Domestic demand. Premium, international and loyalty revenue growth trends are consistent with expectations and reflect the resilience of Delta’s diversified revenue base.”

From American Airlines too:

“the revenue environment has been weaker than initially expected due to the impact of Flight 5342 and softness in the domestic leisure segment, primarily in March.”

Of note in yesterday’s NY Fed’s Consumer Expectations Survey where inflation expectations were little changed, they said this on the labor market:

“Mean unemployment expectations – or the mean probability that the US unemployment rate will be higher one year from now – jumped 5.4 percentage points to 39.4%, its highest reading since September 2023. The increase was broad based across age, education, and income groups.” Also, the quit rate fell to the lowest since July 2023.

Credit Contraction

On the credit side for consumers, “Perceptions of credit access compared to a year ago showed a larger share of households reporting it is harder to get credit, and a smaller share reporting it is easier. Expectations for future credit availability deteriorated considerably in February.”

And, “The average perceived probability of missing a minimum debt payment over the next three months increased by 1.3 percentage points to 14.6%, the highest level since April 2020.”

To the concerns above, “The share of households expecting a worse financial situation in one year from now rose to 27.4%, the highest level since November 2023.”

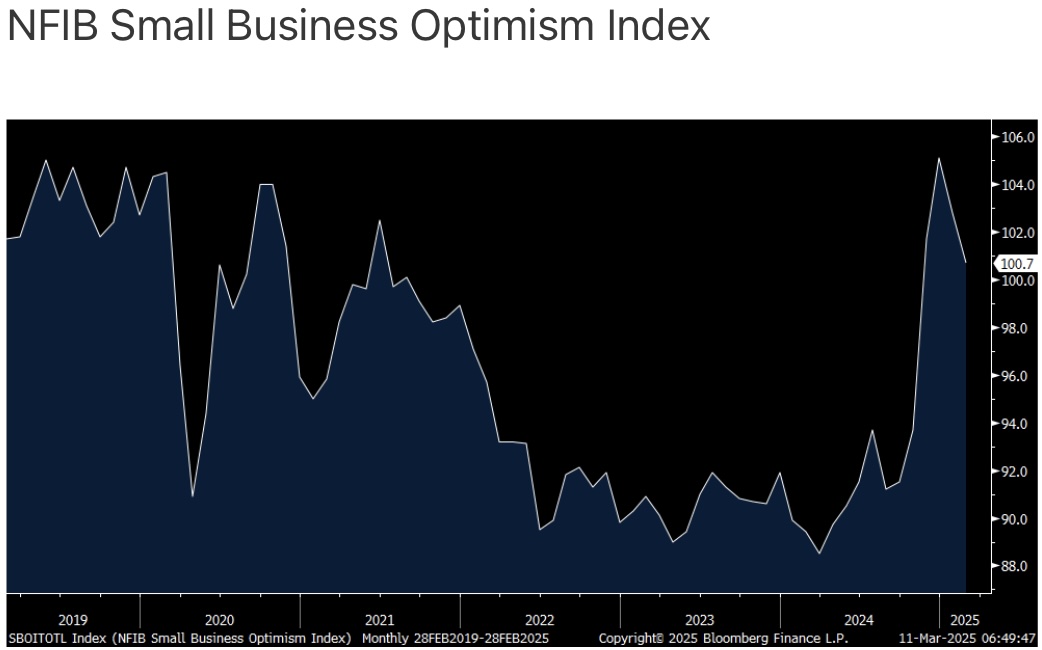

Now with respect to small business confidence, the NFIB optimism index for February fell 2.1 pts m/o/m to 100.7 and down for a 2nd month. It’s though still well above the October, pre-election, level of 93.7.

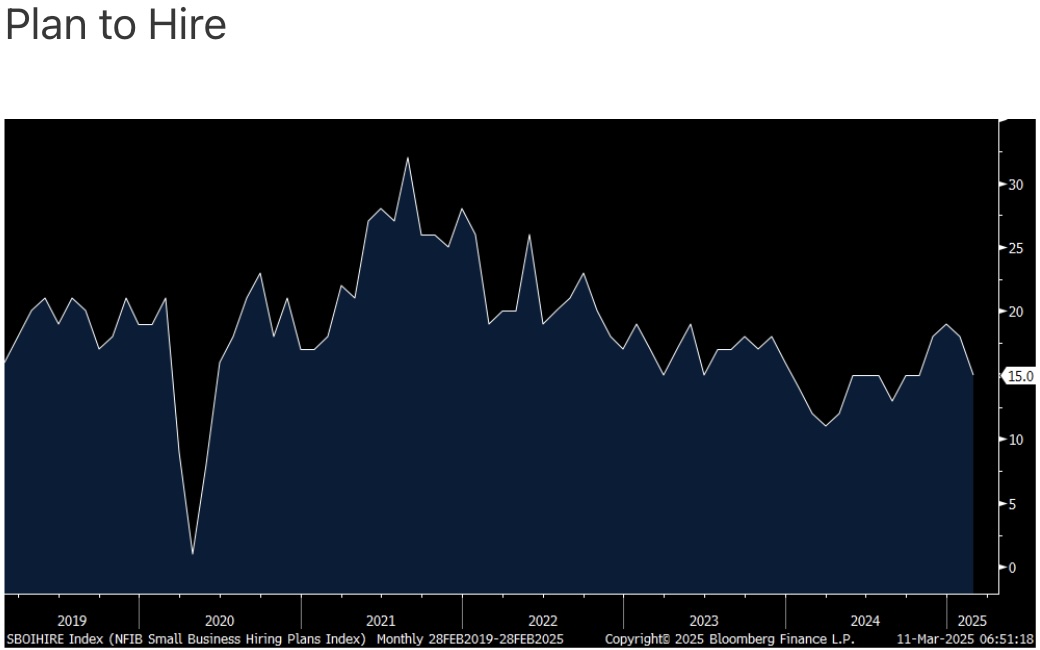

The key internals to highlight, Plan to Hire fell 3 pts to 15%, matching the lowest level since August 2024.

Current compensation was unchanged but future comp plans eased by 2 pts.

Of particular note, and most likely in response to the tariffs, Higher Selling Prices jumped by 10 pts to 32%, the highest since May 2023. The NFIB said “this is the largest monthly increase since April 2021, and the third highest jump in the survey’s history.” Capital spending plans fell 1 pt after dropping 7 pts in January.

Those that Expect a Better Economy fell 10 pts but still is well above zero at 37% vs the -5% it was at in October. Those that Expect Higher Sales and that it’s a Good Time to Expand also fell m/o/m. The average rate paid on a loan dropped to 8.8% from 9.4%.

The NFIB said “Small business owners have experienced uncertainty whiplash over the last four months with the Uncertainty Index falling from October’s 110 reading to 86 in December and then back up to 104.”

As for the top business issue, ‘labor quality’ has now surpassed inflation by 3 pts, though the NFIB still said “Inflation remains a major problem.”

The bottom line from the NFIB, “Uncertainty is high and rising on Main Street, and for many reasons.” I’m sure tariffs and the threats of them are the main reason.

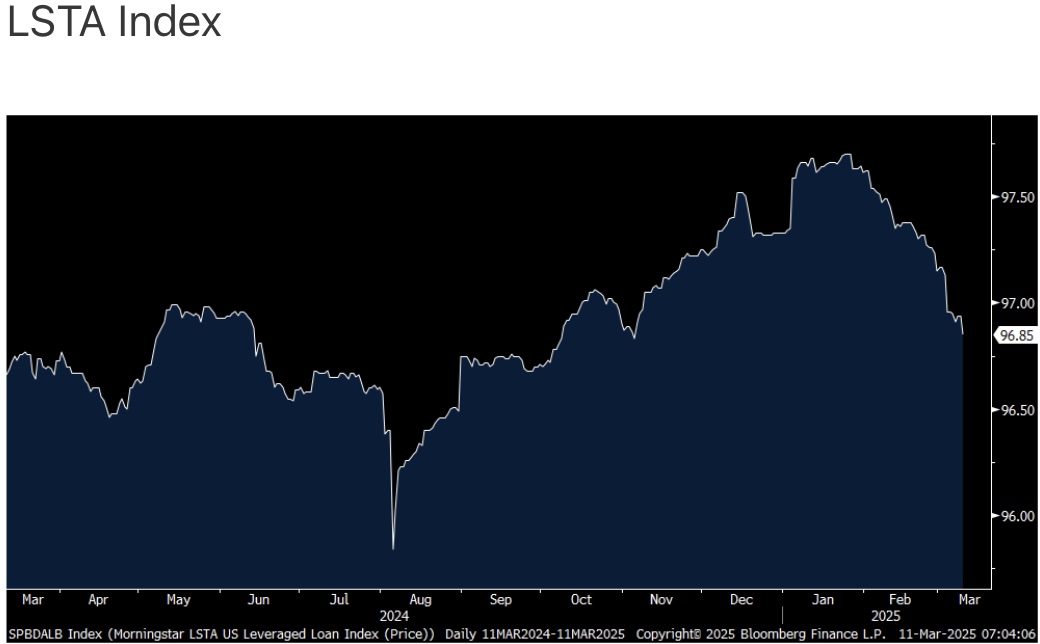

…here is a chart of the LSTA leveraged loan index which includes floating rate debt.

So, on expectations of more Fed rate cuts, these loans become less attractive at the same time the credits, lower end of totem pole, lose luster with worries over economic growth.

Gold Has Been The Light In This Volatility Storm

To listen to Nomi Prins discuss the wild trading in global markets, gold, silver, uranium, mining stocks, what to expect next and more CLICK HERE OR ON THE IMAGE BELOW.

WILD TRADING!

To listen to Alasdair Macleod discuss this week’s wild trading action and what to expect next CLICK HERE OR ON THE IMAGE BELOW.

© 2025 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.