The gold surge is global: from UK pawnbrokers to over $4,200 prices.

But First, Thanks…

October 17 (King World News) – Email from King World News Reader Tom Sawicki: Dear KWN, earlier this year, when Nomi predicted $4K gold by years end, it seemed like a fairy tale.

Not only did that come true, but right now $4365.

It seems like something big is happening right underneath our feet.

Thanks for helping us be informed.

Loyal Reader,

Tom Sawicki

Second … Key Chart For Those Watching Gold Price

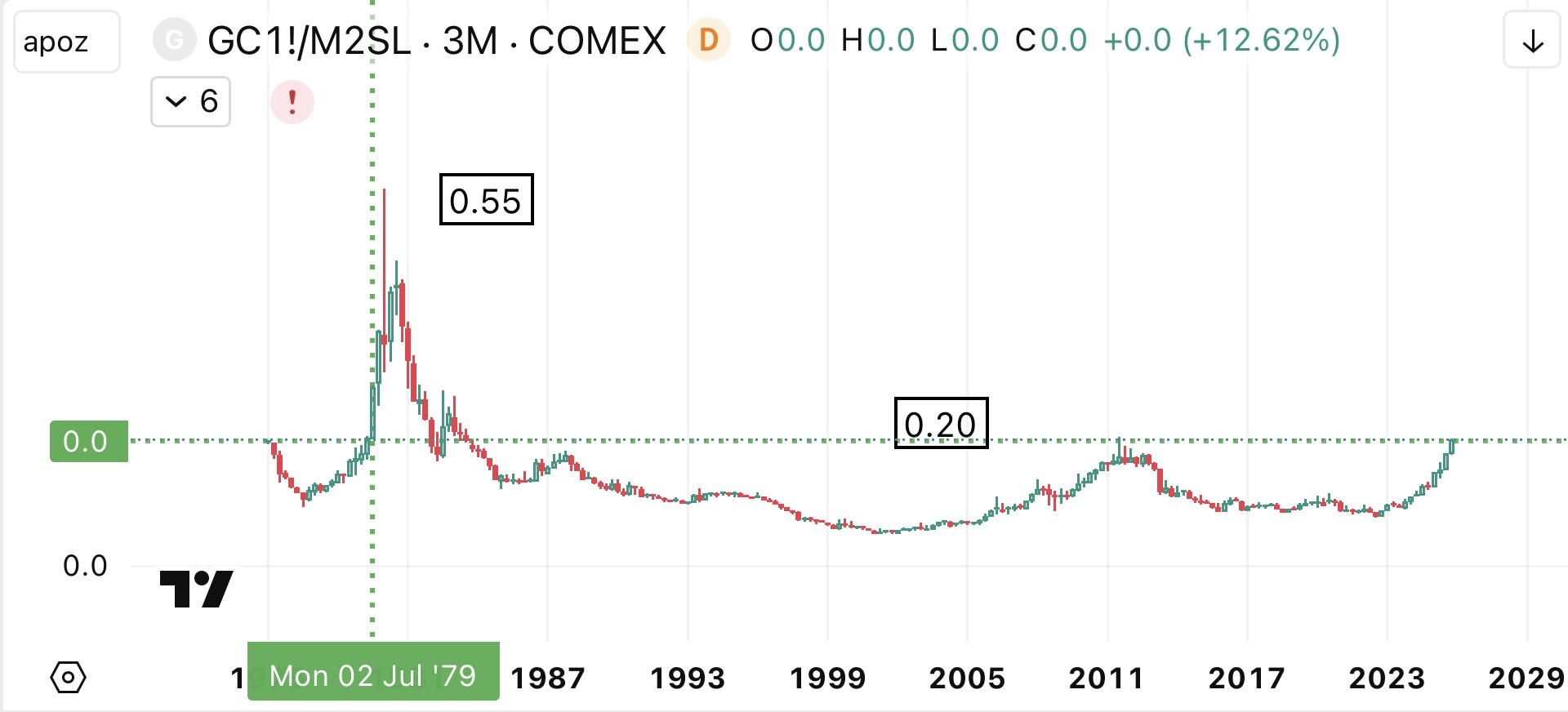

Email from King World News reader Kevin W: Yesterday’s email should have included the following chart of $Gold: M2 as it was referenced in April post. Currently $4400 and $22.1T respectively.

The ratio now about 0.20 (in billionths).

KING WORLD NEWS NOTE: Gold Still Cheap Compared To M2 Money Supply. After Gold Breaks Above 0.20 (GREEN DOTTED LINE) It Should Be Off To The Races On The Upside For Gold

Notice that the peak in that ratio in year 2011 was exactly 0.20.

Notice in Q3 ’79 that 0.20 threshold was breached as central planners lost control or sighed mea culpa. Two quarters later it reached 0.50

Do the math, 0.50 is 2.5x the price today and translates to over $10,000 gold with constant M2.

If US can make the world believe the Fed/UST has 8,100 MT of gold and $10,000 gold, those reserves would be valued at about 12% of US M2. That said $10,000 gold and global CB reserves of 41,000 MT against global M2 of $110T brings that value to only 12% of M2.

The Gold Surge is Global: From UK Pawnbrokers to Over $4,200 Prices

This piece was put together by King World News reader, and retired pawnbroker, Gurjit L: The gold price hits historic highs, driven by a perfect storm of institutional de-dollarisation and unprecedented retail demand across three continents. The spot price has recently reached a record level of over $4,200 per ounce, solidifying a spectacular rally.

Your observations on the street are perfectly timed, as global market data now confirms the dramatic shift you’ve witnessed. The price of gold surged above US$4,200 an ounce for the first time recently (and has climbed as high as $4,378 per ounce), extending its extraordinary rally to more than 60% this year (Trading Economics; Economic Times).

The speed of the upswing has been much faster than analysts had predicted, and current market sentiment—fueled by escalating geopolitical tensions and expectations of Federal Reserve rate cuts—suggests further gains are likely.

The UK Street View: Demand Shock

The anecdotal evidence from your colleagues in the UK refining and dealing sectors confirms an unprecedented appetite for the precious metal:

- Buying Team Expansion: Specialist gold buyers have drastically scaled up their operations, with some increasing their procurement teams from a mere two to ten—a 400% jump in capacity—just to handle the flow.

- Dealer-to-Dealer Buying: The most telling sign of shortage is that major dealers are now actively approaching smaller gold buyers and pawnbrokers to purchase stock directly from their customers.

This is not a supply issue; it is a demand shock. As you noted, it is not simply sellers increasing, but buyers—including sophisticated players—who are aggressively accumulating, suggesting a fundamental belief that Western markets are indeed “waking up” to gold’s new valuation.

Macro Drivers: Institutional Accumulation and ETF Frenzy

The meteoric rise is being fueled by two major, interconnected structural drivers, now further intensified by immediate geopolitical and monetary events:

1. Geopolitical Risk and De-Dollarisation

Emerging market economies, notably China and Russia, are strategically shifting their official reserve assets out of US Dollars and into gold to hedge against geopolitical risk and the threat of financial sanctions. The surge above $4,200 has been specifically attributed to:

- Rising US-China Trade Tensions: Renewed friction, including tariffs and trade restrictions, drives investors toward safe-haven assets.

- Weaponised Finance: The exclusion of Russia from the SWIFT system and proposals to seize its central bank reserves have fundamentally altered the global view of major reserve currencies, making gold a “safe” asset that cannot be sanctioned.

Central bank holdings of physical gold in emerging markets have risen a stunning 161% since 2006 to approximately 10,300 tonnes (International Monetary Fund data, as reported by The Conversation).

2. Investor Accessibility: The ETF and Rate Cut Effect

The soaring price has captured the hearts and wallets of retail and institutional investors alike, thanks to the accessibility provided by Gold Exchange-Traded Funds (ETFs), now paired with monetary expectations:

- Fed Rate Cut Expectations: Growing anticipation of a US Federal Reserve rate cut is boosting gold’s appeal. Gold performs well in low-interest-rate environments because it does not pay interest, making it more attractive relative to low-yielding bonds.

- ETF Inflows (FOMO): The World Gold Council reported record monthly inflows in September, with fund inflows totaling US$64 billion for the nine months leading up to that point. This “fear of missing out” (FOMO) effect is drawing new capital.

This combination of state-level geopolitical hedging and mass-market investment demand has led analysts at Goldman Sachs to increase their long-term price target for gold, now projecting it will reach US$4,900 an ounce by the end of 2026.

Market Volatility and The ‘Weak Hands’ Shakeout

Despite the clear upward trajectory, the market remains volatile. We expect some serious pullbacks in any market to grab any liquidity they can and shake weak hands to sell. This is normal market behavior designed to cleanse the market of retail investors who buy on momentum and panic-sell on dips.

However, the structural demand provides a powerful counter-force: only the brave or insiders would try and fight the central banks who are buying and not selling. This sustained, price-insensitive accumulation by official institutions fundamentally supports the floor of the market, suggesting that any sharp pullback is likely to be temporary and seen as a buying opportunity by large players.

Global Hotspots: Australia and India

The gold rally is reshaping physical markets and national economies worldwide:

Australia: The Export Bonanza

As the world’s third-largest producer of gold, Australia is experiencing a massive economic windfall.

- The Department of Industry, Science and Resources now expects the value of gold exports to overtake liquefied natural gas (LNG) exports next year.

- This would make gold the nation’s second-most important export behind iron ore.

India: The Smuggling Surge

In India, the convergence of record domestic prices and peak festival demand (Dhanteras and Diwali) is creating intense strain and heightening illegal activity.

- Domestic gold prices are now reaching over ₹130,000 per 10 grams (over $1,560, based on current rates), representing a 67% increase since the start of the year.

- The price differential is making smuggling highly lucrative, with margins for illicit operators potentially exceeding ₹1.15 million per kilogram, despite lower import duties. This suggests a tight supply situation combined with historic demand peaks.

From the high-volume UK street market to the record-setting central bank purchases and the surge in global smuggling, the message is clear: the bull market for gold has shifted into a new, aggressive phase, underpinned by both structural demand and geopolitical necessity.

Gurjit The retired Pawnbroker

© 2025 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.

")