On the heels of an absolutely wild week of trading, shocking events are unfolding in China’s gold market.

Alasdair Macleod’s audio interview discussing shocking events unfolding in China’s gold market has just been released (LINK AT BOTTOM).

Foreigners flee the US$, Buy Gold

April 18 (King World News) – Alasdair Macleod: Anti-dollar sentiment is underestimated, and loss of credibility has only just started. A perfect storm is driving gold higher and the dollar down, compounded by systemic issues.

In this market report for precious metals, we examine the factors driving gold higher. Its remarkable performance is doubtless confusing the wider public, leaving investors in western financial markets invested in non-performing assets while missing out on gold.

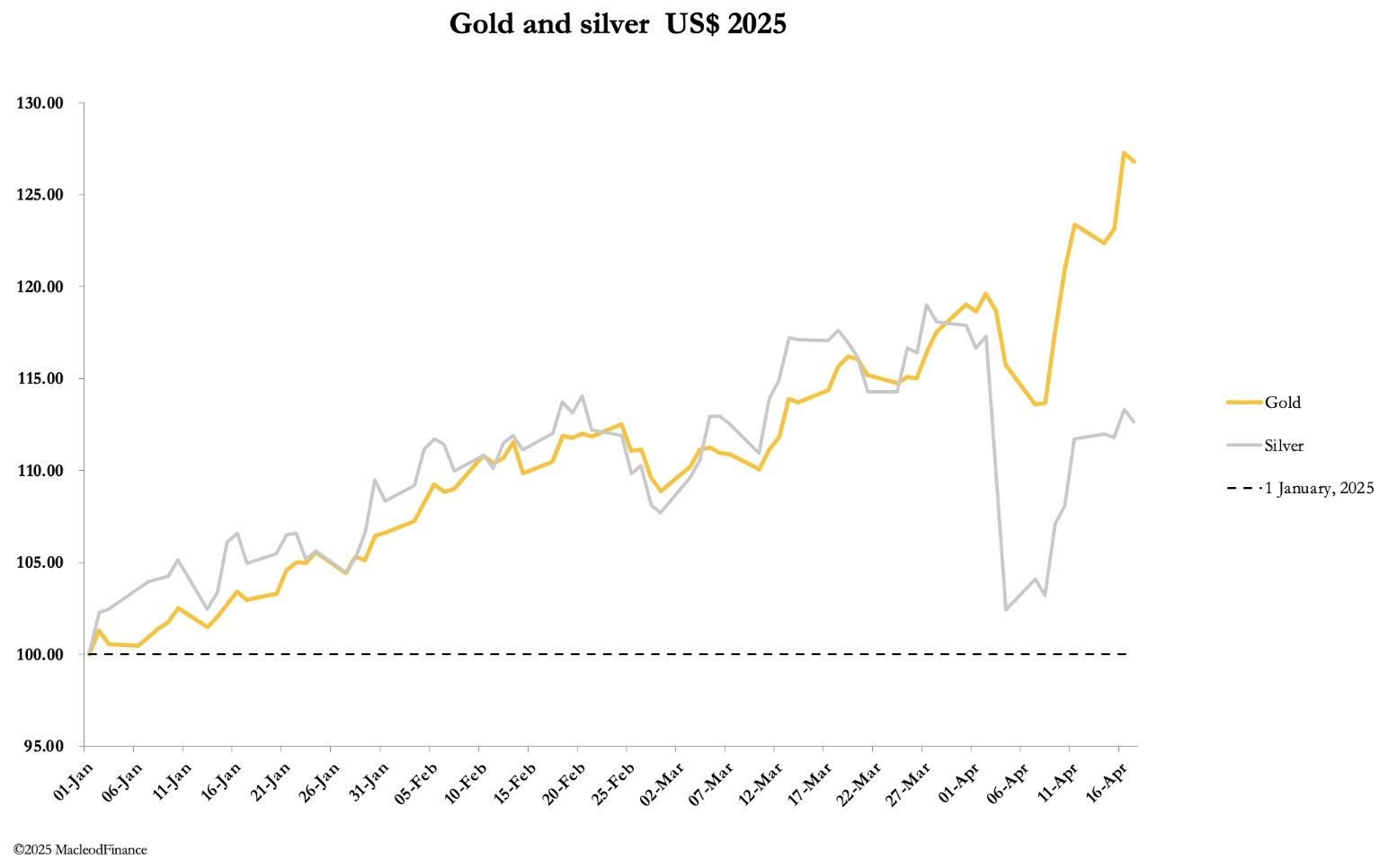

So far this year, gold is up 24%, copper 15.5%, and silver 10.15%. The S&P 500 is down 11.5% and the 10-year US Treasury Note up 2%. The least exposure general investment portfolios have is to gold and its investment substitutes.

This raises the most important questions for portfolio managers: with gold having risen so far, should we buy it or have we missed it?

Read on!

This week saw a continuation of last week’s strong rise in gold following the very brief pullback for both gold and silver at the beginning of the month. Today, being Good Friday, London and New York are closed. But on Thursday gold closed at $3327, up $111 for a two week rise of $288, 9% higher. Silver ended yesterday at $32.55, up only 27 cents, most of its rise happening the week before.

As our headline chart shows, silver has been left behind, which is reflected in a gold/silver ratio of 102. This is next:

This split in performance between gold and silver is undoubtedly due to a sharper liquidity squeeze in gold. While both gold and silver have acute liquidity shortages, in gold they are more acute because of its regulatory status.

In times of heightened credit risk, for banks gold bullion in possession is a high-quality liquid asset according to Basel 3 regulations, whereas derivative positions carry regulatory-defined risk. This does not apply to silver — I shall be analysing the outlook for silver in a separate report shortly.

Basel 3 has the effect of tightening supply in gold derivatives, such as Comex futures. It explains why short positions have come under pressure to close, reflected in the contraction of open interest, despite gold hitting new highs:

This is despite gold hitting new highs after new highs. Instead, it is the squeeze driving gold higher.

It is routinely stated by LBMA commentators that bullion banks are long of physical in London and hedge price risk on Comex. Even if that is true, given gold’s HQLA Basel status, there’s little point in compromising it by hedging price risk in derivative futures, because of the balance sheet risk in the Basel 3 schedules.

Therefore, this squeeze on Comex is unlikely to end soon, particularly with gold’s HQLA status due to be adopted by US banks later this year. But that’s not all.

The withdrawal of bullion from the Bank of England destined for Comex warehouses confirms to central banks with earmarked gold stored in Threadneedle Street the folly of leasing, particularly when increasing numbers in their ranks are selling fiat for gold and taking it into their possession. At the very least, a herd instinct tells them not to renew leases when they fall due.

Throughout the fiat currency era, leasing gold has provided liquidity upon which the entire mountain of gold derivatives depends. That facility is undoubtedly being withdrawn with systemic consequences.

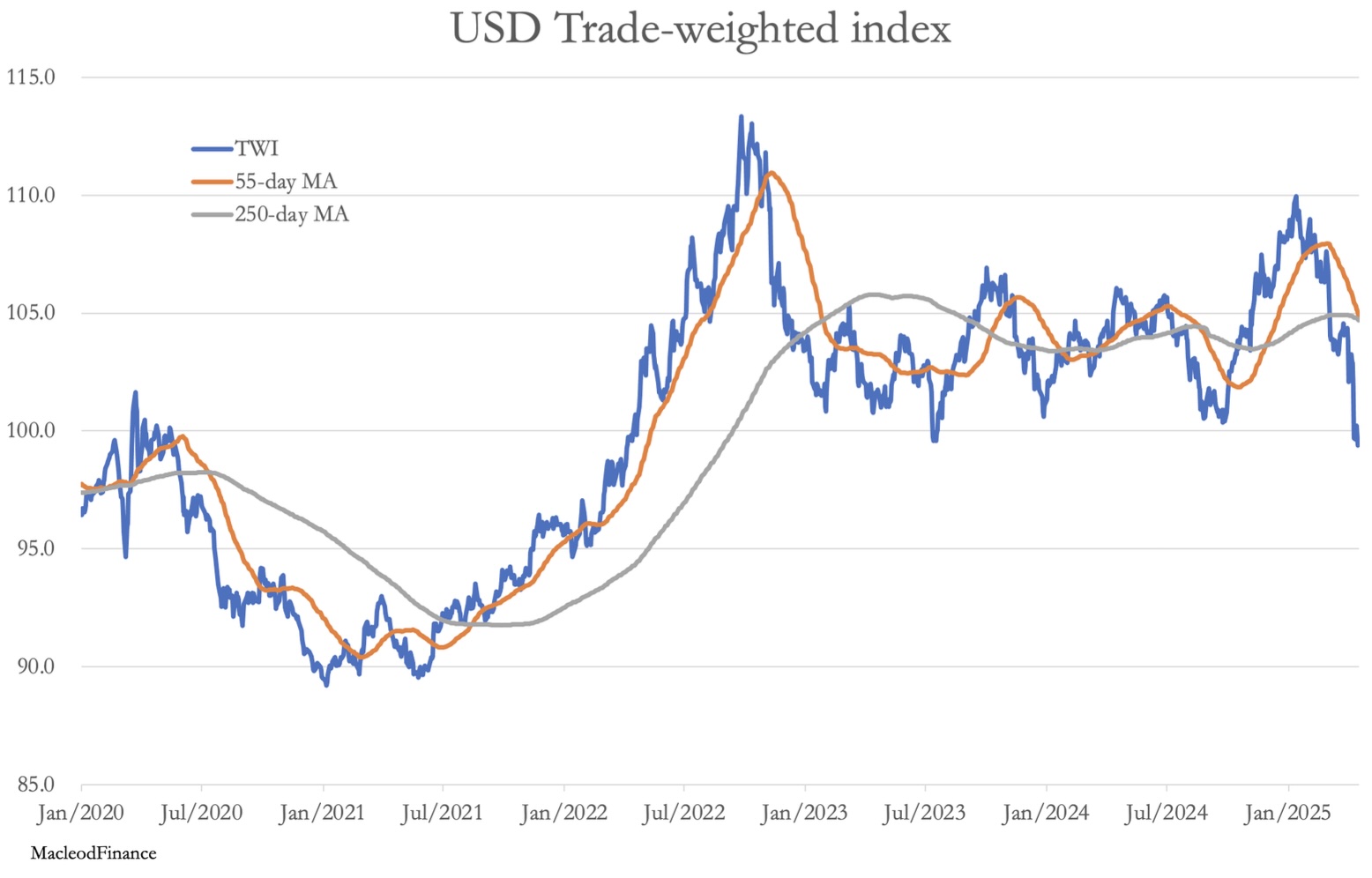

The flight out of the dollar creates further impetus for gold prices. The US-centric financial press and market commentators underplay the mounting distrust foreigners have for Trump and the US Government. But it is all too real, being compounded by Trump’s capricious vacillations on tariffs. A dam holding back $40 trillion of foreign-owned US financial assets and bank deposits is bursting, reflected in the dollar’s trade-weighted index:

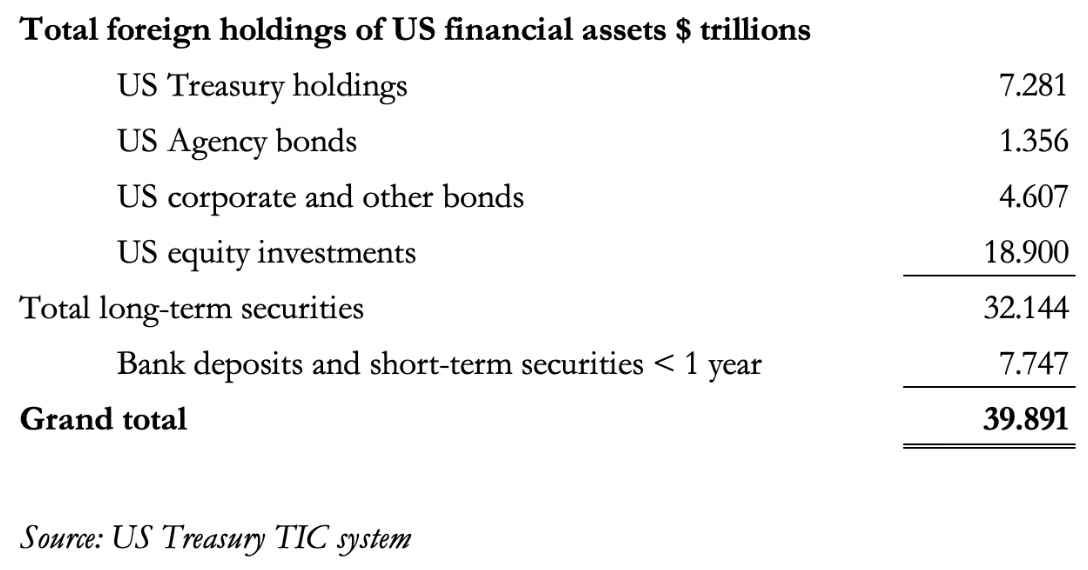

With a death cross confirming in the moving averages and a two-year consolidation being broken on the downside, this chart looks truly awful for the dollar. It reflects huge selling pressure building not just for the dollar, but bonds and equities as well. This is the latest known assessment of foreign dollar exposure, according to the US Treasury, excluding derivatives, all of which is potentially on the market:

Shocking Events Unfolding In China’s Gold Market

Last week was simply a pre-Easter pause in dollar selling by foreigners after the shock of the previous week. It’s hard to think otherwise than that the slide in the dollar and the systemic squeeze on gold is set to continue and that it is just an early warning for what is yet to come…to listen to Alasdair Macleod discuss shocking events unfolding in China’s gold market CLICK HERE OR ON THE IMAGE BELOW.

© 2025 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.