On the heels of the US debt downgrade, US debts and deficits now matter.

US DEBT DOWNGRADE: US Debts And Deficits Now Matter

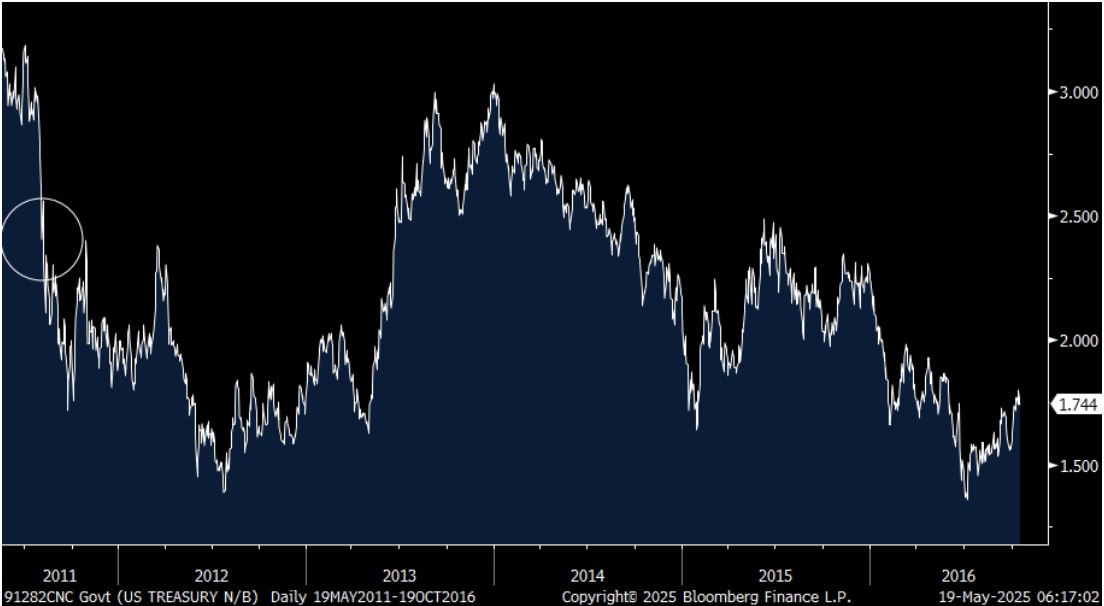

May 19 (King World News) – Peter Boockvar: Yea, US debts and deficits now matter and I don’t say that because of the Moody’s downgrade as S&P did this about 14 years ago in August 2011 and it certainly didn’t matter then. I say it because markets clearly care now and have for the past few years. Understand that in June 2011, the Fed had just ended QE2 and rather worry about the credit implications then of a US downgrade a few months later, the Treasury market was more worried about a double dip recession and the 10 yr yield went DOWN in the year following the downgrade.

This followed a trend where yields went UP during QE1 and QE2 because of the reflationary belief of policy. Fed rate policy was a real driver then too with zero interest rates (totaling 7 years and didn’t get raised until 2015). Now, the long end of the yield curve continues to speak for itself and has been for the last few years and rate cuts have been more tweaks than anything else. Then too in 2011 we were still in a bond bull market. Today, we are three years into the bear, I believe.

On the day after the S&P downgrade, the 10 yr yield response was literally one day. On Friday August 5th, 2011, the 10 yr yield jumped 16 bps to 2.56%. On Monday August 8th though, it plunged by 24 bps to 2.32%. The US dollar index also had a one day blip then. On that Friday it fell .7% to 74.6 and rallied by .25% on that Monday and one month later was unchanged. The US dollar today is of course much higher as yields are too but I think the trend is still higher for the long end and the post tariff foreign rethink of US assets is a brand new, big picture, really important new trend that I believe will continue for the coming years and that means a lower US dollar too.

I circled where 10 yr yield was in days before S&P downgrade on August 5th, 2011. The jump in 2013 was the taper tantrum.

What Moody’s Said About US Debt Downgrade

This is what Moody’s actually said:

“This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns.”

“Successive US administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs. We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration. Over the next decade, we expect larger deficits as entitlement spending rises while government revenue remains broadly flat. In turn, persistent, large fiscal deficits will drive the government’s debt and interest burden higher. The US’ fiscal performance is likely to deteriorate relative to its own past and compared to other highly rated sovereigns.”

I’ll add, we don’t have a tax/revenue problem, we have a massive spending problem and unfortunately only sharply higher interest rates will get the attention of Congress and based on what is being debated right now in DC, it doesn’t look like we’re there yet in terms of crisis type thinking. That said, at least there is a conversation on means testing Medicaid in terms of work requirements but nothing more when it comes to our entitlement programs. I know, it’s a tough, complicated conversation.

The US 10 yr yield is back above 4.50% and the 30 yr yield is at 5.02-.3% in response.

Foreigners Selling US Tech Stocks

So, to my point of the foreign rethink of US assets, I’ve said many times here that Mag 7 stocks because a global reserve asset that not just US institutional and retail investors owned but foreigners did in a big way too, including foreign central banks. I went through some 13F’s in some of the Mag 7 names as of 3/31/25 (so doesn’t include the response to the April 2nd tariff announcement and pause) and here is a small sample of what I saw.

In Nvidia, Japan’s Government Pension Investment Fund sold 17.6 million shares taking their holdings to 149.5 million. The Royal Bank of Canada sold 1.5 million shares leaving them with still a large 81.6 million shares. HSBC sold 7.1 million shares and hold 80 million as of 3/31. Mitsubishi UFJ sold 16.4 million shares to 66.5 million. CIBC sold shares as did Toronto Dominion and Schroders. The Swiss National Bank slightly shed some shares, selling 225k shares but still leaving a large holding of 69 million shares. I await the updated holdings of the Norges Bank.

In Microsoft, Japan’s Government Pension Investment Fund sold 4.1 million shares which was about 10% of their holdings. RBC sold about 1 million shares to 31 million. HSBC actually added some shares, 622k to 24.5 million. The Swiss National Bank tweaked its holdings lower by 27k to just under 20 million. Schroders sold 280k shares to 18.3 million while TD and CIBC saw slight increases.

My guess is that a pronounced trend likely took place in April.

Foreigners Still Buying US Debt

The March TIC data came out late Friday and foreigners bought a large $123b of US notes and bonds with private buyers making up $82b of it. Central banks bought the balance but after four months of selling. The trend has been lower holdings from foreign central banks where in contrast a lot of buying has been on the private side and including hedge funds. That in March was captured by the holdings of the Cayman Islands which was the 2nd biggest buyer, totaling $37.5b.

Foreign flows also come thru UK banks and the UK is now the 2nd biggest holder of US Treasuries as a result. Japan remains the biggest at $1.13 trillion while China’s holdings are down to $765b, lower by almost $20b in March. As the basis trade started to unwind in April, the next TIC report will be important to see in the Cayman Island holdings.

While foreigners still buy US Treasuries in totality, they continue to buy less as a % of total marketable securities. Those holdings are at about 30% vs about 50% 15 years ago.

What To Do

King World News note: Gold is trading higher on the heels of the US debt downgrade as is silver. Continue to accumulate physical silver while the Gold/Silver ratio is at 100/1. Eventually the Gold/Silver ratio should trend all the way down to 15/1. Buying physical silver is trading in fiat money to purchase the cheapest hard asset on the planet.

One Of The Best Audio Interviews Of 2025!

Stop whatever you are doing and listen to this remarkable audio interview with Jonathan Haycock because nothing you read or listen to this weekend will top this one! CLICK HERE OR ON THE IMAGE BELOW.

Just Released!

To listen to Alasdair Macleod discuss the takedown in the gold and silver markets and what to expect next CLICK HERE OR ON THE IMAGE BELOW.

© 2025 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.