There is no question that 2023 is going to be a big year for silver, commodities and gold.

2023: Big Year For Silver, Commodities And Gold

February 7 (King World News) – Ole Hansen, Head of Commodity Strategy at SaxoBank: Cautious and defensive trading – with a few exceptions – best describes the early 2023 price action across the commodity sector, a year that hopefully will provide less drama and volatility than last year, when the Bloomberg Commodity Total Return index surged higher to record a first quarter gain of 38 percent before spending the rest of the year drifting lower before closing with a 16 percent gain. This was a very respectable return considering the stronger dollar and market participants spending the second half increasingly worrying about a recession.

This focus helped drive financial deleveraging across the commodity sector and physical destocking to the point that some markets have ended up being ill prepared for a strong recovery in China and even less so should the most widely anticipated recession in history turn out to be a shallow one.

Tight market conditions across most commodities in 2022 saw forward curves swing into backwardation, a structure that rewards long positions through the positive carry from rolling (selling) an expiring contract at a higher price than where the next is bought. Backwardation helped drive the mentioned 16 percent return on a passive long investment in the Bloomberg Commodity Total Return index, almost 9 percent above the return signalled through changes in spot prices.

The key macroeconomic event that will drive developments in 2023 has, in our opinion, already occurred. The abrupt change in direction from the Chinese government away from its failed zero-Covid tolerance towards reopening and kick-starting its economy will have a major impact on commodity demand at a time where supply of several key commodities from energy to metals and agriculture remains tight. In addition, risk sentiment will likely also be supported by a continued and broad drop in the dollar as US inflation continues to ease, thereby supporting a further downshift in the Fed’s rate hike trajectory.

Furthermore, an increased likelihood of an incoming recession either not materialising or becoming weaker than anticipated may also trigger a response from financial and physical traders as positions and stock levels are being rebuilt in anticipation of stronger demand. In such a scenario, the structural underinvestment thesis, mostly impacting energy and mining, will likely attract fresh attention and support prices.

The strong gains seen at the start of the year – especially in gold and copper – have in our opinion showed the correct direction for 2023. However, while the direction is correct, we believe the timing could be slightly off, thereby raising the risk of correction before eventually moving higher. With activity in China and parts of Asia unlikely to pick up in earnest until after the Lunar New Year holiday, the prospect of a lull in activity could be the trigger for a pause in the current rally, before gathering fresh momentum and strength from the second quarter and onwards…

To find out which gold & copper explorer is trying to hit significant mineralization click here or on the image below

Adding these together we conclude the commodity sector remains on a journey towards higher prices, and while the speed of the ascent will slow we project several years ahead where supply of key commodities may struggle to meet demand. With that in mind, we forecast another positive year for commodities resulting in a +10 percent rise in the Bloomberg Total Return Index.

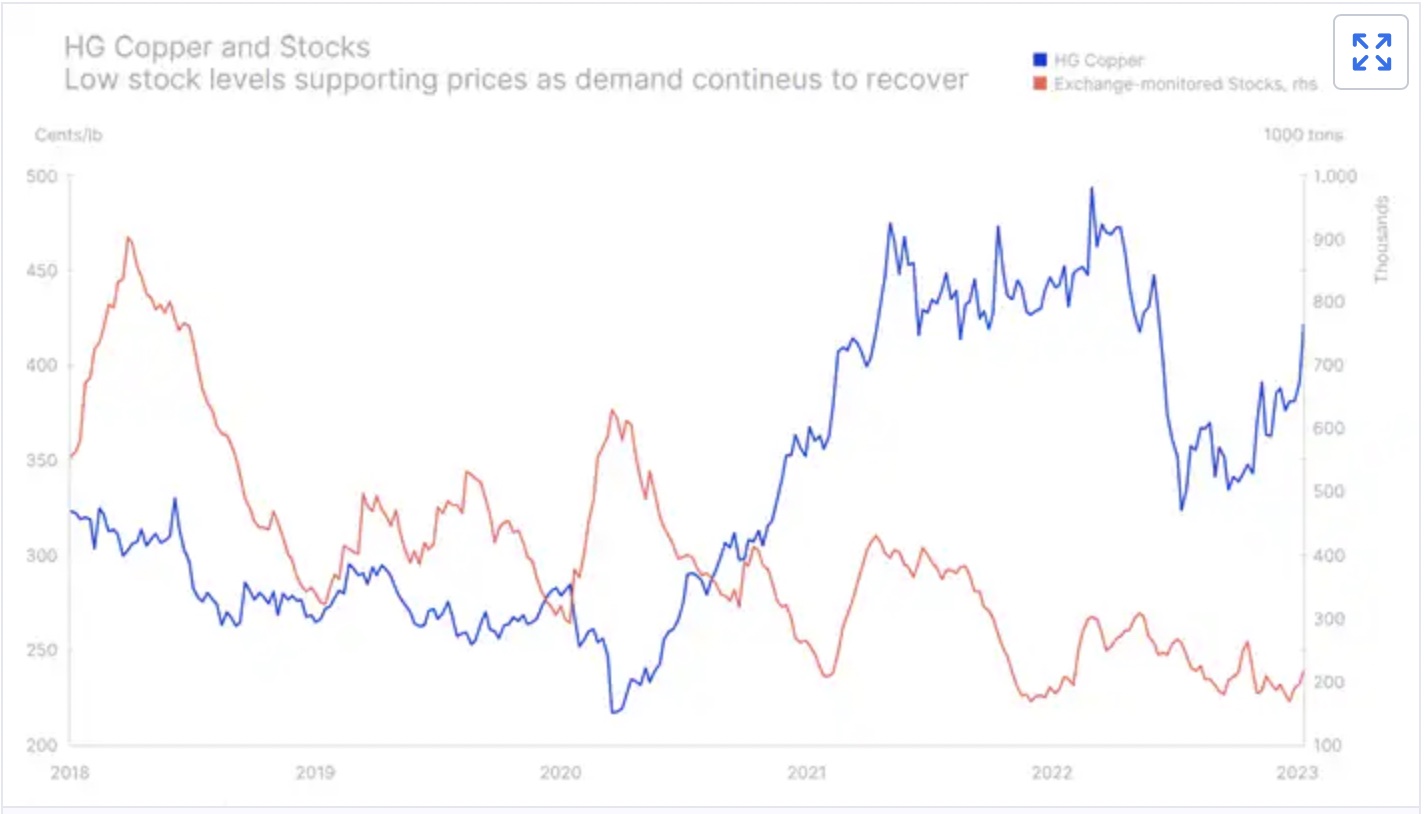

Copper

Inside our positive view on commodities we are significantly bullish on industrial metals, led by copper, aluminium and lithium due to the green transformation and the enormous political capital being invested in achieving this transition. In addition, the new geopolitical environment will mean a massive boost for the European defence industry which should see double-digit growth rates close to 20 percent per year over the next economic cycle as the European continent doubles its military spending in percentage of GDP.

Copper, together with aluminium, has already led a strong start to 2023 for industrial metals on speculation China, the world’s top consumer, will step up its economic support similar to what it did in 2003 (post-WTO entry), 2009 (post-GFC crisis) and 2016 (currency devaluation). This is in order to fuel an economic recovery to offset the economic fallout from President Xi’s failed and now abruptly abandoned zero-Covid policies. This optimism has been mixing with a weaker dollar on speculation that the Federal Reserve is slowing down the pace of future rate hikes as the inflation outlook continues to moderate.

The initial and strong rally in copper, however, has primarily been driven by technical and speculative traders frontrunning an expected pickup in demand from China in the coming months. Once the initial rally is over, the hard work begins to support those gains, with an underlying rise in physical demand needed to sustain the rally, not least considering the prospect of increased supply in 2023 as several projects go live. Overall we see copper settle into a USD3.75 to USD4.75 range during the coming months before eventually breaking higher to reach a new record sometime during the second half.

Gold and silver

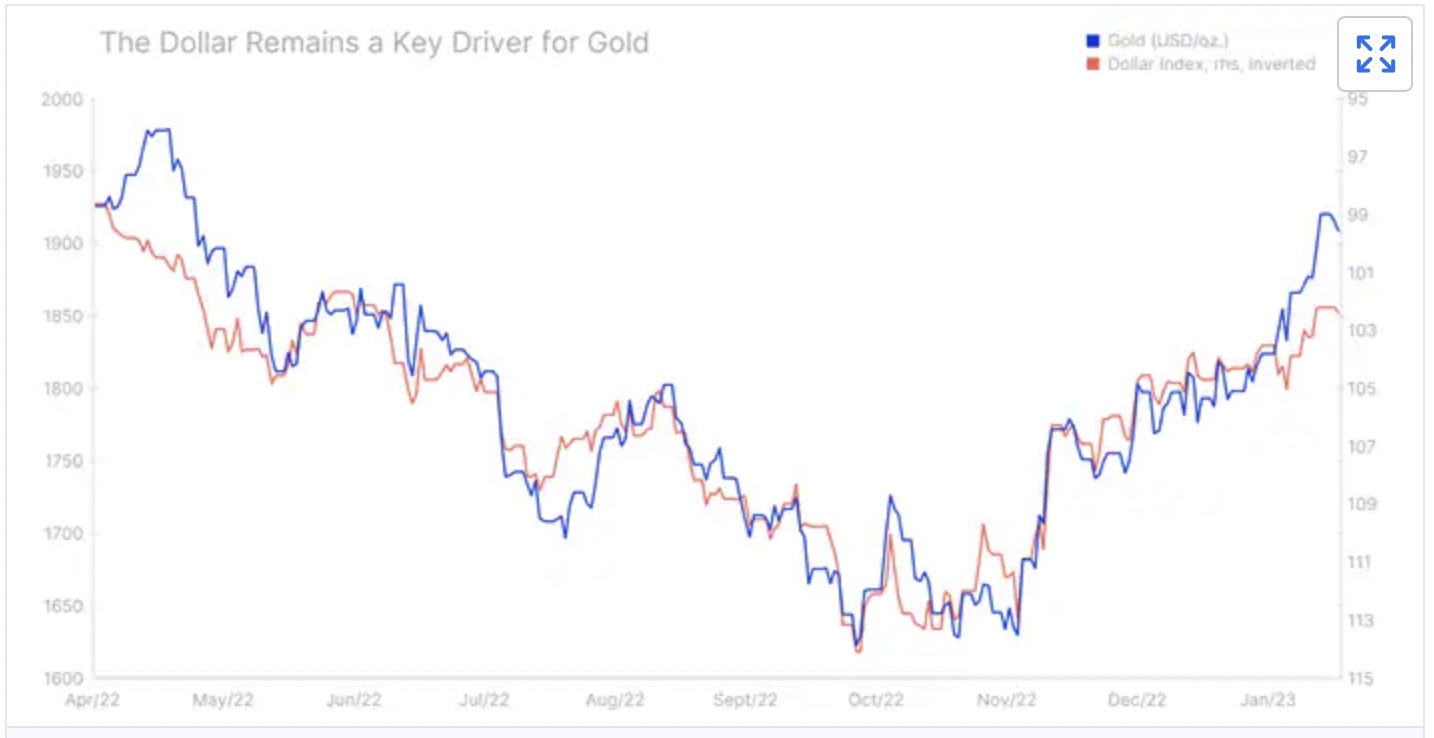

Gold jumped out of the gate to kick off 2023 with strong gains as the positive momentum, supported by a weaker dollar, carried over into the new year. Silver initially struggled to keep up but given our bullish view on copper we see the potential for silver outperforming gold during a year that will signal a turnaround from 2022 as previous headwinds, the stronger dollar and rising yields reverse to add support…

ALERT:

This company is about to start drilling what could be one of the largest gold discoveries in history! CLICK HERE OR ON THE IMAGE BELOW TO LEARN MORE.

In addition, we see continued strong demand from central banks providing a soft floor in the market. While last year’s record buying of 673 tons during the first three quarters alone (Source: World Gold Council) is unlikely to be repeated, the activity nevertheless is likely to create a soft floor under the market, similar to the one OPEC+ through actively managing supply has established under the crude oil market. Part of that demand is being driven by a handful of central banks wanting to reduce their dollar exposure. This de-dollarisation and general appetite for gold should ensure another strong year of official sector gold buying.

Adding to this, we expect a friendlier investment environment for gold to reverse last year’s 120 tons reduction via ETFs to a renewed increase. However so far, and despite the strong gains since November, we have yet to see demand for ETFs – often used by long-term focused investors – spring back to life, with total holdings still hovering near a two-year low. ETF demand struggles when investors trust central banks will deliver what they promise, and with inflation coming down that that trust is currently not being challenged.

However, it is our belief that inflation, following a slump during the next six months, will start to revert higher, primarily driven by rising wage pressures and China stimulus raising demand and prices for key commodities, including energy and metals. Until such time we will likely see gold spend most of the first quarter consolidating within a USD1,800 to USD1,950 range, before eventually moving higher to reach a fresh record above USD2,100. If achieved we could see silver return to USD30 per ounce, a level that was briefly challenged in early 2021.

Crude oil

Crude oil demand will, according to the International Energy Agency, rise by 1.9 million barrels per day in 2023, bringing the total to the highest ever. The main engine behind that price supportive call is a strong recovery in China as the country moves away from lockdowns towards a growth-focused recovery, driven not only by increased mobility on the ground but also supported by a post-pandemic recovery in jet fuel consumption as pent-up travelling demand is unleashed.

What it will do to prices very much depends on producers’ ability and willingness to bump up supply to meet that increase in demand. We expect multiple challenges will emerge on that front to support higher crude oil prices later in the year once demand in China increases, sanctions on Russian crude and fuel products continue to bite, and OPEC shows limited willingness to increase production.

The theme for our quarterly outlook, ie the model is broken, has very much been felt and seen across the energy sector this past year. Russia’s attempt to stifle a sovereign nation and the Western world’s push back against Putin’s aggressions in Ukraine remains a sad and unresolved situation that continues to upset the normal flow and prices of key commodities from industrial metals and key crops to gas, fuel products and not least crude oil. EU and G7 sanctions against Russian oil from December last year has created several new price tiers of oil where quality differences and distance to the end user no longer are the only drivers of price differentials between different crude grades. Seaborne crude oil flows from Russia has held up but will increasingly be challenged in the coming months as EU’s product embargo is introduced in February.

These developments have forced Russia to accept a deep discount on its crude sales to customers not involved in sanctions, especially China and India. The second-wave reaction to these developments has been strong refinery margins in China, a country with capacity beyond what is required for the domestic market. Depending on the strength of the economic rebound in China, we are likely to see an increase in product flows from China to the rest of the world. Together with the US, the Middle East, an emerging refining powerhouse, these flows will likely make up the shortfall in Europe from the removal of supply from Russia.

Crude oil’s trajectory during the first quarter primarily depends on the speed with which demand looks set to recover in China. We believe the recovery will be felt stronger later in the year, and not during the first quarter which seasonally tends to be a weak period for demand. With that in mind we see Brent continue to trade near the lower end of the established range this quarter, mostly in the USD80s before recovering later in the year once recession risks begin to fade, China picks up speed and Russian sanctions bite even harder.

OPEC meanwhile has increasingly managed to rein back some price control, not least considering the level of market share it controls together with members of the OPEC+ group. Through their actions they have been able to create a soft floor under the market and the question remains how they will respond to a renewed pickup in demand. Not least considering their frustrations with Western energy companies and what they see as political interference in global oil flows and not least last year’s decision by the White House to release crude oil from its Strategic Reserves.

Overall we see another year where multiple developments will continue to impact both supply and demand, thereby raising the risk of another volatile year which at times may lead to reduced liquidity and with that fundamentally unwarranted peaks and troughs in the market. Following a relatively weak first quarter where Brent should trade predominately in the USD80s, a demand recovery thereafter combined with supply uncertainties should see Brent recover to trade in the USD90s with the risk of temporary spikes taking it above USD100.

Summary:

Following a dramatic and volatile 2022 with good returns, a lot of this year’s commodity performance may be driven by Chinese politics.

ALSO JUST RELEASED: Silver May Hit $700 After Multi-Decade Breakout CLICK HERE.

ALSO JUST RELEASED: Newmont Newcrest Merger May Kickoff A Golden Wave Of Merger Mania CLICK HERE.

ALSO JUST RELEASED: The Global Financial System Is Already Doomed And The Collapse Will Be Terrifying CLICK HERE.

To listen to Stephen Leeb discuss Putin, gold, China, the US and what surprises to expect in 2023 CLICK HERE OR ON THE IMAGE BELOW.

To listen to Alasdair Macleod discuss the $100 takedown in the paper gold market and what to expect next CLICK HERE OR ON THE IMAGE BELOW.

© 2023 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.