Gold and silver Open Interest has collapsed to the lowest level in 13 years!

Open Interest Collapses

May 29 (King World News) – Alasdair Macleod: As China buys up the bullion, the relevance of paper markets on Comex (and London) is shrinking. Liquidity and relevance of paper gold and silver relative to bullion are diminishing.

This market report analyses why open interest on Comex has declined to multi-year lows and the consequences. Clearly, liquidity has been drained from western paper markets by the continual drift of bullion into firm Asian hands. We present evidence of the strains on market makers on Comex who have limited capital resources and we debate the consequences.

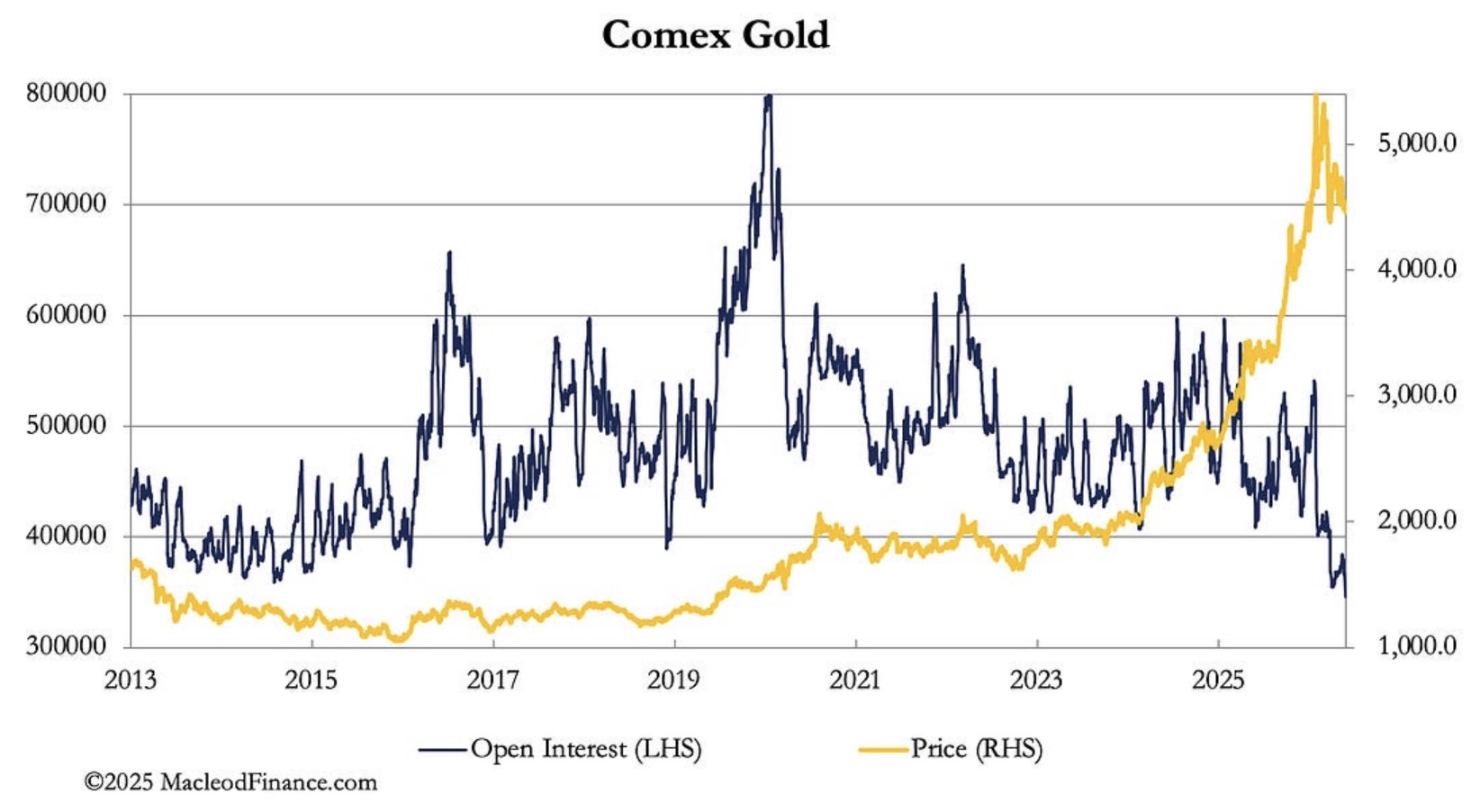

Open interest is now at multi-year lows

This week saw open interest in the Comex gold contract drop to under 350,000 contracts. This is the lowest it has been in at least thirteen years.

It is the clearest indication of a near total absence of speculative interest on Comex, and because Comex arbitrages with London, it will be true of that market as well. This is even more remarkable given the price rise since 2023 would normally lead to greater speculative interest, but it has collapsed instead, particularly after December 2024.

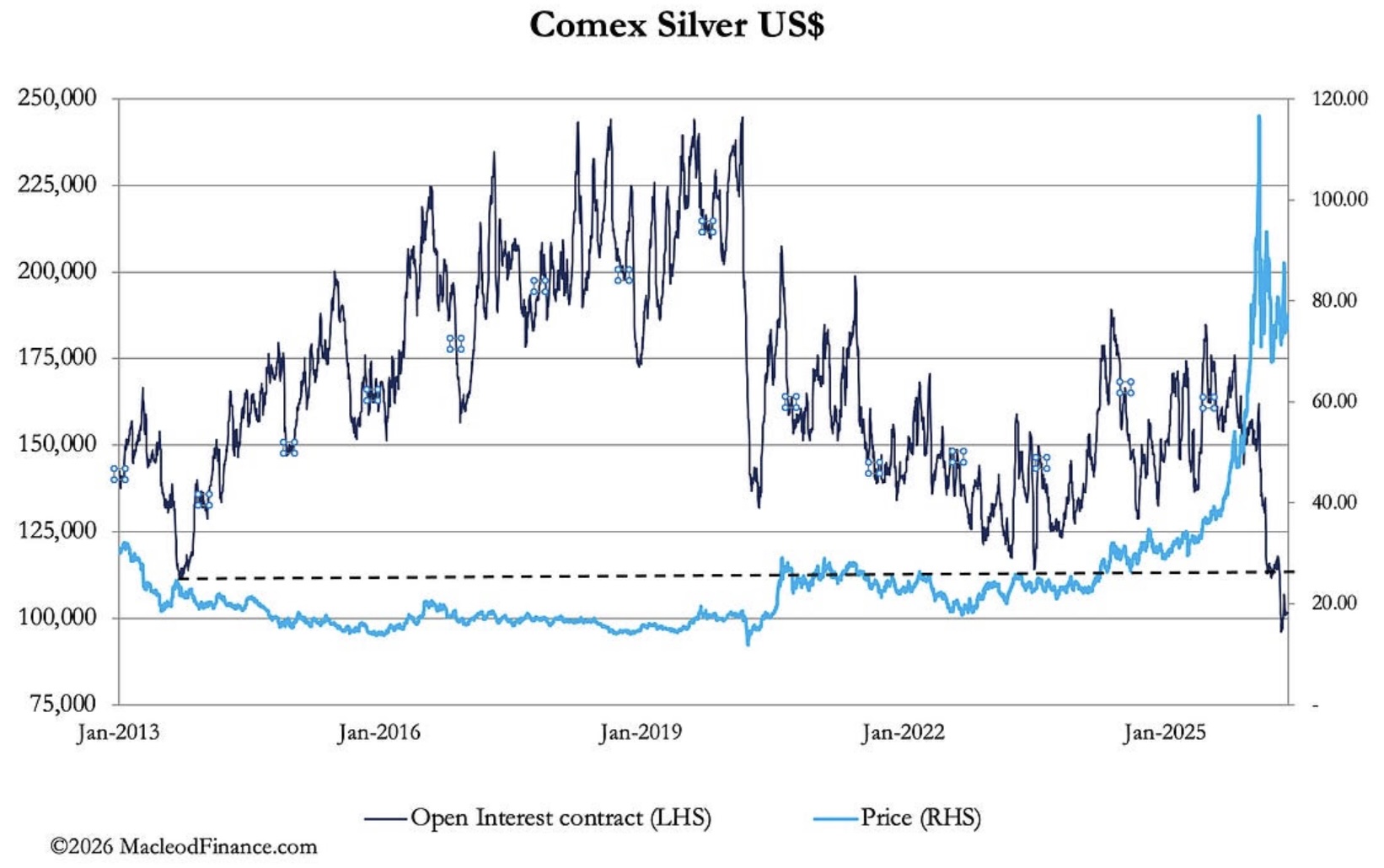

We see the same trend in Comex’s silver contract, which is next:

Open interest is also the lowest for thirteen years by far, and its collapse is firmly tied to a silver price which rose sharply from mid-October last. This links the collapse in speculative interest to the extreme liquidity problem in London when silver’s lease rate rose to a stunning 40% on 9th October.

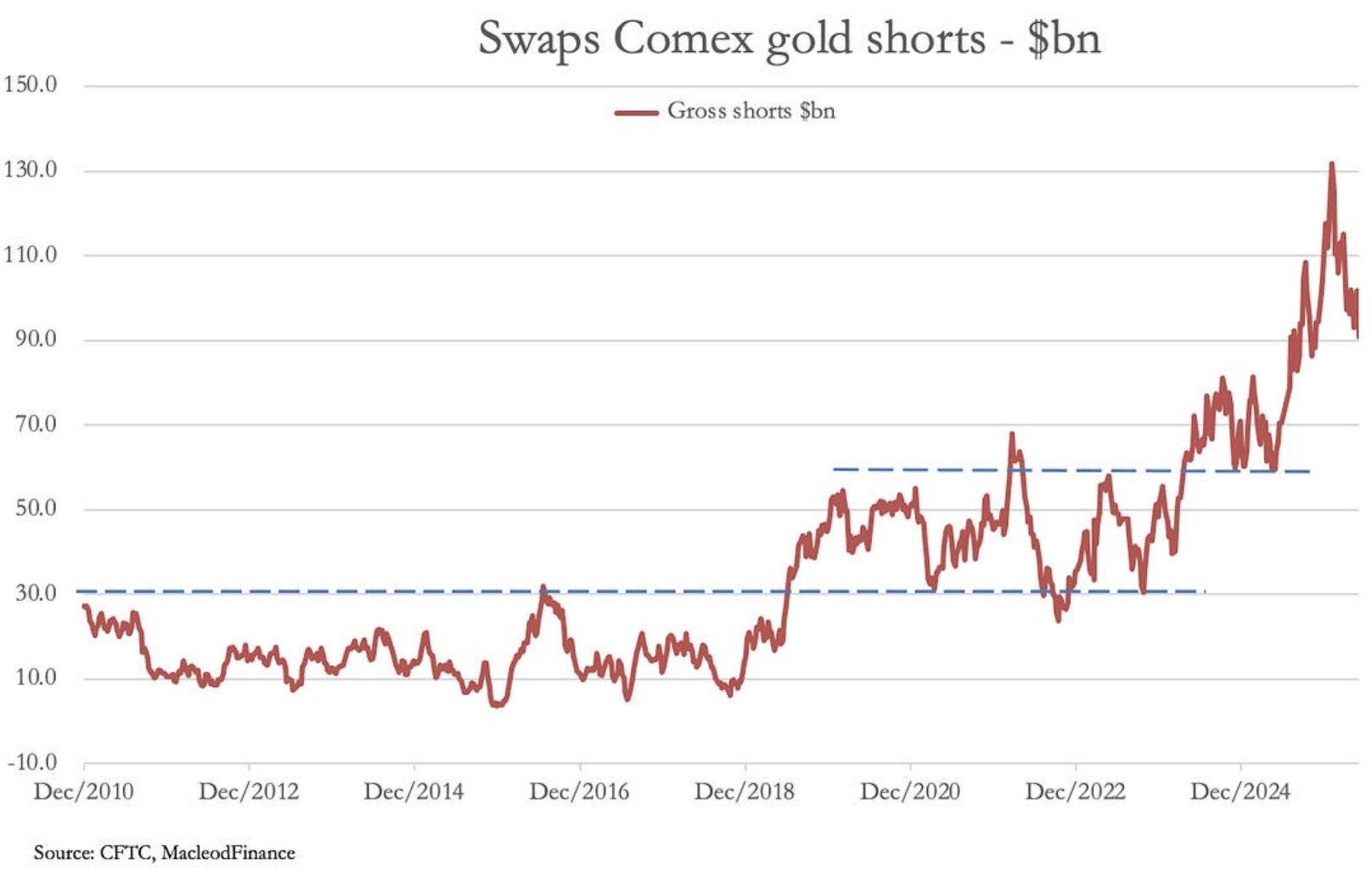

So, liquidity in futures and forwards is the problem. Higher prices must be stretching the position limits of market makers and bullion bank traders, collectively the swaps category on Comex, which traditionally takes the short side. This is evidenced in our next chart of the dollar-value of the swap category’s shorts:

For many years, this category contained its collective shorts to less than $30 billion shown by the lower pecked line. That then doubled to about $60 billion and today having peaked at double that again, the current price consolidation coupled with a drop in open interest still has it at an uncomfortable $90 billion. Average individual swap short exposure is $3.75 billion having been close to $5bn when gold peaked.

Besides the obvious strain on capital resources and the increase in systemic risk, we arrive at an important conclusion: London and New York lack the capacity to deal with higher bullion prices. In other words, as a means of diverting gold and silver demand into paper contracts and thereby containing prices, after decades of success it is now failing.

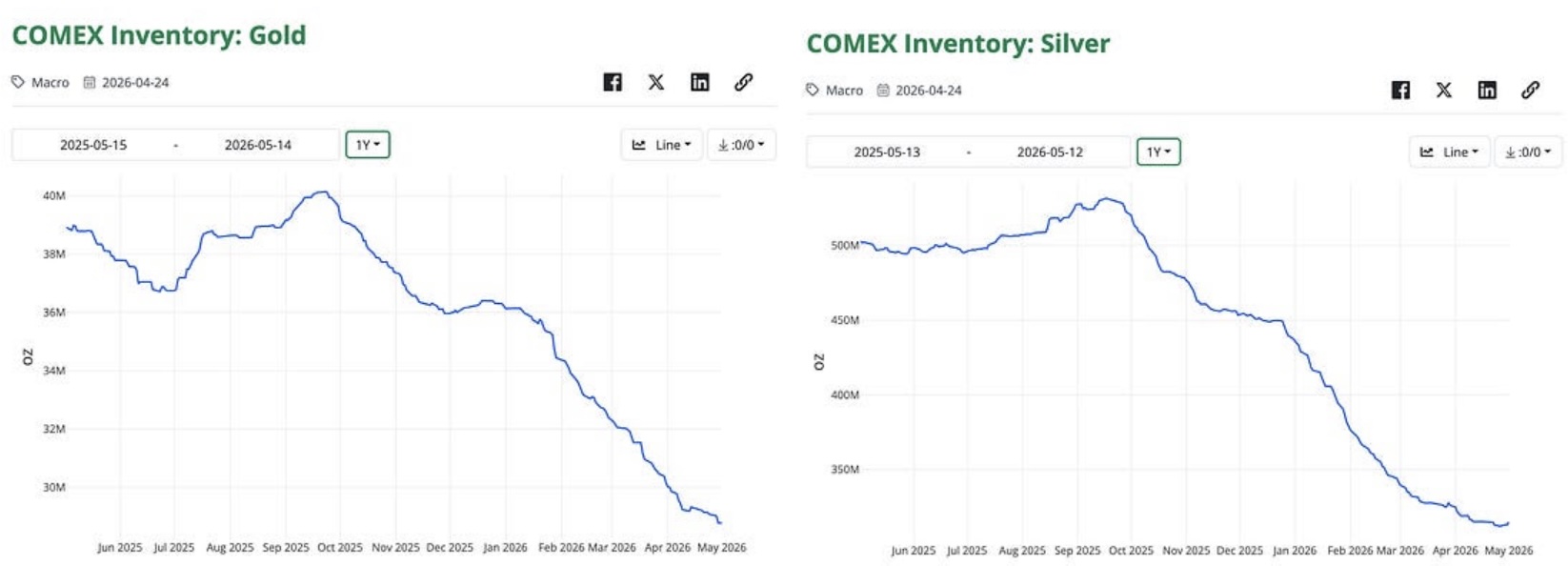

The reason is that demand for physical liquidity is now driving prices. This is the consequence of Asian selling of dollars for gold. It is reflected in Comex warehouse statistics for gold and silver which continue to be drained despite the fall in prices over the last four months. These are illustrated next:

As well as continuing demand for gold from central banks, China’s commercial banks are big buyers. They offer their customers gold accumulation accounts, which they have been forced to suspend or restrict due to lack of available bullion. They have used a falling price in the London and New York as an opportunity to replenish their stocks.

But only yesterday, it was announced that the facility was becoming available again. This was from a Chinese newspaper:

Meanwhile spot prices in London have failed to properly reflect demand for bullion, being essentially a “local” price — local that is to western capital markets. A similar situation is seen in oil, where Asian prices on the ground are significantly higher than US and European prices. Gold and silver are not the only markets bifurcating both regionally and between paper contracts and physical reality.

In London and Comex, gold and silver prices reflect a short-termism which denies actual consequences. Oil prices rise, and gold and silver get marked down. Bond yields rise, and gold and silver get marked down. In Asia the view is diametrically opposed. Oil prices rise and the dollar’s value is threatened. Bond yields rise because the dollar’s purchasing power is falling.

All reasons in Asia to sell the dollar for gold. A consequence is that when speculative interest returns to western capital markets, the lack of liquidity can be expected to see gold and silver prices squeezed significantly higher than their end-January peaks. That in itself will raise awkward questions over the future of the fiat dollar…to continue listening to Alasdair Macleod discuss the collapsing Open Interest and gold and silver being drained out of COMEX vaults CLICK HERE OR ON THE IMAGE BELOW.

China Paying Massive $10-$12 Premium To Get Physical Silver

To listen to James Turk discuss China paying massive premiums for physical silver as well as what surprises are happening in the gold and mining share markets CLICK HERE OR ON THE IMAGE BELOW.

ALSO RELEASED!

Gold, Miners And Commodities Poised To Radically Outperform CLICK HERE.

The Great Unwind, Gold, Silver And Mining Stocks CLICK HERE.

The Truth About Gold And The Coming Stock Market Crash CLICK HERE.

Everyone Needs To Read This And Be Prepared For What Lies Ahead CLICK HERE.

Look At Who Is Long Gold, Silver, Miners, Oil Fertilizer & Uranium Stocks CLICK HERE.

Huge Gold & Silver Catalysts, Plus Look At What Just Collapsed Below 2008-2009 Lows! CLICK HERE.

Celente Says This Is One Of The Greatest Dangers Facing The World Today CLICK HERE.

COLLAPSE WARNING: This Is The Scariest Chart Of 2026 CLICK HERE.

COMEX Gold & Silver Inventories Are Collapsing! CLICK HERE.

They’re Lying To You About Gold, It’s Not In A Bubble And Headed A Lot Higher CLICK HERE.

One Chart Says It All: Something Is About To Snap CLICK HERE.

Gold Miners Now Doing Largest Share Buybacks In History CLICK HERE.

Another Major Oil Price Spike Will Be Hugely Bullish For Gold & Silver CLICK HERE.

World Economy “On Borrowed Time” As Massive Oil Crisis Looms CLICK HERE.

Take A Look At What Is Now Closing In On A 30 Year High! CLICK HERE.

Expect Violent Moves In Gold, Silver, Bonds And Stocks CLICK HERE.

This Is What A Boom Looks Like! Plus A Look At Another Collapse CLICK HERE.

© 2026 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.