Gold is soaring $130 higher and silver futures are rocketing up over 8%, but investors don’t realize that the stock market is yet to crash but it will.

January 5 (King World News) – Alasdair Macleod, writing for VON GREYERZ: Stagnating economies, together with high government debt loads, inevitably create funding crises and debt traps. Nowhere is this problem more destructive than for the fiat dollar.

But it’s not just the dollar. Economies in the Eurozone and the UK have insufficient growth to support their colossal mountains of government debt. In this article, I explain the mechanics of a debt trap. And how a combination of rising interest rates reflecting growing risk and stagnating economies bring on debt traps, leading to yet higher interest rates making the situation even worse.

My memory is of the sterling crisis in 1976, when the IMF bailed out the British government, and the Bank of England had to fund medium-term debt with gilt coupons of over 15%. The Labour government was forced to cut its spending to resolve the situation. So I have a question for today: who is going to bail out first, the US Government, then the UK and Eurozone, and who is going to force them to cut spending on the edge of a recession?

Only the markets will do it: crisis first, and only if we are lucky, the solution follows. Read on…

Listen to the greatest Egon von Greyerz audio interview ever

by CLICKING HERE OR ON THE IMAGE BELOW.

Introduction

Understanding debt, the counterpart of credit, is of increasing importance. For example, it is the other side of bank credit, and when banks become overleveraged, there comes a time when their managers become concerned about the risk to their balance sheets. In any economy, the risk is conventionally understood to be in private sector lending, and a recession is part and parcel of the withholding of further credit, leading to corporate and personal insolvencies. Under these circumstances, banks redirect their balance sheet assets from private sector loans and corporate bonds to government debt, which is seen as the risk-free asset in any currency.

There are signs that, with respect to some jurisdictions, these views are evolving, with the outlook for government debt being examined more closely. There is also little confidence in economic prospects for all the major economies, improving government budgets.

Given mounting government debts, debt is a problem no longer confined to private sectors which have suffered from the generally unexpected rise in interest rates over the last few years. And governments in the advanced economies appear to have little sense of the debt trap being sprung upon them, too. As well as the rate of nominal GDP growth, the interest rate matters and a combination of slowing economies moving into recession together with high interest rates is a lethal combination for government finances.

More specifically than growth in GDP, what matters is the growth in tax revenue required to fund the pace at which the combination of debt and interest is being rolled over. In Europe and the UK, tax rates are already so high that attempts to obtain more revenue by increasing them will almost certainly lead to lower revenues due to the Laffer curve effect. The US is probably not at that point yet tax-wise, but economic stagnation has the same effect.

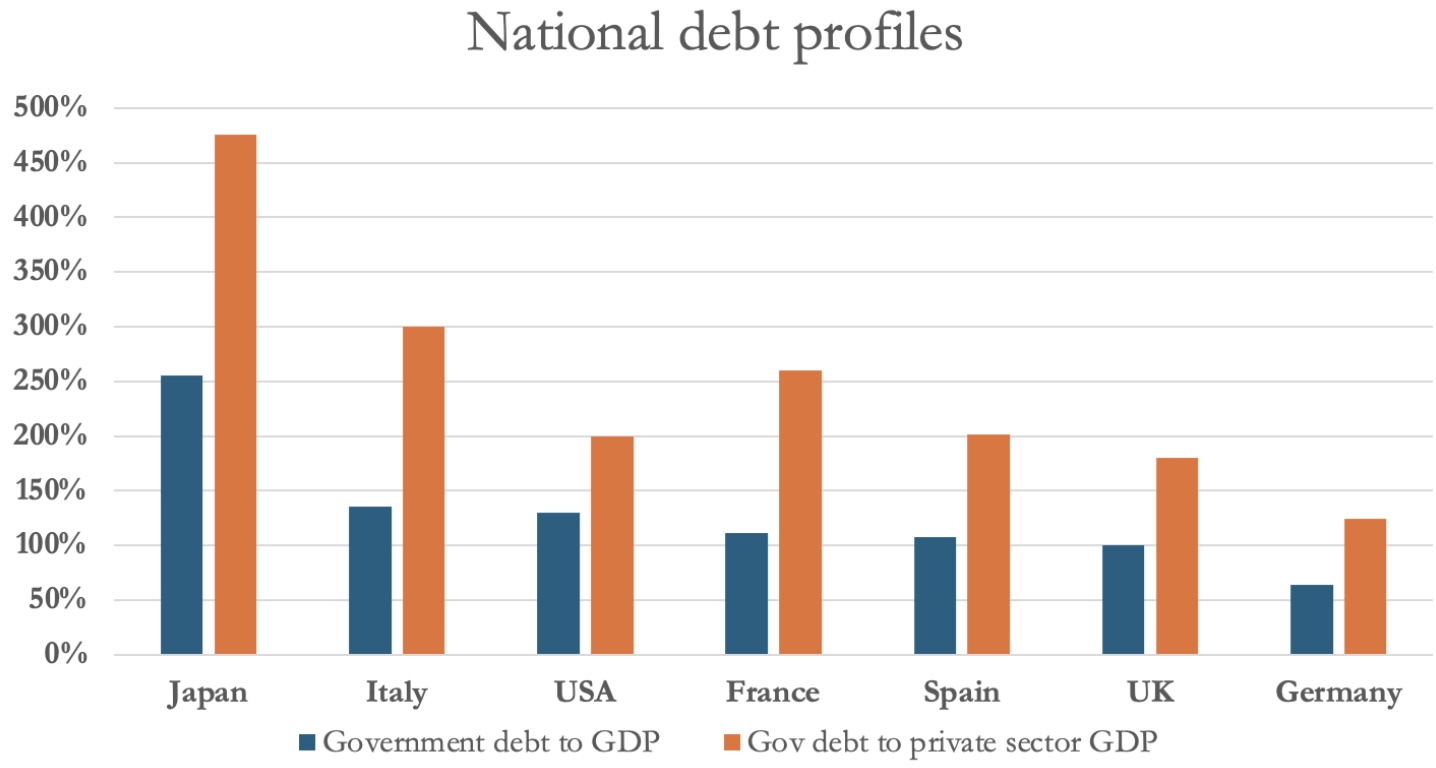

The following table illustrates government indebtedness relative to GDP for the G7 nations and also relative to private sector GDP, which produces the revenue for governments upon which debt credibility depends.

Various papers have been written on this problem, all concluding that a debt trap occurs when the rate of GDP growth falls to below the rate at which the cost of funding the debt increases. But it is surely more correct to compare the rate of increase of tax revenues with the rate of increase of the debt: do tax revenues increase more rapidly than the debt, or does the compounding debt increase more rapidly than revenues?

How did governments cut the debt-to-GDP ratio following WW2?

Much of the complacency over government debt levels arises from the fact that high WW2 debt levels were reduced over the following two decades to manageable levels, fuelling a belief that it can be done again. America’s government debt to GDP in 1946 peaked at 120%, below current peace-time levels, falling to 35% in 1971 when Nixon suspended the Bretton Woods Agreement. The relevant figures are shown in the table below.

The increase in gross Federal debt was 142%, but the increase in GDP was 483%. And the increase in revenue, which ultimately pays for the debt, was slightly more than the increase in GDP. Therefore, revenue growth outpaced debt growth nearly three and a half times, leading to a significant reduction in debt to GDP. This was how the war debt relative to GDP was reduced, before the discipline of gold on government spending and interest rates was finally abandoned.

The common belief that debt reduction was due to financial repression, that is to say, the cost of funding was suppressed by central bank interest rate policies and yield curve control, is incorrect. To understand why, we need to address another point. And that is what happened to prices. The dollar and through the dollar all other currencies were tied to gold at $35 for the whole 25 years, but the CPI for Urban Consumers rose from 22 to 40, nearly doubling at an average annual rate of about 0.7%. Yet, measured in gold there should have been no inflation, because the expansion of economic activity under a gold standard is expected to lead to better manufacturing processes, product improvements, and a tendency towards falling prices.

The problems with a CPI measure are many. Logically, there is no such thing as a statistical measure of price inflation, the subjectivity of which has been clearly demonstrated in more recent decades by wildly differing estimates. Government intervention in the economy distorts outcomes, and the savings rate fluctuated, but not enough to explain the disparity between a steady gold standard and a statistical outcome.

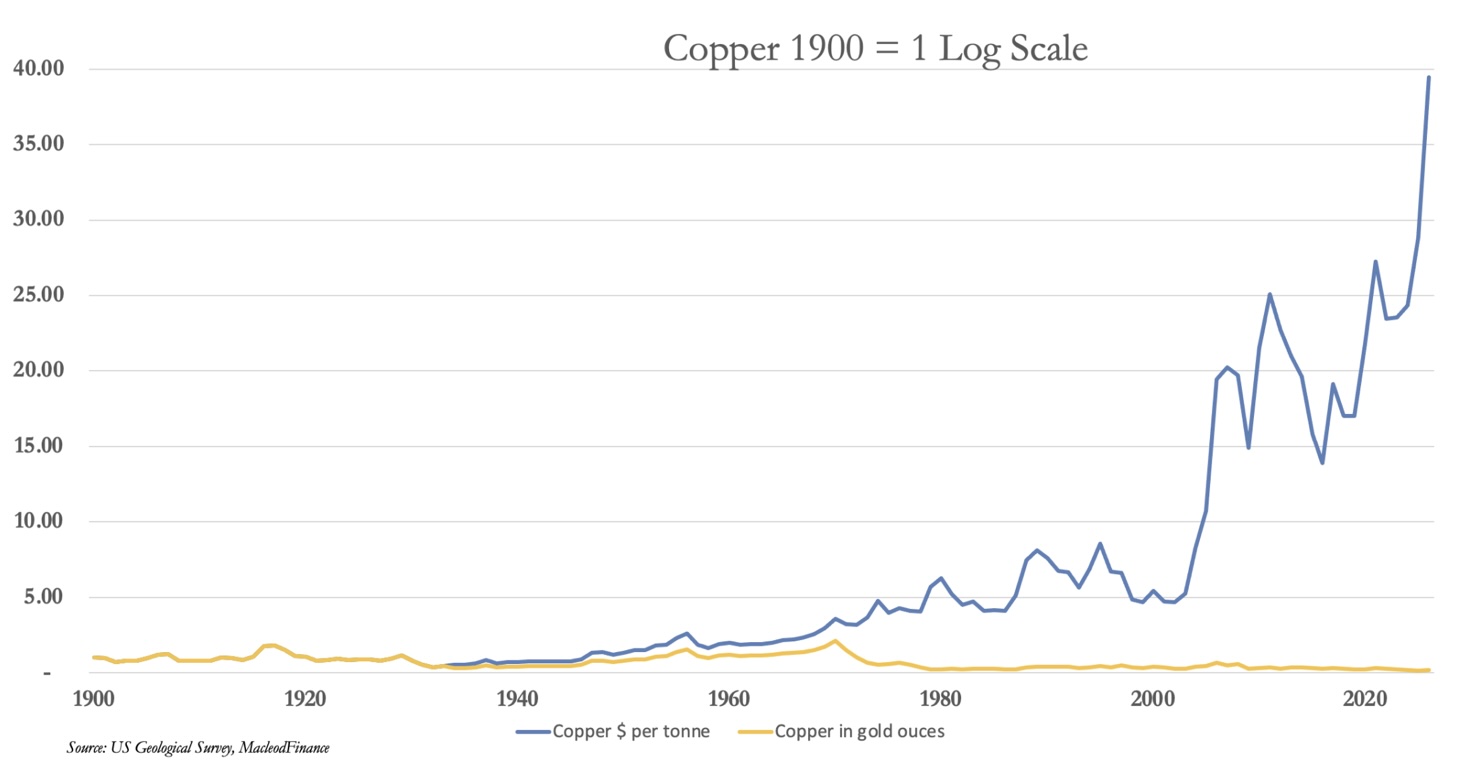

A cleaner price comparison is found in commodity prices. Oil was pegged at $2.57 per barrel, increasing to $3.56, which held until 1973: that’s a 38% increase compared with a near doubling of US consumer prices. Copper was similarly more stable priced in gold, as the next chart demonstrates.

That both copper and oil did increase in price by either measure in the post war years can be explained by demand increasing for these commodities more rapidly than supply. But this does not get round the fact that with the dollar supposedly acting as a gold substitute at a fixed value of $35 per ounce there is an unexplained disparity in consumer price performance. The answer is that the Bretton Woods system ended up suppressing the value of gold, evidenced by the selling down of US gold reserves from 21,828.2 tonnes in 1949, representing over 70% of global official reserves and 45% of total above-ground stocks, to 9,069.7 tonnes, less than 25% of global official reserves and only 12% of above-ground stocks in 1971.

The suspension of the Bretton Woods Agreement in August 1971, far from removing gold from the monetary system, had the effect of releasing gold from its increasing suppression by US economic policies in the post-war years. It is important to understand this relationship in its proper context, now that in this new millennium US Government debt is spiralling out of control.

This millennium is different from the post-war years

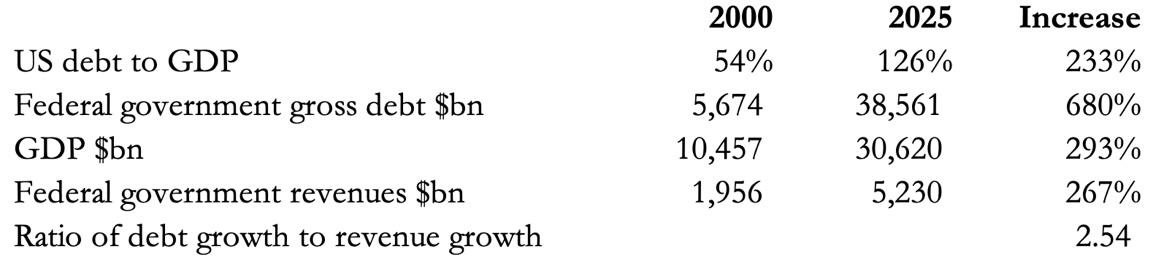

The next table replicates the first table in this article, but for the 25 years of this current millennium.

Here, we can see that gross debt has been rising nearly three times faster than GDP, and even more so measured in the federal government revenues which are behind the sustainability of the debt. With the increase in revenue badly lagging the debt increase, the US Treasury is in a classic debt trap, a condition which has been accelerating, particularly since the pandemic of 2020. It is a fact which is increasingly recognised by foreign central bankers who are getting out of dollars and into gold.

The second element of the debt trap – soaring interest rates

So far, we have seen that in the first 25 years of this new century, the increase in tax revenue has failed lamentably to keep pace with the increasing growth of debt. For the US Government, this has not mattered too much while the Fed was able to suppress interest rates even to the zero bound and therefore contain the compounding cost of funding. Additionally, with the dollar being everyone’s reserve currency, foreign buyers were always demanding them and investing in the regulatory “risk-free” status of US Treasury debt. It is this combination which has extended the dollar’s life as a fiat currency, pushing it even further into a debt trap waiting to be sprung by higher interest rates.

Interest rate suppression is less evident today, at least not to the degree of recent years. The sharp rise in interest rates and bond yields between2021—2023 have only partially been corrected in the belief that inflation has receded as a problem. This is an error, because the inflationary consequences of a $2+ trillion budget deficit and a decline in the personal savings rate will continue to feed into a falling purchasing power for the currency. And geopolitical factors encourage members of the Shanghai Cooperation Organisation and BRICS, representing a large majority of the world’s population, to reduce their dollar exposure as well.

Both these factors are feeding into an inevitable funding crisis for the US Government, as foreign buyers of US Treasury debt stay away, and in some cases are actually selling. And instead of interest rates and bond yields being under the control of the Fed, they will be exposed to the brutal consequences of falling market demand. A buyers’ strike by foreign investors at the margin is already forcing the US Treasury to fund itself in short-term T-bills, with auctions for longer maturities being generally avoided. Increasingly, the $38.6 trillion debt mountain sees longer maturities being replaced by T-bills as well. The whole maturity structure of US Treasury debt is changing, and it is not for the good.

The yield curve has begun to price in maturity risk, with the 30-year long bond yielding 68 basis points more than the 10-year note, and 127 bp more than the 6-month T-bill. But there is a further problem: in a debt trap, the higher the funding cost, the less attractive an investment proposition becomes, because the compounding pace at which the debt rises accelerates.

The consequences for the credit bubble

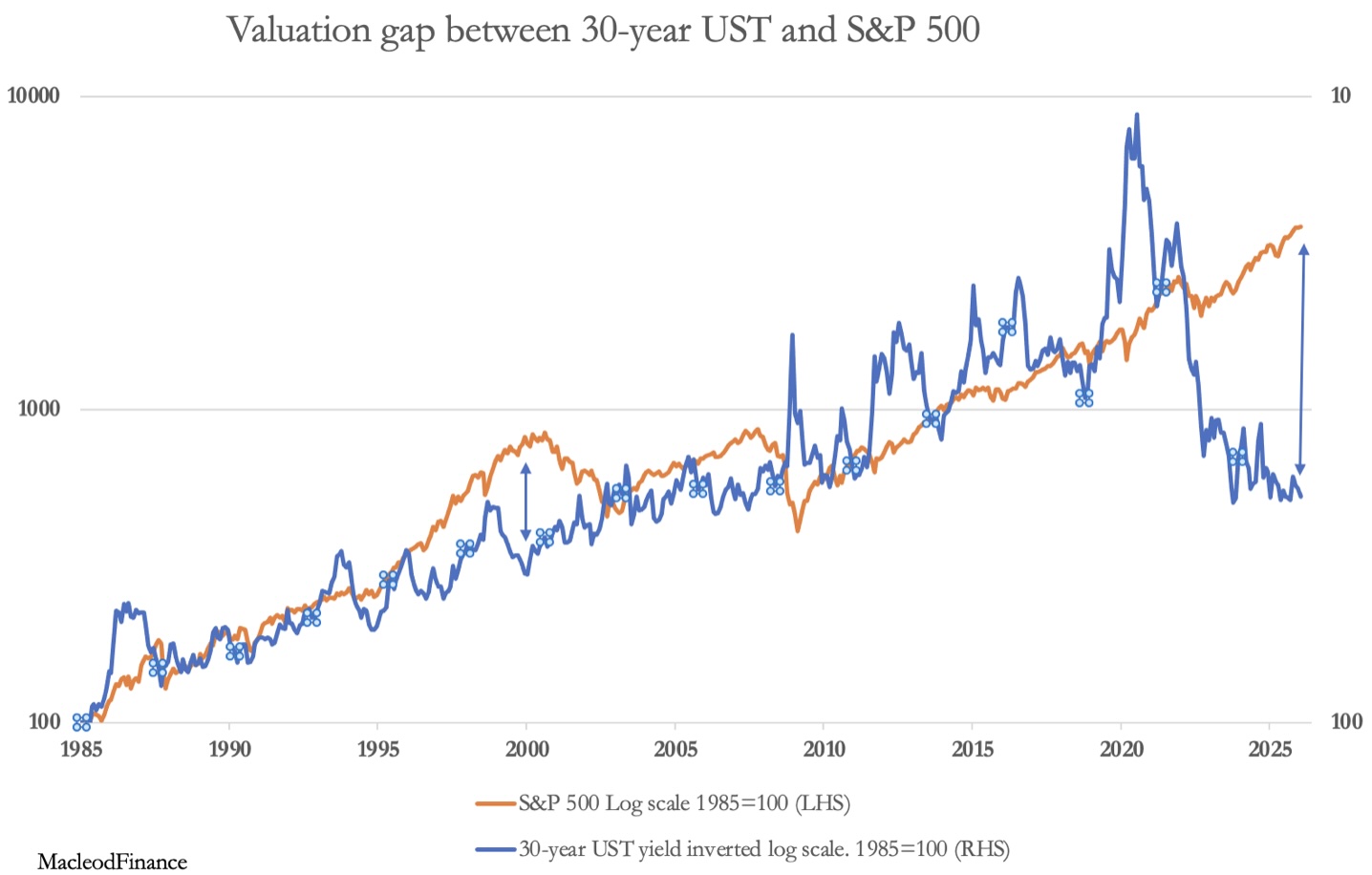

For every debt, there is a credit and in recent years significant quantities of this credit, has found its way into financial instruments, particularly equities. As the interest cost on this debt increases, the credit side of the bubble will burst. Today, the disparity between the returns on long maturity bonds and equities is at an all-time record, illustrated by the chart below:

It is worth taking time to study this chart closely. Not only is the excessive value of the S&P over the long bond greater than it has ever been, but it shows signs of going higher due to rising bond yields. This will only be resolved by an equity crash to rival or even exceed anything seen in history.

It is hardly a surprise that gold measured in dollars is rising at an accelerating rate. It reflects and signals that a final collapse in the dollar’s credibility as a currency is underway. This will link you directly to more fantastic articles from Alasdair Macleod, Egon von Greyerz and Matthew Piepenburg CLICK HERE.

To listen to Alasdair Macleod discuss what to expect for gold, silver and the miners in 2026 CLICK HERE OR ON THE IMAGE BELOW.

ALSO JUST RELEASED!

Silver Sparkles & Gold Shined In 2025 But Look At What’s Ahead In 2026 CLICK HERE.

Silver, And What Stood Out To Me The Past Two Weeks CLICK HERE.

Here Is The Remarkable Big Picture Setup For Gold As We Head Into 2026 CLICK HERE.

CNBC Antics About The Silver Market CLICK HERE.

Turnaround Tuesday As Silver & Gold Soar, But Take A Look At This… CLICK HERE.

Black Monday For Gold, Silver & Platinum Markets. Here Is Where Things Stand CLICK HERE.

Costa – Here Is The Big Picture After Silver & Gold Prices Tumble CLICK HERE.

Tavi Costa – What A Week As Silver Explodes To The Upside! CLICK HERE.

Historic Silver Short Squeeze Sends Price Soaring Over 7% On Friday! CLICK HERE.

An Astonishing Christmas Prediction From Legend Richard Russell CLICK HERE.

EXPECT WAR: Early Days For Gold & Silver Bull, Especially The Miners CLICK HERE.

Hansen – This Is What Is Really Happening With Gold Market CLICK HERE.

$15,000 TARGET: Volatile Gold & Silver Trading But Look At What Is Coiled To Skyrocket CLICK HERE.

Michael Oliver – Historic Breakouts Will Now Send Gold & Silver Prices To Levels That Will Shock The World! CLICK HERE.

© 2026 by King World News®. All Rights Reserved. This material may not be published, broadcast, rewritten, or redistributed. However, linking directly to the articles is permitted and encouraged.